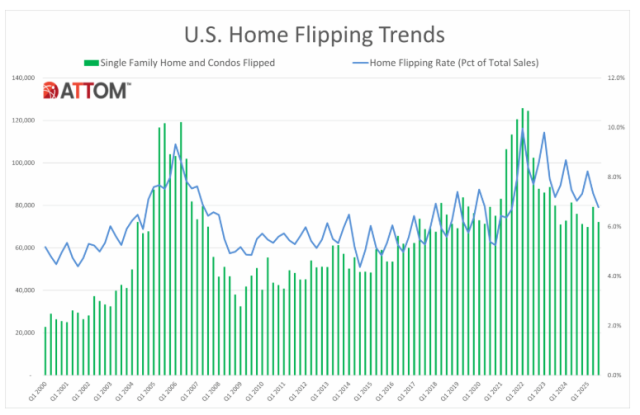

ATTOM’s Q3 2025 U.S. Home Flipping Report reveals continued contraction in the nation’s house‑flipping market, with profitability sliding to levels not seen since the run‑up to the 2008 financial crisis.

According to the report, 72,217 single‑family homes and condominiums were flipped nationwide during the third quarter (July through September), representing just 6.8% of all home sales — a decline from both the prior quarter and year‑ago results.

“Home flipping activity and profitability continued to decline in Q3 2025 with typical return on investment dropping to 23.1%, the lowest since 2008,” said Rob Barber, CEO of ATTOM. “Rising home prices and shrinking margins have made flipping increasingly challenging. What was once a flipping market that consistently delivered 40%–60% returns for more than a decade, beginning in 2009, has now settled into five straight quarters of returns in the 20% range. Investors must choose their markets more carefully as the game has fundamentally changed.”

A defining feature of the Q3 2025 report is the sharp drop in investor returns. The typical return on investment for a flipped property was 23.1%, down from 26.5% in Q2 2025 and 29.8% in Q3 2024. This marks the lowest profit margin observed in any quarter since 2008, reflecting persistent upward pressure on home acquisition costs amid historically high home prices. Gross profits also contracted: the median flip generated approximately $60,000 in gross profit — notably below prior periods.

The data also highlight geographic disparities. Southern metro areas such as Columbus, Georgia (13.5% of sales); Tuscaloosa, Alabama (12.1%); and Spartanburg, South Carolina (12.0%) recorded the highest rates of flipping activity, whereas markets including Seattle, Washington (3.9%) and Rochester, New York (4.6%) exhibited relatively low flip rates.

Profitability varied widely across metros: while a minority of areas posted typical returns exceeding 50% — including Lynchburg, Virginia and Scranton, Pennsylvania — several large Texas markets showed single‑digit flips margins.

ATTOM’s analysis underscores the evolving challenge for investors in a market where rising prices, extended holding periods, and renovation costs are compressing returns, prompting more selective investment strategies amid a backdrop of tightening profit margins.