Single‑family rent growth continued its multi‑month deceleration nationwide in November 2025, according to the latest Single‑Family Rent Index (SFRI) from Cotality, a property information and analytics provider. The national index showed annual rent growth of 1.1%, down substantially from the 2.5% increase recorded between November 2023 and November 2024.

The November data marks the fifth consecutive month of slowing annual rent gains, reflecting a broad easing in rental market pressures after years of rapid increases. Senior Principal Economist Molly Boesel described the slowdown as “the weakest pace in more than 15 years,” signaling a notable cooling in single‑family rental demand.

Despite the slowdown, rent levels remain significantly higher than in prior years. Over the past five years, cumulative rent increases across price and property type tiers have hovered around the 27%–28% mark, underscoring continued affordability challenges for many households. For example, in high‑growth markets such as Miami, rents have risen approximately 51% over that period — nearly double the national average.

“Rent growth slowed to its weakest pace in more than 15 years, signaling a broad-based cooling across the U.S. rental market as the market is adjusting after years of rapid increases,” said Boesel. “While Miami, Houston, and Dallas posted annual declines, rents remain significantly higher than five years ago. Miami alone is up 51%, nearly double the national average of 27%. The slowdown in rent growth is widespread: 43 of the 50 largest metros are seeing weaker growth than a year ago, and 16 are registering outright decreases. Florida leads in annual declines, while Chicagoland metros top the list for increases. Even high-end rentals, which posted the strongest annual gains, show long-term growth converging across all price tiers, reflecting normalization across segments."

The deceleration trend was widespread but uneven across metropolitan areas. Among the 10 largest U.S. metros, Chicago posted the highest year‑over‑year rent growth at 4.2%, followed by Philadelphia (2.8%), Detroit (2.7%), New York‑Jersey City‑White Plains (2.3%), and Los Angeles (2.1%).

Conversely, several major markets registered annual rent declines: Dallas (-0.8%), Houston (-0.7%), and Miami (-0.5%).

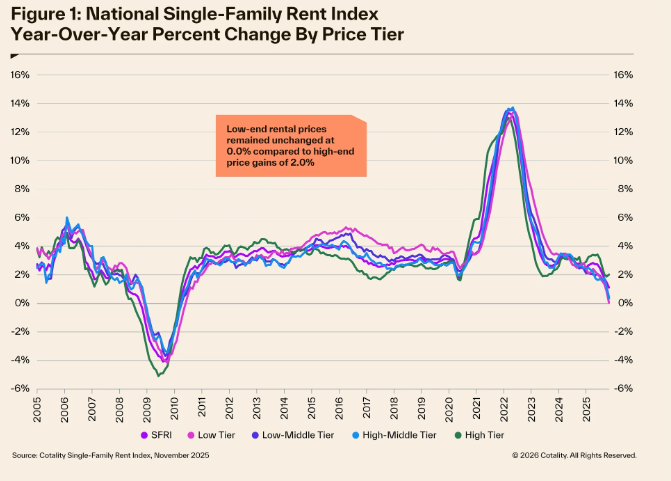

The slowing pace extended across property tiers and types. High‑end rents increased 2.0%, down from last year’s 2.7% gain, while low‑end rents showed no annual increase in November — falling from a 2.8% gain the prior year. Detached rents rose 0.8%, and attached rentals increased 1.1%.

Cotality’s report concludes that while single‑family rent growth remains positive in most regions, the pace of increases has decelerated significantly, pointing to a normalization of rental market conditions following historic rent inflation.