Average fixed mortgage rates rose for the third consecutive week–and the costs of borrowing for a lower amount home loan are also on the uptick.

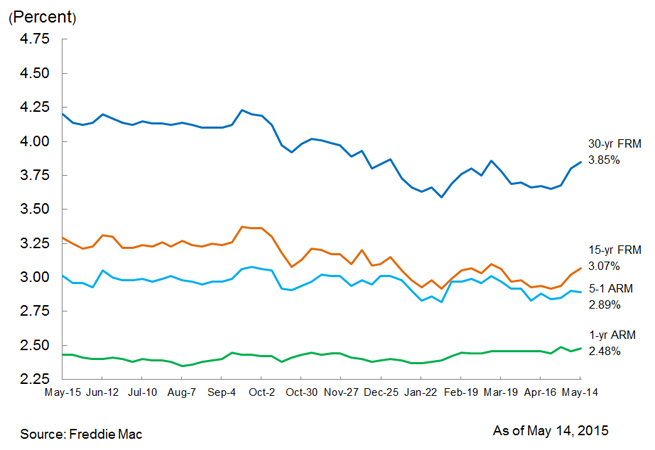

On the rates front, Freddie Mac’s latest Primary Mortgage Market Survey (PMMS) found the 30-year fixed-rate mortgage (FRM) averaged 3.85 percent with an average 0.6 point for the week ending May 14, up from last week when it averaged 3.80 percent but down from the 4.20 percent average recorded a year ago. The 15-year FRM this week averaged 3.07 percent with an average 0.6 point, up last week’s average of 3.02 percent but down from the 3.29 percent level a year ago at this time.

Also, the five-year Treasury-indexed hybrid adjustable-rate mortgage (ARM) averaged 2.89 percent this week with an average 0.5 point, down from last week when it averaged 2.90 percent; last year at this time, it averaged 3.01 percent. And the one-year Treasury-indexed ARM averaged 2.48 percent this week with an average 0.4 point, up from last week when it averaged 2.46 percent; it is slightly below last year’s 2.43 percent average.

"Mortgage rates rose for the third consecutive week as 10-year Treasury yields continued to climb,” said Len Kiefer, deputy chief economist for Freddie Mac. “The labor market continues to improve with U.S. economy adding 223,000 jobs in April, a solid rebound from merely 85,000 job gains in March. Also, the unemployment rate dipped to 5.4 percent in April as the participation rate ticked up to 62.8 percent and jobless claims were far less than expected."

But Freddie Mac’s data offered little cheer to borrowers with low-loan amounts—according to a new Zillow study, they pay 10 percent more for every dollar than borrowers with high-loan amounts due to higher interest rates and fees. Zillow reported that the average interest rate offered on a $100,000 home loan in the first quarter of this year was 3.95 percent with an APR of 4.06 percent, while the average interest rate offered on a $400,000 home loan during the same period was 3.64 percent with an APR of 3.7 percent.

Furthermore, Zillow found that borrowers with small loan amounts have substantially fewer lenders willing to lend them money. Borrowers seeking a home loan for $100,000 received half as many loan quotes from lenders compared to those seeking loans for $400,000.

"Lenders go after big loan amounts and back-burner small loan amounts because even though they take the same amount of time to complete, the larger the loan amount is, the more a lender typically makes," said Erin Lantz, Zillow’s vice president of mortgages. "Since there is less competition for small loan amounts, lenders offer higher interest rates to help cover the costs and many low- to middle-income borrowers have no choice but to pay more."