It is quite a busy day in the housing world: The upward spiral of home prices showed signs of stalling, Florida was identified as having the hottest housing markets, a new survey determined that Millennials are saving for downpayment and new data found foreclosure starts took an uptick.

First, let’s talk money …

The S&P CoreLogic Case-Shiller Indices (formerly known as the S&P/Case-Shiller Home Price Indices) reported a five percent annual gain in May on its U.S. National Home Price NSA Index covering all nine U.S. census divisions, the same level as the previous month. The 10-City Composite posted a 4.4 percent annual increase, down from 4.7 percent the previous month, while the 20-City Composite reported a year-over-year gain of 5.2 percent, down from April’s 5.4 percent in April.

Before seasonal adjustment, the National Index posted a month-over-month gain of 1.2 percent in May while the 10-City Composite recorded a 0.8 percent month-over-month increase and the 20-City Composite posted a 0.9 percent increase in May. After seasonal adjustment, the National Index recorded a 0.2 percent month-over-month increase, the 10-City Composite posted a 0.2 percent decrease and the 20-City Composite reported a 0.1 percent month-over-month decrease.

Despite the desultory numbers, David M. Blitzer, managing director and chairman of the Index Committee at S&P Dow Jones Indices, insisted that the data glass was half-full and not half-empty.

“Home prices continue to appreciate across the country,” Blitzer said. “Overall, housing is doing quite well. In addition to strong prices, sales of existing homes reached the highest monthly level since 2007 as construction of new homes showed continuing gains. The SCE Housing Expectations Survey published by the New York Federal Reserve Bank shows that consumers expect home prices to continue rising, though at a somewhat slower pace.”

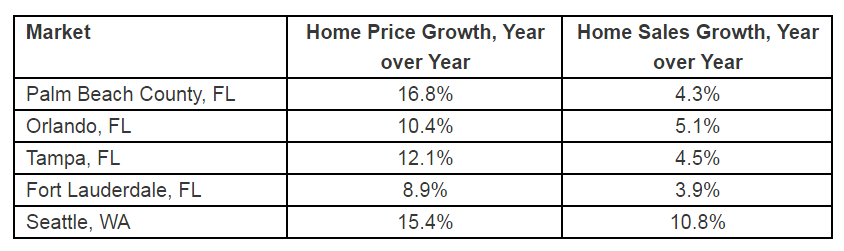

Separately, the online real estate portal Ten-X released its ranking of the nation's 50 largest housing markets according to current and forecasted housing fundamentals including pricing, sales, permit activity and economic growth. Florida reigned at the peak of the list—Palm Beach County, Orlando, Tampa and Fort Lauderdale occupied the top four spots, with Seattle coming in fifth place. San Diego, Oakland, Portland, Denver and Nashville rounded out the top 10 list.

"There are strong regional tendencies in our Summer housing market report, with cities in the Southeast, the Pacific Northwest, and California performing exceptionally well, while the Northeast and Midwest are lagging behind," said Ten-X EVP Rick Sharga. "Cities like Orlando are receiving a boost from low oil prices, which in turn is leading to an increase in travel and tourism. And of all the states that were hit hard during the crash, Florida still has the most room to grow to get back to peak housing prices."

And speaking of buying home, a new survey from TD Bank found that 63 percent of Millennials are considering a home purchase in the next two years. However, 74 percent of Millennials polled for this survey said they were saving for a downpayment, while 19 percent planned to supplement their savings for a home with financial assistance from friends and family and 65 percent planned to have a spouse or partner as a co-signer on the mortgage.

"It's encouraging to see Millennials thoughtfully prepare to enter the housing market," said Scott Haymore, head of pricing and secondary markets at TD Bank. "With today's affordability programs, owning a home doesn't have to be a dream, it can be a reality."

Hopefully, tomorrow’s homeowners will stay in their homes and not face foreclosure. New data from Black Knight Financial Services placed the total U.S. loan delinquency rate (loans 30 or more days past due, but not in foreclosure) at 4.31 percent in June, up 1.33 percent from May but down 10.03 percent from June 2015. The total U.S. foreclosure pre-sale inventory rate registered at 1.10 percent in June, down 2.57 percent in May and down 29.35 percent from one year earlier.

However, there were 69,300 foreclosure starts in June, up 11.59 percent from May but down 11.27 percent from a year earlier. June marked the second consecutive month with rising foreclosure starts.