BY MARK PAOLETTI | SPECIAL TO NATIONAL MORTGAGE PROFESSIONAL

AT A GLANCE - Key Economic Data and Events during December 2021

- Interest Rates drifter higher. The 10-Year Treasury yield rose to 1.52% (Dec 31) from 1.43% (Dec 1).

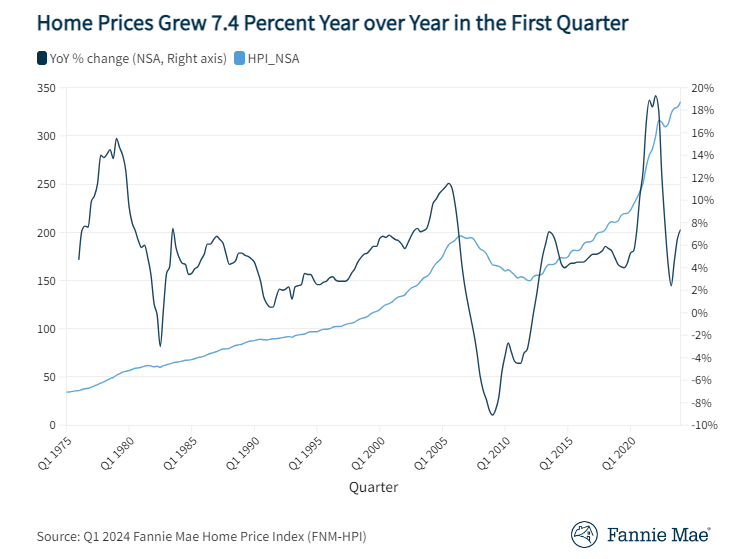

- Housing: Home Prices continue rising about 1.0% per month, New and Existing Home Sales are still making gains, and new construction is accelerating to meet demand.

- Labor: Disappointing Job creation as the Economy created only 210,000 new jobs in November, the Unemployment Rate dropped to 4.2%, and Wage Growth increased 4.8% YoY.

- Inflation raged higher in December: CPI up 0.8% (+6.8% YoY), PPI up 0.8% (+9.6% YoY).

- The Economy: US GDP grew at a 2.3% annualized rate during the 3rd Quarter of 2021, with a 4.9% growth rate in the last 12 months.

- Consumers: Retail Sales rose a humble 0.3%, while Consumer Confidence rose 3.5%.

- Stock Markets: The S&P closed at another all-time high of 4,793.

- The Omicron Variant careened thru the US and World catching everyone off guard with its rapid transmissibility but mild symptoms. Interest Rates and Fed Watch

Interest Rates and Fed Watch

The last FOMC Meeting of 2021 wrapped up on December 15th. In the FOMC Announcement, the Fed stated they would conduct a faster wind-down of its Bond-Buying Program with an expected end in March. They also announced they will get more aggressive dealing with Inflation - meaning they will raise Interest Rates. If you remember 12 months ago, the Fed said they weren't going to raise Interest Rates until 2023 - or later. That all changed. To deal with runaway Inflation, they have to raise rates sooner and anticipate three 1/4% Rate hikes in 2022. The Fed has a dual mandate: Price Stability and Full Employment. In 2021 the Fed focused on Employment and let Inflation run. In 2022, they will focus on containing inflation. Monetary Policy is not the only driver of Inflation. I don't think anyone (including the Fed) expected that the Pandemic would create such a huge supply chain disruption. Supply Chain Problems are exacerbating Inflation, so we can't blame Monetary Policy alone. The next FOMC meeting is on January 25th and 26th.

- 10 Year Treasury Security Yield: rose to 1.52% (Dec 30) from 1.43% (Nov 30).

- 30 Year Fixed Mortgage was unchanged at 3.11% (Dec 30) from 3.11 (Dec 02).

- 15 Year Fixed Mortgage fell to 2.33% (Dec 30) from 2.39% (Dec 02).

- 5/1 ARM Mortgage fell to 2.41% (Dec 30) from 2.4% (Dec 02).

Housing Market Data Released in December 2021

2021 will wrap up the year with Home Prices rising about 20%. In real terms, Home Prices, after being adjusted for Inflation, are higher than in 2007. How high will Home Prices go in 2022? Estimates are all over the board, 2% - 14%, but the consensus seems to be in the 5% - 8% range. During December, like all of 2021, the Housing Market was plagued by the same problem - low inventory. However, there are now more Homes under construction than in the last 10 years. Supply will eventually catch up to demand, but that probably won't happen in 2022 or 2023. Expect the Home Inventory issues to persist for the near future.

- Existing Home Sales (closed deals in November) rose 1.9% to an annual rate of 6,346,000 homes, down 2.0% in the last 12 months. The median price for all types of homes is $353,900 - up 13.9% from a year ago. The median Single-Family Home price is $362,600 and $283,200 for a Condo. Homes were on the market for an average of 18 days, and 83% were on the market for less than a month. Currently, 1,110,000 homes are for sale, down 13.3% from 1,280,000 units a year ago.

- New Home Sales (signed contracts in November) rose 12.4% to a seasonally adjusted annual rate of 744,000 homes - down 14.0% YoY. The median New Home price rose to $416,900 from $407,700 the prior month. The average price rose to $481,700 from $477,800 the prior month. There are 402,000 New Homes for sale, which is a 6.5 month supply.

- Pending Home Sales Index (signed contracts in November) fell 2.2% to122.4 from 125.3 the previous month, down 2.7% YoY.

- Building Permits (issued in November) rose 3.6% to a seasonally adjusted annual rate of 1,712,000 units - up 0.9 YoY. Single-Family Permits rose 2.7% to an annual pace of 1,108,000 homes, down 4.5% YoY.

- Housing Starts (excavation began in November) rose 11.8% to an annual adjusted rate of 1,679,000, up 8.3% YoY. Single-Family Starts rose 11.3% to 1,173,000 units, up 10.7% YoY.

- Housing Completions (completed in November) rose 4.1% to an annual adjusted rate of 1,282,000 units - up 3.1% YoY. Single-Family Completions fell 0.1% to an annual adjusted rate of 910,000 homes - up 12.2% YoY.

- S&P/Case-Shiller 20 City Home Price Index rose 0.9% in October, up 18.4% YoY.

- FHFA Home Price Index rose 1.1% in October, now up 17.4% YoY.

Labor Market Economic Data Released in December 2021

The Economy created 210,000 new jobs in November, falling way short of expectations of 515,000. There are 11,000,000 job openings and 6,500,000 people Unemployed. So, every Unemployed worker could have 2 jobs, if they wanted. Companies are desperate for workers, so why isn't Job Creation bigger? Lots of theories - too many to address in this short review. However, look at the Labor Force Participation Rate. It has fallen below 62%. That level hasn't been seen since the 1970s. The question should be: why are so many able-bodied workers not in the Labor Force?

- The Economy created 210,000 New Jobs during November.

- The Unemployment Rate fell to 4.2% in November from 4.6% in October.

- The Labor Force Participation Rate rose to 61.8% from 61.6% in October.

- The Average Hourly Wage rose 0.3% in November, now up 4.8% YoY.

- Job Openings rose to 11,033,000 in October.

Inflation Economic Data Released in December 2021

Inflation dominated the Economic headlines in 2021. The December CPI clocked Inflation at a 6.8% annual rate - the highest in 40 years. PPI was worse at 9.6% YoY. The big culprits were the cost of shelter, gasoline, food, and cars. Everyone is blaming the Fed for letting Inflation get out of control. However, the reasons why shelter, energy, cars, and food prices skyrocketed are due more to Supply Chain Disruption than Monetary Policy. Today's high Inflation is multifaceted and can't be blamed entirely on loose Monetary Policy. Hopefully, distribution problems will resolve by mid-year, and Inflation should start abating.

- CPI rose 0.8%, up 6.8% YoY | Core CPI rose 0.5%, up 4.9% YoY

- PPI rose 0.8 %, up 9.6% YoY | Core PPI rose 0.7%, up 6.9% YoY

- PCE rose 0.6%, up 5.7% YoY | Core PCE rose 0.5%, up 4.7% YoY

GDP Economic Data Released in December 2021

The 3rd and Final estimate of 3rd Quarter GDP showed the US economy grew at a 2.3% annualized rate (a slight revision from last month's 2.1%). The economy continues to grow at about a 5.0% annual rate. However, GDP growth did slow from the 2nd Quarter growth rate of 6.5%. Personal Consumption Expenditures (Consumer Spending) was down significantly and a major reason 3rd quarter is trailing below 2nd quarter. Consumers spent less on a number of manufactured goods (particularly vehicles), and services (mostly bars, restaurants, and hotels).

Consumer Economic Data Released in December 2021

Consumers slowed down their buying in November as Retails Sales rose only 0.3% for the month. However, Retail Sales for the past 12 months are up 18.2%. Consumers were on a buying binge in 2021, but they were also paying more for goods. Retail Sales data needs to be kept in context with Inflation data. Much of that 18.2% increase can be attributed to higher costs, especially higher energy costs. Consumers are spending more money to heat their homes and fuel their cars. Gas Station Sales increased 52.3% in the last 12 months. Most of that 52% increase is the higher cost of gasoline rather than Consumers buying more gallons.

- Retail Sales rose 0.3% during November, now up 18.2% in the last 12 months.

- Consumer Confidence Index rose 3.5% to 115.8 from 111.9 the previous month.

- Consumer Sentiment Index (U of M ) rose to 70.4 from 67.4 the previous month.

Energy, International, and Things You May Have Missed

Oil prices rose as several oil-producing countries are intentionally restricting production.

- West Texas Intermediate Crude rose to $76/barrel (Dec 30) from $67/barrel (Nov 30).

- North Sea Brent crude rose to $78/barrel (Dec 30) from $70/barrel (Nov30).

- Natural Gas fell to $3.7/MMBtu (Dec 30) from $4.58/MMBtu (Nov 30). Natural gas prices tumbled as US LNG cargo ships were redirected from Asia to Europe.

- Turkish Economic Troubles - Inflation is over 21%, and the Lira has fallen 54% in 2021.

- Olaf Scholz became the new Chancellor of Germany, replacing Angela Merkel, who had been Chancellor since 2005.

- NASA launched the James Webb Space Telescope - the largest and most powerful telescope to ever leave Earth.

The Mortgage Economic Review is a concise summary of Key Economic Data that influences the Mortgage and Real Estate Industries. It's a quick read that keeps busy Professionals updated on important Economic Information. Feel free to share this with friends and colleagues in the Mortgage and Real Estate business. To have the Mortgage Economic Review emailed to you each month, click here.

Discover new lending opportunities at MortgageElements.com, where you can explore over 300 Wholesale, Correspondent, Warehouse, Reverse, Construction, and Rehab Mortgage Lenders, from one website. Use the Mortgage Periodic Table to research Mortgage Products, view Underwriting Guidelines, and connect with Wholesale and Correspondent Account Executives - it costs nothing to use and is one of the industry's largest databases of TPO Mortgage Lenders.

Mark Paoletti, MortgageElements.com

The Mortgage Economic Review is for informational and educational purposes only and should not be construed as investment, legal, financial, or mortgage advice. The information is gathered from sources believed to be credible; some are opinion-based and editorial in nature. Mortgage Elements Inc does not guarantee or warrant its accuracy or completeness, and there is no guarantee it is without errors. This newsletter is created for use by Mortgage and Real Estate Professionals and is not an advertisement to extend credit or solicit mortgage originations. © Copyright 2022 Mark Paoletti, Mortgage Elements Inc, All Rights Reserved.