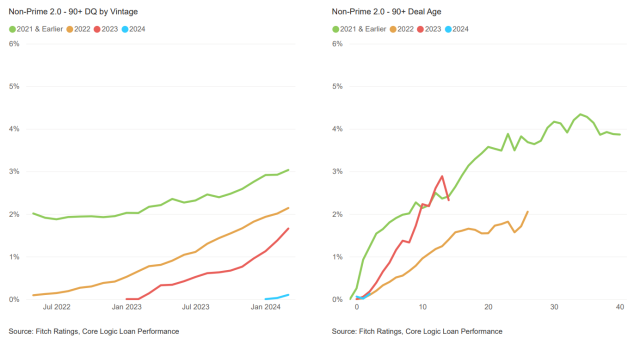

The average delinquency rate for a non-QM, 2023-vintage transaction four months after issuance is 3.2%, almost twice as high as the 2022 vintage, according to Fitch Ratings’s most recent U.S. RMBS Performance Chartbook, released last week.

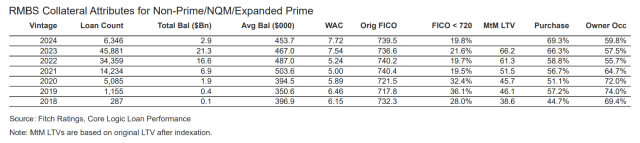

The 2023 vintage represents nearly $22 billion of outstanding balance in Fitch's current Non-Prime rated portfolio.

The prime sector has also experienced an uptick in early (30-plus day) delinquencies. Court Lake, senior director of structured finance at Fitch Ratings and lead analyst on the report, said in an interview with NMP that he will be watching to see how many of those loans roll into serious (90-plus day) delinquencies.

“We’ve been highlighting the trends within the Non-Prime/NonQM space. The increase in delinquencies have been evident over the last nine months or so,” Lake explains. “But, now you’re starting to see a slight uptick in 30-plus delinquencies for Prime. We want to see how that 30-plus delinquencies translates to more of a serious delinquency rate.”

However, the more troubling finding from the report was one that wasn’t new – a persistent trend in rising delinquencies among Non-QM/Non-Prime borrowers. The share of Non-Prime loans in 30-plus and 90-plus day delinquencies stands at 5.2% and 2%, respectively, the result of sustained upticks over recent months.

“Between 2020 and 2022 there was significant home price gains,” says Lake. “I think you look at the, the labor market and you’re still seeing a very low unemployment rate, so that’s supporting these Non-Prime borrowers. In terms of the increase in delinquencies,” he continues, “I think it’s a combination of what we highlighted in our report last quarter with seeing some worse collateral attributes about borrowers. And then you’re probably just seeing also some more macroeconomic pressure in the segment of borrowers, especially in the lower income segments.”

Serious delinquencies in the Non-Prime sector have been steadily increasing through the past year for all vintages.

In terms of new issuance, the Non-QM/Non-Prime sector remains the most active in RMBS sectors.

Within Fitch's rated portfolios, Non-QM/Non-Prime issuance increased more than 800% from 2020 through 2023. As a proxy for loan production, the total balance of Fitch's rated Non-QM/Non-Prime portfolio has skyrocketed: $1.9 billion for 2020 vintages, $6.9 billion for 2021, $16.6 billion for 2022, and $21.3 billion for 2023.

Meanwhile, the percentage of borrowers with FICO scores under 720 in Fitch's Non-QM/Non-Prime RMBS pools has decreased from roughly one-third to roughly one-fifth over the past four years, suggesting the underlying collateral for these securitizations has improved.

This growth in Non-QM/Non-Prime sectors has occurred amid a major drop-off in Prime sector originations and issuance in 2022's and 2023's higher-interest-rate environment. For comparison, the collateral attributes of Fitch's rated Prime RMBS show:

Yet, Fitch attributes the deteriorating loan performance in 2023 vintages to weaker collateral attributes such as lower FICO scores, higher combined loan-to-value ratios, fewer full-documentation-type loans, higher mortgage rates, and higher debt-to-income ratios. Many collateral attributes were at their weakest between the second and fourth quarters of 2022 when loans that were securitized in 2023 RMBS pools were originated, driving elevated delinquency rates for the 2023 vintage.

For example, weighted average FICO scores decreased to 732 in the third quarter of 2022 from 742 in the third quarter of 2021 at the same time that loan concentrations shifted to lower FICO buckets with higher delinquency rates.

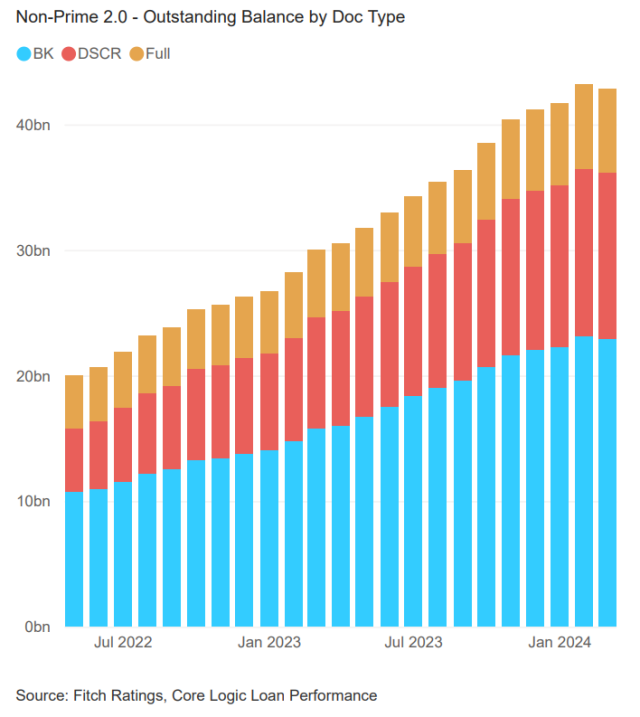

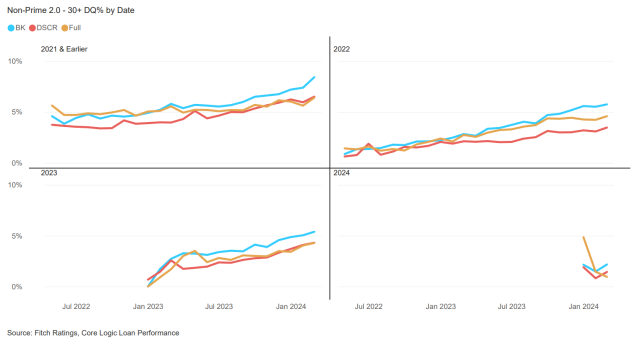

Loans underwritten to bank statements have had the greatest increase in concentration within Fitch’s rated Non-Prime transactions since mid-2022, but are also the greatest area of concern within the Non-Prime sector.

Bank statement products have had the highest share of 30-plus day delinquencies among all vintages. However, "right now," Lake says, “the performance is still below our stressed assumptions.”

Whereas the weaker underwriting standards of less-than-full-doc, bank statement loans has likely been the root of that segment’s weaker loan performance, says Lake, the strong performance of DSCR loans – which are only underwritten to cash flows, not income – has been a surprise.

“The performance in the DSCR space has really been excellent and outperformed our expectations,” he says. “We think it’s driven by a supportive home price environment as well as the continued increase in rental prices and rents throughout the country.”

Meanwhile, Fitch expects borrower performance to continue to be pressured in 2024 as the effects of elevated interest rates pass through the economy and real income growth slows. A strong job market has bolstered borrowers, but declining affordability and the rising costs of insurance, taxes, and utilities have added pressure to borrowers' ability to make their monthly payments.

And yet, despite collateral headwinds, Non-QM producers may be starting to turn things around in 2024.

“We actually just received the latest remit report data for the most recent payday, and we actually saw a slight decrease in impairments and delinquencies, so I think we’re starting to see more improved performance and what we’ve seen from issuances over the last four months,” said Lake. “Through 2024, we’re actually seeing a better collateral profile. We’re expecting, from all the deals that have been going out, lower expected losses. We’re starting to see a return to tighter, more improved collateral that’s being issued in the Non-QM space.”