The Mortgage Bankers Association says there was a three basis point decrease in the total number of loans in forbearance. As of November 30, 2023, the forbearance rate stands at 0.26%, down from 0.29% in the previous month.

MBA's estimates indicate that approximately 130,000 homeowners are currently in forbearance plans. Since March 2020, mortgage servicers have extended forbearance to around 8.1 million borrowers.

In November 2023, the share of Fannie Mae and Freddie Mac loans in forbearance decreased by two basis points to 0.16%. Ginnie Mae loans in forbearance saw a five basis point drop to 0.47%, while the forbearance share for portfolio loans and private-label securities (PLS) decreased by two basis points to 0.30%.

“Nearly 96 percent of all home mortgages are performing, which underscores how strong servicing portfolio performance is right now with the same resilience seen in the U.S. labor market,” said Marina Walsh, CMB, MBA’s vice president of industry analysis. “Meanwhile, the performance of loan workouts is solid, but declined last month. Roughly 70 percent of loan workouts initiated since 2020 are current.”

She added, “MBA forecasts an economic downturn in 2024, and there are signs of early distress in other credit types such as car loans and credit cards. Those borrowers who struggled in making their mortgage payments in the past may find themselves in similar situations in a softening economy and rising unemployment.”

By investor type, Ginnie Mae loans in forbearance decreased to 0.47% relative to the previous month, while Fannie Mae and Freddie Mac loans dropped to 0.16%. Other loans, such as portfolio and PLS loans, decreased to 0.30%.

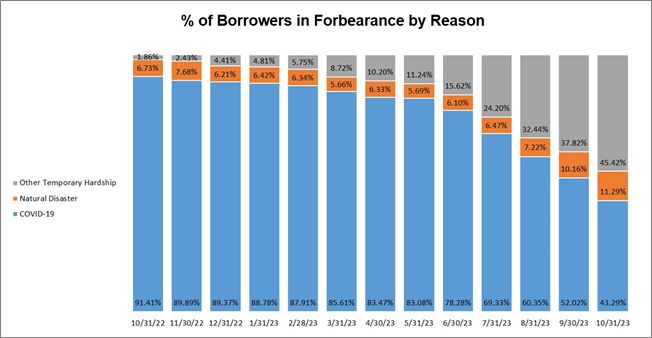

Regarding the reasons for forbearance, 53.6% of borrowers are in forbearance due to temporary hardships like job loss, death, divorce, or disability. Another 34.3% are in forbearance due to COVID-19, and 12.1% are in forbearance due to natural disasters.

By stage, 49% of total loans in forbearance are in the initial forbearance plan stage, with 35.1% in a forbearance extension. The remaining 15.8% represents forbearance re-entries, including re-entries with extensions.

The report also highlights the outcomes of cumulative forbearance exits from July 1, 2020, through November 30, 2023. Notable results include 29.4% resulting in a loan deferral/partial claim, 17.7% where borrowers continued to make monthly payments during forbearance, and 16.1% resulting in loan modifications or trial loan modifications.

Total loans serviced that were current as a percent of servicing portfolio volume decreased slightly to 95.71% in November 2023 from 95.80% in October 2023.