Single-family rent (SFR) growth across the U.S. continues to moderate, reaching levels not seen in more than a decade, according to the latest Cotality Single-Family Rent Index (SFRI) for October 2025. The national index shows a year-over-year rent increase of just 0.9%, significantly lower than the 2.8% gain recorded in October 2024, and marking the fourth consecutive month of deceleration.

“Forty of the largest 50 metros posted lower annual rent growth compared to October 2024. Eighteen metros saw outright year-over-year declines in the Single-Family Rent Index, with half of those declines occurring in Florida,” said Molly Boesel, senior principal economist at Cotality. “While this moderation is notable, rents remain elevated compared to pre-pandemic levels. Annual growth peaked in March 2022, and even after three years of slowing, the national index in October was still 9% higher than the 2022 average level. This trend reflects a normalization process rather than a reversal, as affordability challenges and regional dynamics continue to shape rent performance.”

Market Overview

The slowdown is broad-based: 40 of the largest 50 U.S. metros reported lower annual rent growth compared to last year, and 18 metros experienced outright year-over-year declines, with half of those decreases occurring in Florida markets. Despite the moderation, rent levels remain elevated relative to pre-pandemic norms, and the national index in October still stood roughly 9% above the 2022 average.

Regional and Segment Variations

Chicago led major markets with the strongest rent growth at 4.6%, followed by Washington, D.C. (2.4%) and Detroit (2.4%).

Dallas posted the weakest performance, with single-family rent declining by 1.3% year-over-year.

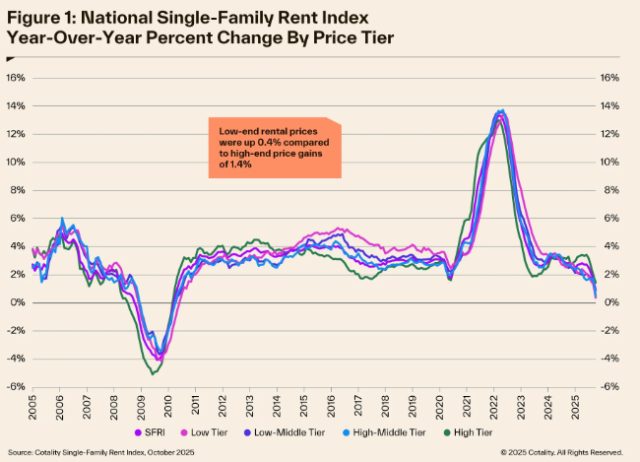

From a property class perspective, higher-end rentals grew 1.4%, while lower-end units rose only 0.4% — a steeper deceleration for more affordability-sensitive segments.

"For mortgage brokers working with investor clients, the 'normalization' of the market is a sign of long-term health," noted Kyle Concannon, VP of Product & Wholesale, Constructive Capital. "While the explosive rent growth of previous years has cooled, the fact that rents are not 'reversing' (outside of specific correction markets like Florida) suggests a stable environment for rental property acquisitions. Brokers can help investors find opportunities in resilient 'Midwest metros' like Chicago and Detroit, which continue to lead the nation in growth."

Implications for the Marketplace

- Demand Dynamics May Shift Toward Ownership: Slower rent growth can improve affordability for prospective buyers contemplating a transition from renting to ownership, particularly in markets where rental cost inflation has been a barrier. As rent increases flatten, the relative cost of monthly mortgage payments (adjusted for prevailing rates) may appear more competitive for qualified borrowers, potentially stimulating purchase demand in select metros.

- Price Sensitivity Among Borrowers: Mortgage originators should be alert to increased price sensitivity among first-time and lower-income buyers, who may feel more empowered to pursue homeownership when rent growth cools, especially if wage trends remain supportive. However, persistent high mortgage rates and elevated home prices continue to constrain affordability for many. Originators may need to tailor mortgage solutions (e.g., adjustable-rate products, first-time buyer programs) to align with borrower affordability profiles.

- Underwriting and Risk Considerations: The deceleration in rent growth could influence rent-assumption underwriting models and debt-service coverage ratio (DSCR) evaluations for investment property loans. With rent growth slowing and even declining in certain metros, cautious assessment of projected rental income is recommended, especially for DSCR loans where cash flow relies heavily on rent covering payment obligations. Recent industry reports also suggest rising DSCR delinquencies in some investment segments, underscoring the importance of conservative underwriting assumptions.

- Regional Market Nuances Require Localized Strategies: The uneven nature of rent trends — with markets like Chicago outperforming while others, such as Dallas and some Florida metros, weaken — reinforces the need for local market intelligence in originations strategy. Tailored outreach, pricing, and product positioning that reflect metro-specific rent and affordability dynamics can help originators better capture demand where it is strengthening.

- Broader Housing Market Context: The rental market trend complements other housing indicators. National rent growth slowing to a 15-year low reflects broader supply/demand adjustments following post-pandemic volatility; however, rents remain historically elevated. Combined with low for-sale inventory and a persistent “lock-in” effect among existing homeowners reluctant to relinquish low mortgage rates, housing turnover remains constrained. This macro backdrop should inform originator expectations around pipeline velocity, refinancing dynamics, and purchase activity.