A new LendingTree analysis of homeownership data reveals persistent racial disparities in U.S. housing, with Black households owning a significantly smaller share of homes across the nation’s largest metropolitan areas.

The study underscores the structural and economic barriers that continue to limit Black Americans’ access to homeownership, a key driver of long-term wealth.

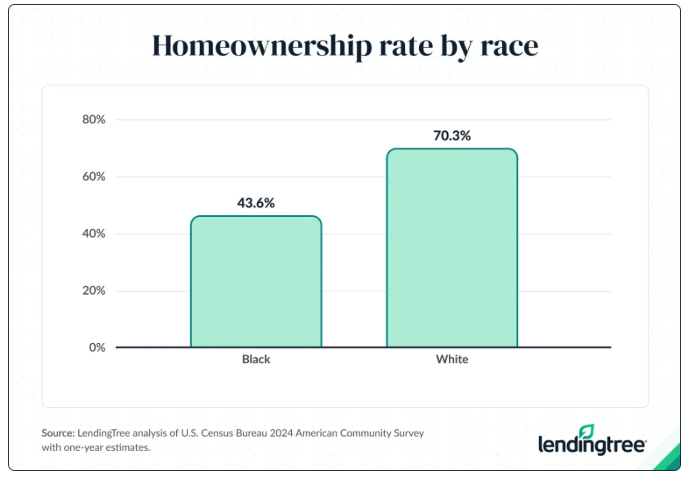

Across the 50 largest U.S. metropolitan statistical areas, the Black homeownership rate in 2024 was just 43.6%, compared with 70.3% among white householders, according to LendingTree’s analysis of 2024 American Community Survey (ACS) data. That equates to roughly 4.6 million homes owned by Black households in these major markets.

“Without sufficient income and decent credit, getting a home can be a major challenge, and Black Americans still trail well behind white Americans and other groups in those areas,” said Matt Schulz, LendingTree chief consumer finance analyst. “Until that changes, that gap will likely remain.”

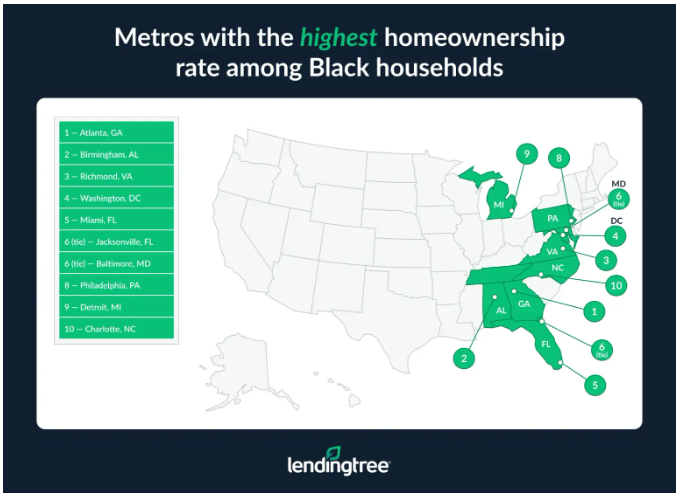

The gap persists despite Black Americans’ presence in many urban communities. Atlanta leads for Black homeownership among the largest metros, with a rate of 55.3%, followed by Birmingham, Alabama (54.1%); and Richmond, Virginia (52.8%). Washington, D.C. and Miami are the only other metros where Black homeownership exceeds 50%.

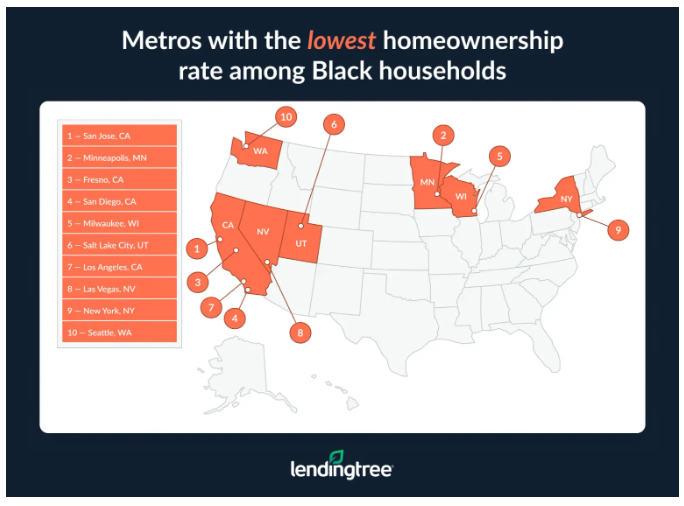

By contrast, costly housing markets show the lowest Black homeownership rates. San Jose, California, ranks at the bottom with just 29.2%, followed by Minneapolis, Minnesota (30.1%); and Fresno, California (30.5%). Larger expensive metros including Los Angeles, New York, and Seattle also fall in the bottom 10 for Black homeowners.

The study also highlights disparities in home values, as the median value of homes owned by Black Americans nationwide was $278,500 in 2024, roughly 22.8% below the overall national median home value of $360,600. LendingTree analysts attribute these differences in part to lower average income and credit scores among Black households, which can limit mortgage size and buying power.