The first quarter of this year brought a degree of relief to 268,000 homeowners that regained equity in their properties, according to new data from CoreLogic. By the end of the first quarter, 92 percent of all mortgaged properties had equity.

As for the eight percent of homes with negative equity (approximately four million residences), there is some good news: the total number of homes in this situation decreased 6.2 percent from the fourth quarter of 2015 and decreased 21.5 percent year-over-year. The national aggregate value of negative equity was $299.5 billion at the end of first quarter, down 3.8 percent from the previous quarter and down 11.8 from a year earlier.

Of the more than 50 million homes with a mortgage, approximately 9.1 million, or 18 percent, have less than 20 percent equity (referred to as "under-equitied") and 1.1 million, or 2.2 percent, have less than 5 percent equity (referred to as near-negative equity). Borrowers who are under-equitied may have a difficult time refinancing their existing homes or obtaining new financing to sell and buy another home due to underwriting constraints. Borrowers with near-negative equity are considered at risk of moving into negative equity if home prices fall.

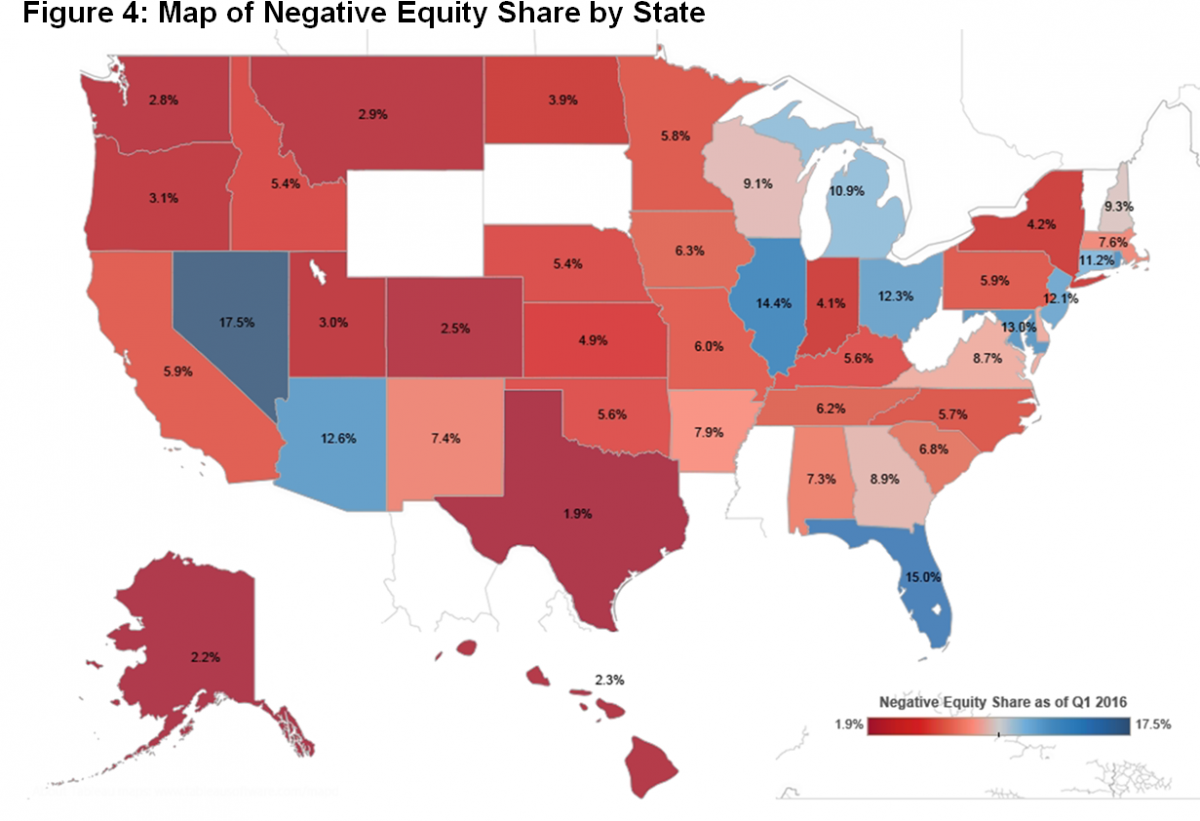

The top five states with the highest levels of negative equity—Nevada (17.5 percent), Florida (15 percent), Illinois (14.4 percent), Rhode Island (13.3 percent) and Maryland (12.9 percent)—accounted for 30.2 percent of the national negative equity level but only 16.5 percent of outstanding mortgages. Among metro markets, Las Vegas and Miami carried the highest negative equity rates with 19.9 percent and 19.6 percent, respectively. In contrast, positive equity reigned in Texas, with the highest level at 98.1 percent, and in the San Francisco metro area, with a 99.4 percent positive equity level.

"In just the last four years, equity for homeowners with a mortgage has nearly doubled to $6.9 trillion," said Frank Nothaft, chief economist for CoreLogic. "The rapid increase in home equity reflects the improvement in home prices, dwindling distressed borrowers and increased principal repayment. These are all positive factors that will provide support to both household balance sheets and the overall economy."