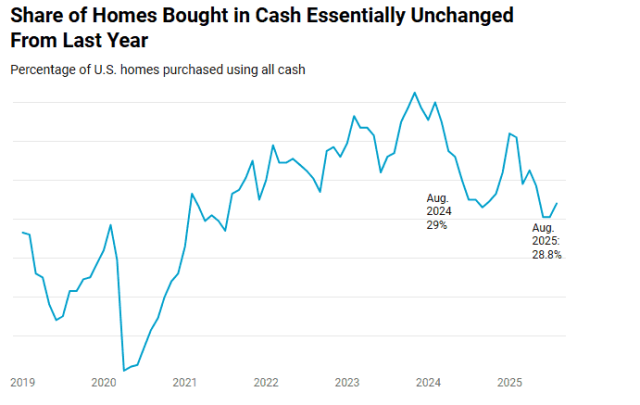

Redfin recently examined nationwide home sales and found that 28.8% of U.S. homebuyers paid in all-cash in August, down just incrementally from 29% year-over-year. The prevalence of all-cash payments peaked at nearly 35% in late 2023 and early 2024 because mortgage rates peaked in the high-7% range during that time. Buyers were inclined to pay in cash — if they could afford it — to avoid high monthly interest payments.

When mortgage rates fell from that peak, all-cash payments became less common, as lower rates meant lower interest payments. Another reason the share of buyers paying in cash has declined from its peak: this past summer was the strongest buyer’s market in over a decade, and a less competitive market means fewer buyers have to pay cash to beat out other bidders.

While the share of buyers paying cash has declined from its high point, it is essentially unchanged from last year largely because mortgage rates were sitting between 6.5% and 6.6% in August, mostly flat from a year before, keeping interest payments the same.

The lack of all-cash buyers can be good news for house hunters who do not have the means to purchase a home without a loan, especially when paired with the fact that buyers in most markets hold negotiating power. Now that rates have declined a bit more to a weekly average of 6.27%, all-cash purchases may become even less common.

“First-time buyers have more opportunities than they did when the market was hot; they’re no longer competing against 10 other offers from people who are either paying in cash or shelling out a 50% downpayment,” said Kathy Scott, a Redfin Premier agent in Phoenix. “House hunters are able to take a breath and think more clearly about where they want to live and what type of house they want. When they find it, they can make an offer they feel comfortable with, even if it’s below the asking price, and there’s a real chance the seller will accept. Home prices may dip a bit in the next year or so, but now is a great time to start building equity if you’re planning to stay in your new home for five to 10 years.”

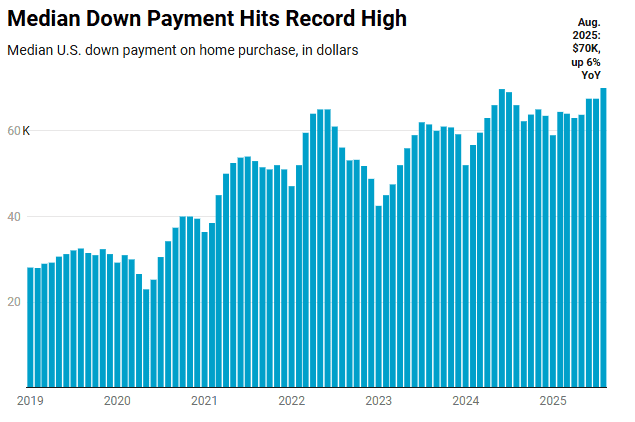

Median Downpayments On The Rise

A typical downpayment for a home was $70,000 in August 2025, up 6.1% year-over-year to the highest dollar amount ever. In percentage terms, the typical homebuyer’s downpayment was equal to 18.6% of the purchase price, up from 17.8% a year earlier, and the highest August level reported since 2013.

As the price of homes continues to rise, downpayments are following suit, as when homes cost more, buyers need to put down more money.

But higher prices aren’t the only reason … home prices have risen nearly 2% year-over-year and downpayments are up 6%. Downpayment growth is outpacing home price growth mainly because when housing costs are high, like they are now, affluent people with the means to make larger downpayments are more likely to buy homes. It’s also likely that some wealthy Americans are making larger downpayments, rather than paying in all-cash as mortgage rates slide closer to the 6% mark.

“With the housing market in a downturn, the people who are buying are those who are financially comfortable, secure in their jobs, and have money ready and waiting in the bank for a downpayment,” said Andrew Vallejo, a Redfin Premier agent in Austin, TX. “For example, a few months ago, I helped a buyer close on an $800,000 home with a 50% downpayment. They were able to liquidate stocks to make a $400,000 downpayment without thinking about it too much, and now their monthly payments are lower.”

Metro-Level Highlights

Reports from the month of August 2025, covering 40 of the most populous U.S. metro areas, include:

- All-cash purchases were most prevalent in West Palm Beach, Florida, where 43.4% of all home purchases were in cash, followed by Cleveland (42.1%) and Miami (39.2%).

- All-cash purchases were least prevalent in several West Coast metros, including Oakland, California (18.8%); San Jose, California (19.1%); and Seattle (20.5%).

- The share of homes purchased in cash rose in roughly half the metros in Redfin’s analysis, with the biggest increases found in Baltimore; Riverside, California; and Providence, Rhode Island.

- The share of homes purchased in cash declined most in Milwaukee, New York, and Cincinnati.

- Downpayments were reported the biggest in California, with the median downpayment at $408,000 in San Jose, the most of any metro in this analysis, $400,000 in San Francisco, and $300,000 in Anaheim. Downpayments were the smallest in Virginia Beach, Virginia ($9,000); Pittsburgh ($23,000); and Cleveland ($27,000).

- Downpayments rose year-over-year in roughly half the metros in Redfin’s analysis, with the biggest increases reported in Providence, Rhode Island; Chicago; and Washington, D.C. The biggest declines were found in Riverside, California; Seattle; and Denver (-9.5%).

- In percentage terms, California also takes the cake in terms of biggest downpayments, as the typical homebuyer put 25% down in Anaheim, San Francisco, and San Jose. Percentages were smallest in Virginia Beach (3%), Las Vegas (9.4%), and Tampa, Florida (9.8%).

- In percentage terms, downpayments rose in 28 of the metros in Redfin’s analysis, with the biggest increases reported in Providence, Rhode Island; Orlando, Florida; and Columbus, Ohio, with the biggest declines found in Miami, Denver, and Warren, Michigan.