Today’s housing data news offered surprises—some pleasant, some not—on new highs and lows.

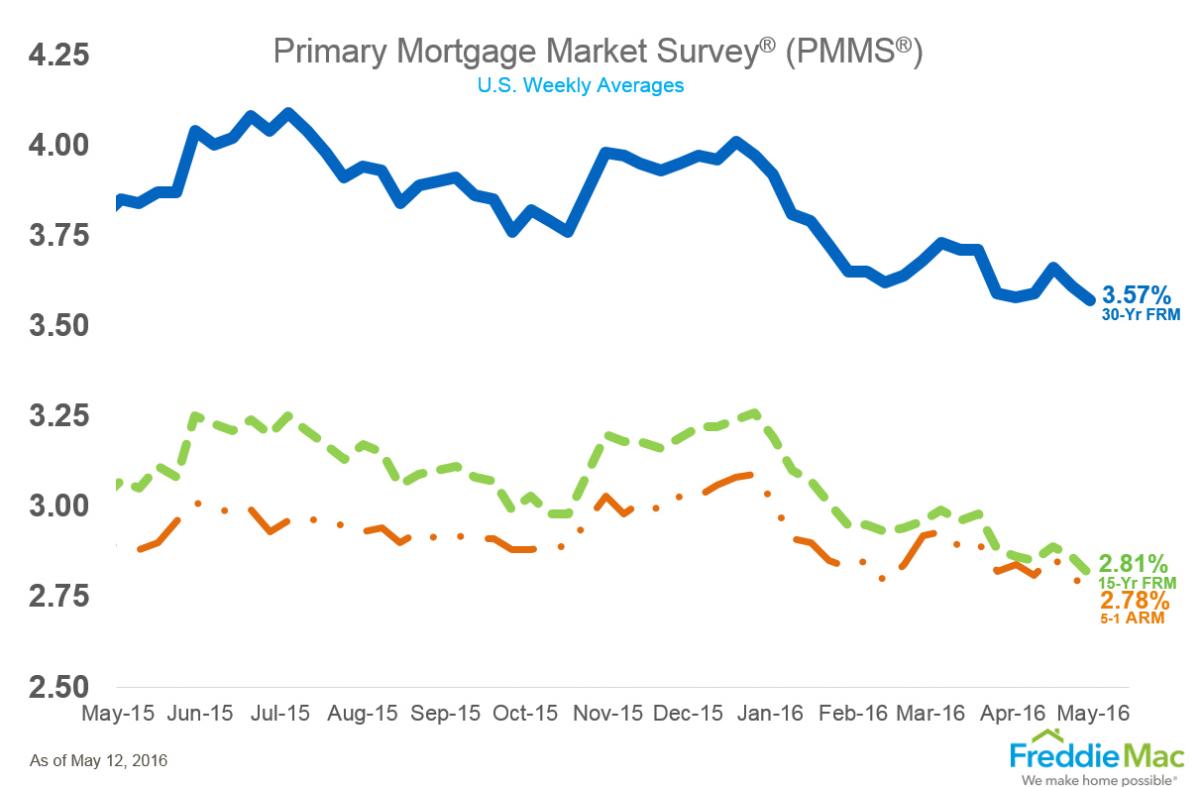

Mortgage rates sank to a new 2016 low, according to Freddie Mac’s Primary Mortgage Market Survey (PMMS) for the week ending today. The 30-year fixed-rate mortgage (FRM) hit a three-year low with an average of 3.57, down last week’s 3.61 percent. The 15-year FRM this week averaged 2.81 percent, down from last week’s 2.86 percent, and the five-year Treasury-indexed hybrid adjustable-rate mortgage averaged 2.78 percent this week, down from last week when it averaged 2.80 percent.

Still, Freddie Mac Chief Economist Sean Becketti preferred to see the rainbow instead of the rain. “Prospective homebuyers will continue to take advantage of a falling rate environment that has seen mortgage rates drop in 14 of the previous 19 weeks,” he said.

But is this happening? RealtyTrac’s latest U.S. Residential Property Loan Origination Report found 1.4 million home loans were originated on residential properties (one-to-four units) in the first quarter, down 12 percent from the previous quarter and down eight percent from a year ago. These new numbers mark the lowest level of originations since the first quarter of 2014.

According to RealtyTrac, this drop in total originations was primarily fueled by a 20 percent year-over-year decrease in refinance originations—a significant drag, to be certain, considering that purchase originations increased three percent and home equity line of credit originations increased 10 percent from a year ago.

The total dollar amount of purchase loans originated in the first quarter was an estimated $146 billion ($145,693,394,297), down 11 percent from the previous quarter but up eight percent from a year earlier. The metro areas with the biggest year-over-year percentage increase in purchase originations were Baltimore (up 26 percent); Tucson, Ariz. (up 18 percent); Louisville, Ky. (up 17 percent); Minneapolis-St. Paul (up 14 percent); and Nashville (up 14 percent).

“After a surprisingly strong 2015, the mortgage refi market started running out of steam in the first quarter of 2016 despite lower mortgage interest rates,” said Daren Blomquist, senior vice president at RealtyTrac. “Meanwhile the purchase loan market continued the pattern of slow-and-steady growth that it has been following the past two years, and HELOC originations increased on a year-over-year basis for the 16th consecutive quarter, showing that borrowers are regaining both home value and the confidence needed to increasingly leverage their home equity.”

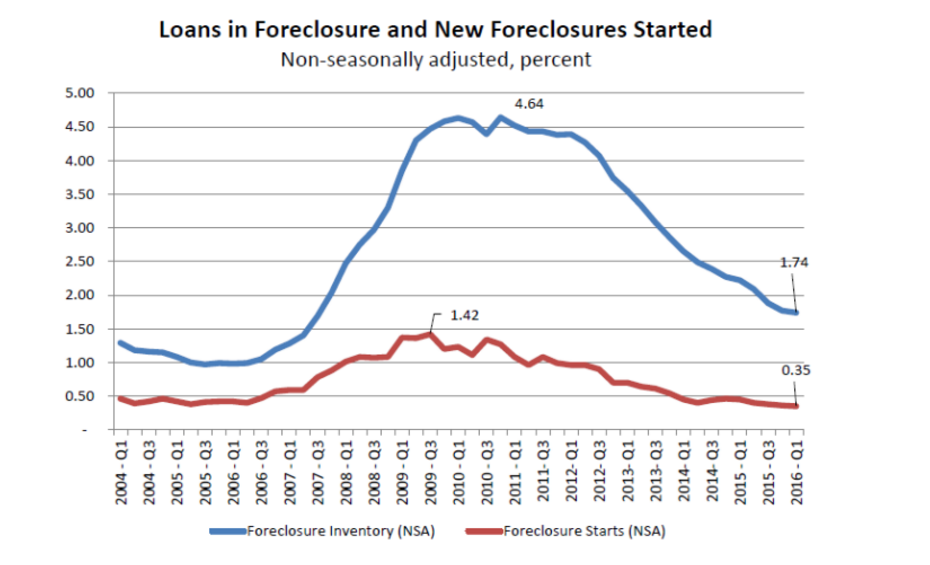

On a positive note, the home loans that are being originated are consistently strong. The data in the latest Mortgage Bankers Association’s (MBA) National Delinquency Survey determined the delinquency rate for mortgage loans on one-to-four-unit residential properties remained unchanged from the previous quarter at a seasonally adjusted rate of 4.77 percent of all loans outstanding at the end of the first quarter. This marks the lowest level since the third quarter of 2006.

The delinquency rate was 77 basis points (bps) lower than one year ago, while the percentage of loans on which foreclosure actions were started during the first quarter was 0.35 percent, a one basis point drop from the previous quarter, and down 10 bps from one year ago. This foreclosure starts rate is now at its lowest level since the second quarter of 2000. Also hitting new lows were the foreclosure inventory rate and the serious delinquency rate—both were at low levels not seen since the third quarter of 2007.

“The delinquency rate of 4.77 percent has returned to typical pre-recession levels and is lower than the historical average of 5.4 percent for the time period from 1979 to the first quarter of 2016,” said MBA’s Vice President of Industry Analysis Marina Walsh. “The rate at which new foreclosures were initiated in the first quarter was 0.35 percent, the lowest in 16 years, and 10 bps below the historical average of 0.45 percent. A total of 28 states and Washington, D.C., either saw decreases or no change in the foreclosure starts rate this quarter, while the remaining 22 states experienced increases in the foreclosure starts rate. Only two of these 22 states have strictly non-judicial processes in place.”

And a brighter near-term future is ahead for housing, according the Lawrence Yun, chief economist at the National Association of Realtors (NAR). Speaking at the trade group’s legislative conference in Washington, D.C., Yun predicted that existing sales will finish this year at a pace of around 5.40 million—the best level since the 6.48 million existing sales in 2006—while the national median existing-home price is forecast slightly moderate to between four and five percent this year.

“The housing market continues to expand at a moderate pace in spite of the fact that home prices are rising too fast in some areas because of insufficient supply fueled by the grossly inadequate number of new single-family homes being constructed,” said Yun. “The good news is that pending sales in recent months have remained stable and should support a modest gain in home sales heading into the summer.”

But, Yun warned that this can only occur if the housing inventory shortage is addressed with some degree of speed and priority.

“Homebuilders need to significantly ramp up production so that more existing homeowners can trade-up and list their home for sale,” added Yun. “Otherwise, inventory shortages will continue and demand could soften even more in some areas as a greater number of buyers are unable to find homes at affordable prices.”