Identity and transaction fraud rise for the second consecutive year, CoreLogic reports

The CoreLogic Mortgage Application Fraud Risk Index increased 8.3% nationwide over last year and increased by 1.1% since last quarter. Overall, the CoreLogic report found that one in 123 mortgage applications were estimated to have indications of fraud in the second quarter of 2024.

Driving Factors

In reviewing trends among six fraud types, the 2024 CoreLogic fraud report found identity fraud and transaction fraud were the two with an increase over the previous year.

Identity fraud is reported less frequently in the industry, and is rarely mirrored in the Fannie Mae fraud trend reporting. Yet, identity fraud risk indicators have increased for two straight years, up 5.5% year-over-year in 2024 and up 12% the year prior. Researchers believe this is due to the rise in ITIN (Individual Tax Identification Numbers) loan programs for people who do not have Social Security Numbers.

Transaction fraud risk, on the other hand, has appeared more frequently with indicators increasing 4.9% in 2024 after increasing 1.9% last year. CoreLogic ties the rising trend to upticks in rapid resales with rising prices, more high-activity buyers, and sales transactions with multiple high-risk flags. Elements of those transactions, such as down payments, property uses, or non-arm's-length relationships, are more likely to be misrepresented.

Property fraud risk and income fraud risk were down 1.8% and 2%, respectively, from last year. Occupancy fraud risk and undisclosed real estate debt fraud risk were down 3.9% and 6%, respectively.

Get the NMP Daily

Essential stories, every weekday.

High interest rates have kept mortgage volume in check, CoreLogic reports, with the refinances share of activity staying between 24% and 27.5% since mid-2022. Meanwhile, purchase transactions as a share of overall volume were 74.3% in the second quarter of 2024, hardly changing from last year.

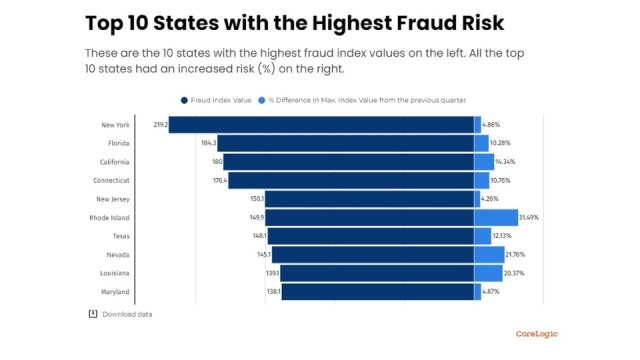

Risky States For Fraud

Number one on the list for having the most fraud risk is New York, up 4.8% from last year, due to its high concentration of above-average risk loans, including two- to four-unit loans, FHA purchases, and investment purchases.

Next is Florida, which has shown increased risk in FHA purchases in the past two years, with the overall state risk increasing 10.2% in the last year. Following in third is California, which had the largest overall risk increase of 14.6%, nearly double the national increase rate. The increase was distributed across loan segments.

Coming in fourth is Connecticut, where risk levels are largely due to investment loans — both purchase and refinance — which are at higher risk levels and in higher volumes than national averages. Overall risk was up 10.8%. In fifth, New Jersey had the smallest increase of the top five states, at 4.3%. Its risk level is impacted by higher-risk two- to four-unit purchases and refinances.

CoreLogic data showing the top 10 states with the highest fraud risk index in 2024.

The company expects to begin purchasing fixed-rate HELOCs from correspondent lenders during the third quarter

Achieve has completed a $261.5 million securitization backed by 3,129 fixed-rate home equity lines of credit as it prepares to begin purchasing HELOCs from correspondent lenders.ACHM Trust 2026-HE1 closed July 30 and was announced Aug. 6. It is Achieve’s first HELOC securiti...

Platform volume overtook DTC, but costly enterprise integrations have yet to deliver, and new partnership growth is not expected until Q4

Better Home & Finance will miss its goal of reaching adjusted EBITDA break-even by the end of September, interim CEO Daniel Lewis acknowledged during his first earnings call leading the company.Rather than set another deadline, Lewis said Better must first show that it c...

Home equity and purchase lending lifted production economics, while management characterized its relaunched wholesale channel as a supporting business rather than a major growth engine

Pending sales fell to their lowest level since early April, but lower asking prices and reduced competition give originators more options to structure deals for qualified borrowers