Advertisement

Susan Springfield Announces Retirement after 13 years.

First Horizon Corporation announced that Executive Vice President, Head of Franchise Finance Thomas Hung will be named senior executive vice president, chief credit officer, effective October 1, 2024. Hung will succeed Susan Springfield, senior executive vice president, chie...

Advertisement

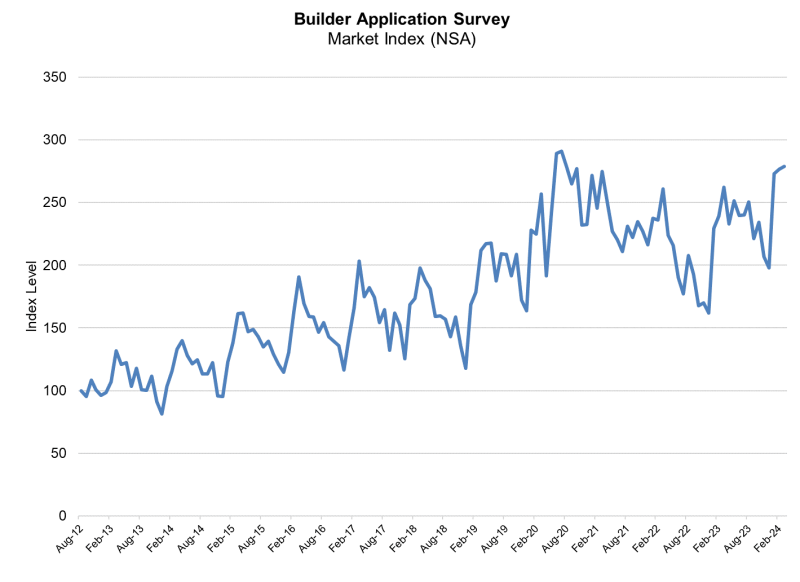

Latest data breaks four-month period of gains for HMI Index

Builder sentiment flatlined in April as mortgage rates remained close to 7%, inciting mixed reactions from housing analysts on the new-home market. The National Association of Home Builders (NAHB)/Wells Fargo Housing Market Index, (HMI) released Tuesday, showed builder co...

Renew your NMLS License — for free.

Enjoy access to a free NMLS renewal class when you attend an in-person event.

More from

Regulation and Compliance