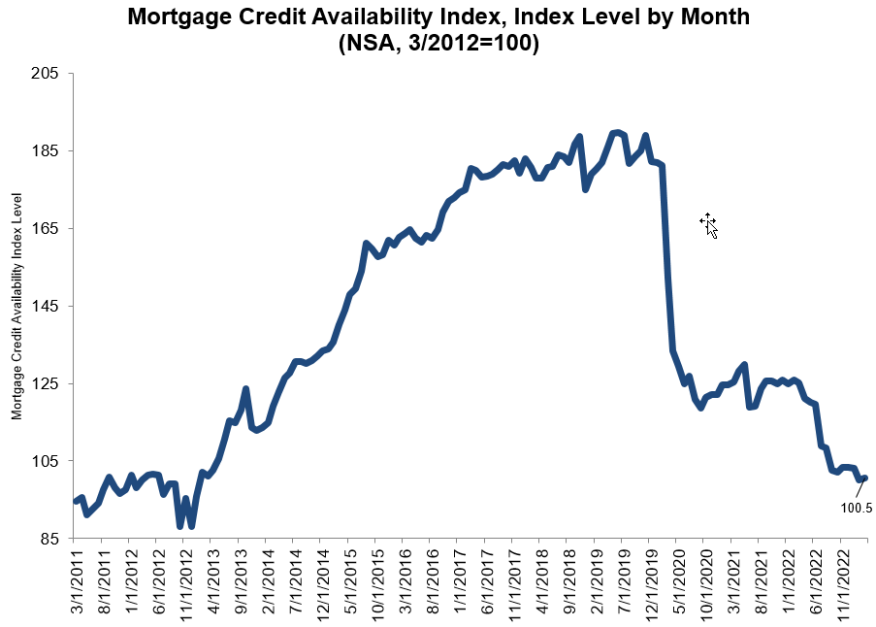

The availability of mortgage credit improved a bit in March, but credit remained at its tightest levels in 10 years, the Mortgage Bankers Association (MBA) said Tuesday.

The MBA released its monthly Mortgage Credit Availability Index (MCAI), a report that analyzes data from ICE Mortgage Technology.

The MCAI rose by 0.4% to 100.5 in March. An increase in the index indicates that lending standards are loosening, while a decrease indicates tightening credit. The index was benchmarked to 100 in March 2012.

The Conventional MCAI increased 1.1%, while the Government MCAI decreased by 0.2%, the MBA said. Of the component indices of the Conventional MCAI, the Jumbo MCAI increased 1.4% and the Conforming MCAI rose by 0.4%.

“Mortgage credit supply increased modestly in March but remained close to its tightest levels since 2013,” said Joel Kan, MBA’s vice president and deputy chief economist. “With the spring buying season underway, lenders are grappling with the threat of a recession and tighter overall financial conditions following the recent bank failures.”

Kan said the supply of government mortgage credit — which includes FHA and VA loans that many first-time homebuyers rely on — declined for the third time in four months, which could hinder first-time buyer activity.

“There was a small increase in credit availability for jumbo loans, with more programs offered for cash-out refinances,” he said. “However, we expect banks, which account for most of the jumbo market, will tighten jumbo credit criteria in response to recent challenges in the banking sector.”

The conventional, government, conforming, and jumbo MCAIs are constructed using the same methodology as the Total MCAI. They are all designed to show relative credit risk/availability for each index.

The primary difference between the total MCAI and the component indices are the population of loan programs which they examine, the MBA said. The Government MCAI examines FHA/VA/USDA loan programs, while the Conventional MCAI examines non-government loan programs. The Jumbo and Conforming MCAIs are a subset of the conventional MCAI and do not include FHA, VA, or USDA loan offerings. The Jumbo MCAI examines conventional programs outside conforming loan limits, while the Conforming MCAI examines conventional loan programs that fall under conforming loan limits.

The Conforming and Jumbo indices have the same “base levels” as the Total MCAI (March 2012=100), while the Conventional and Government indices have adjusted “base levels” in March 2012.

MBA said it calibrated the Conventional and Government indices to better represent where each index might fall in March 2012 (the “base period”) relative to the Total=100 benchmark.

The MCAI provides the only standardized quantitative index that is solely focused on mortgage credit, the MBA said. It is calculated using several factors related to borrower eligibility (credit score, loan type, loan-to-value ratio, etc.). The metrics and underwriting criteria for over 95 lenders/investors are combined by MBA using data made available via ICE Mortgage Technology and a proprietary formula derived by MBA to calculate the MCAI, a summary measure that indicates the availability of mortgage credit at a point in time. Base period and values for total index is March 31, 2012=100; Conventional March 31, 2012=73.5; Government March 31, 2012=183.5.