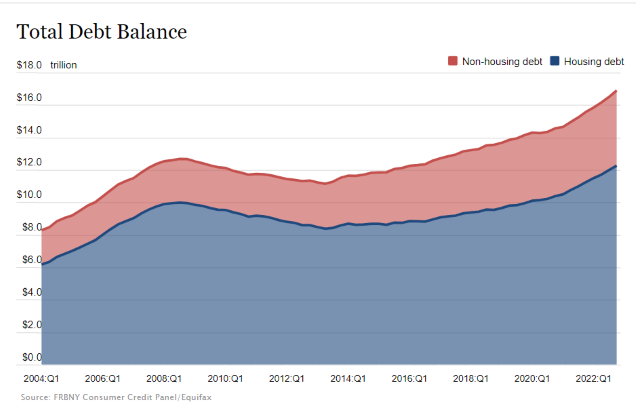

Total household debt in the fourth quarter of 2022 increased $394 billion, or 2.4%, to $16.9 trillion — $2.75 trillion higher than at the end of 2019, according to a report released Friday by the Federal Reserve Bank of New York.

The Quarterly Report on Household Debt and Credit, from the bank’s Center for Microeconomic Data, is based on data from its nationally representative Consumer Credit Panel.

According to the report, mortgage balances rose by $254 billion in the fourth quarter and stood at $11.92 trillion at the end of December, a nearly $1 trillion increase in mortgage balances in 2022.

Credit card balances increased $61 billion in the quarter to $986 billion, surpassing the pre-pandemic high of $927 billion, the report states. Auto loan balances increased by $28 billion in the quarter, while student loan balances now stand at $1.60 trillion, up by $21 billion from the previous quarter. In total, non-housing balances grew by $126 billion.

Mortgage originations, which include refinances, fell to $498 billion in the fourth quarter, representing a return to lower levels last seen in 2019, before the COVID-19 pandemic, the bank said.

The share of current debt becoming delinquent increased again in the fourth quarter for nearly all debt types, following two years of historically low delinquency transitions. The delinquency transition rate for credit cards and auto loans increased by 0.6 and 0.4 percentage points, respectively.

The report also noted that, while the pandemic foreclosure moratoria have been lifted nationally, new foreclosures have stayed very low since the CARES Act moratorium was put into place. About 34,000 individuals had new foreclosure notations on their credit reports, the bank said.

“Credit card balances grew robustly in the 4th quarter, while mortgage and auto loan balances grew at a more moderate pace, reflecting activity consistent with pre-pandemic levels,” said Wilbert van der Klaauw, economic research advisor at the New York Fed. “Although historically low unemployment has kept consumer's financial footing generally strong, stubbornly high prices and climbing interest rates may be testing some borrowers' ability to repay their debts.”