In published remarks delivered Wednesday to the Exchequer Club, a Washington D.C.-based group professionally interested in national economic and financial policy, Acting Comptroller of the Currency Michael Hsu highlighted the urgency needed in addressing three long-term trends reshaping banking: the growing number and size of large banks, the complexity of bank-nonbank relationships, and polarization.

“These trends are underappreciated by the public because they are evolving incrementally,” Hsu said to the Club. “The issues they pose thus seem manageable. Left untended, however, they may lead to a painful reckoning in the future, similar to how shadow banking seemed to emerge from nowhere in 2008, even though it had been building for years” (Hsu’s emphasis).

Those surprises pose “deep threats to trust in banking and warrant our collective attention,” he said.

This synopsis of Hsu’s comments focuses specifically on the second trend Hsu warns about, the complexity of bank-nonbank relationships. These complexities create interdependencies between banks and nonbanks, Hsu explained, including fintechs, that blur the line between banking and commerce, specifically concerning payments.

Hsu delivered remarks in February 2024 at Vanderbilt University highlighting the same risks of "the next great blurring."

His comments examining this trend made on July 17 to the Exchequer Club have been condensed for length and clarity.

As the ascendency of financial engineering, derivatives, and structured finance turbocharged a rapid expansion of shadow banking, which played a direct and indirect role in the 2008 financial crisis, “a similar transformation is occurring in payments,” Hsu observed on Wednesday. Advancements in technology, combined with and facilitating the inevitable rise of online and mobile commerce, have hastened the digitalization of banking, with most of the innovation being led by nonbank financial technology firms (fintechs).

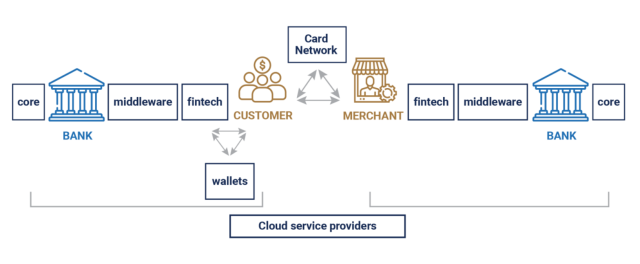

Customers and merchants are increasingly using fintechs for payments, lending, and deposit services. As a result, direct banking relationships are being replaced with long-intermediated chains of discrete services. By way of analogy, Hsu suggests that banking is beginning to resemble global manufacturing supply chains.

Fintechs partner with banks — sometimes indirectly through intermediaries or other “middleware” firms — to execute services offered. Banks, too, rely on a host of nonbank service providers such as core processors to support a range of operations and functions.

On a meta-layer, banks and nonbanks have grown increasingly reliant on large cloud service providers to support their digitization initiatives, as have corporations and governments. “The line between where a bank ends and where a nonbank begins is increasingly hard for consumers, regulators, and market participants to discern,” Hsu said, which he added then leads to the creation and distribution of risk in unclear ways. “This makes it challenging to know who is responsible for what.”

These bank-nonbank arrangements have highlighted the need for tailored federal payment regulation and supervision, Hsu believes. Opponents argue that state supervision of customer-facing nonbank fintechs has enabled innovation in the market. In response, Hsu insists that “none are supervised prudentially at the federal level,” which has enabled fintechs “to play fast and loose with how they market their services and their relationship to FDIC insurance, which does not cover their failures” (Hsu’s emphasis).

The risks from deposit arrangements and necessary controls may differ from those needed for payment arrangements, and further differences exist for lending arrangements between banks and nonbanks.