From left to right, E Mortgage Capital CEO Joseph Shalaby, West Capital Lending CEO Daniel Iskander, NEXA CEO Mike Kortas, Loan Factory CEO Thuan Nguyen, Equity Smart Home Loans CEO Pablo Martinez, and NMP Head of Engagement & Outreach Andrew Berman.

There’s only one mortgage conference in the nation that would invite the top five brokerage owners in the nation on stage to battle head-to-head over who has the best brokerage model, and that’s Originator Connect.

In classic MMA fashion, the heavyweight broker champions emerged from each corner of the room with hype music blaring over the loudspeakers, inspiring rambunctious cheers and even some boo’s from originators in the audience. Of course, gathering five of the top CEOs of the broker world on stage would encourage excitement in the crowd, as did many of the provocative questions from host Christine Stuart, News Director at National Mortgage Professional. But the Brokerage Brawl event wasn’t merely for entertainment.

From left to right, E Mortgage CEO Joseph Shalaby, West Capital Lending CEO Daniel Iskander, NEXA CEO Mike Kortas facing off against Equity Smart CEO Pablo Martinez, and NMP Head of Engagement & Outreach Andrew Berman to the far right.

The Contenders:

Pablo “The Determinator” Martinez, Equity Smart Home Loans CEO

“Tenacious” Thuan Nguyen, Loan Factory CEO

“Electric” Joe Shalaby, E Mortgage Capital CEO

“Dynamic” Dan Iskander, West Capital Lending CEO

Mike “The Bull” Kortas, NEXA CEO

In 2023, the broker community is showing who’s boss. Statistics from the NMLS shows retail originators switching to wholesale at an increasing rate, and in 2022 over 20,000 loan officers joined the wholesale channel. More can be expected to transition this year because brokers can offer borrowers more competitive rates and lower fees on their loans. With high rates, unreachable home prices, and scarce inventory, the mortgage business is as dry as a bone. In these desperate times, originators from retail and banking are looking for salvation in the wholesale channel, and broker owners are ready to capture them with a wide net.

The transition from retail originator to broker can be shaky if one does not know what they’re looking for. The decision to work with one brokerage over another is largely up to individual preference. Does the originator want the freedom to choose their own software? Does the originator need training to become self-generated? Are they looking for access to specific resources or tools? And, of course, do they want to work with Rocket or UWM?

Get the NMP Daily

Essential stories, every weekday.

Really, it comes down to what kind of leadership style the originator is attracted to, and here we have a very different assortment.

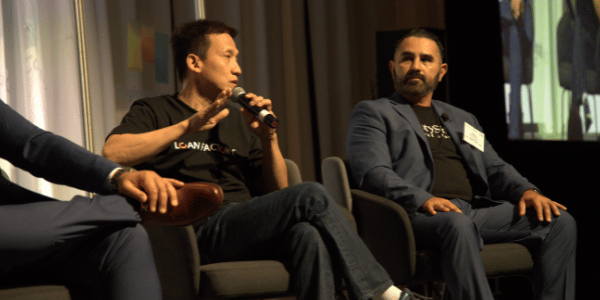

West Capital Lending CEO Iskander speaking on stage, with Loan Factory CEO Nguyen looking over his shoulder. On the right, E Mortgage Capital CEO Shalaby holds the microphone.

Training & Retention

Working in the brokerage channel means loan originators need to be proficient at generating their own leads. That could present challenges for some retail originators who have been working in call centers and had their leads handed to them. So each brokerage’s training and recruitment process matters greatly, as well as their retention. Some companies are willing to nurture originators with support and training, while others expect them to hit the ground running.

Looking at overall monthly volume numbers can be deceiving, since 10% of originators could be carrying out most of the production while many others are floundering. It’s one thing to be able to recruit top producers in the industry, but quite another to be able to create top producers. Iskander, CEO of West Capital Lending, claims his company does it best.

“We’re funding 550 units compared to, I think, last month they [NEXA] funded 1,560. So we’re funding one third of their production, yet we have only 16% of the LOs that they do,” Iskander said.

Some brokerages, such as West Capital Lending and Loan Factory, are more in favor of a nurturing approach when it comes to training their loan originators. They care about retention, because after providing training and doing the hard work to get those new recruits acclimated, it could be a blunder when most of them end up leaving.

Nguyen’s latest comeback story helps illustrate the challenges in recruiting, training and retaining loan originators. Seven months ago, Loan Factory had only 20 LOs on staff producing 50 loans per month. Since then it has aggressively been able to recruit 300 more new and experienced LOs. But that’s come at a cost to overall productivity: for the company, production has risen to 167 loans per month. But on average, individual production has dipped from 2.5 loans per month to one funded loan every other month per loan officer.

Nguyen recognizes the slippage, but argues that problem can be solved with enough time and training. “Recruiting is important but retention is even more important. It’s difficult to provide them with support and training to help them grow their production. We focus our attention on the support they need; the marketing, the underwriting, the technology, the training, and the coaching,” Nguyen asserts. “So give us a few months and we’re going to be way better.”

On Your Own

NEXA, on the other hand, has more of a sink or swim mentality. Its onboarding process is expedient, putting loan originators on the payroll in as little as four hours, its training process is an ongoing weekly class. Kortas said NEXA has an academy program for newer originators, but they must honor a commitment to fund at least two loans a month.

“You have to commit to doing at least 2 loans a month... but if you don’t do that, we’ll let you go,” Kortas said. “Out of 400 new loan officers who join the academy, probably 300 of them wash out. But that’s the reality of this industry.”

That eventually prompted Nguyen to slam Kortas in an interview after the Brawl, saying, “I don’t think he really cares for the loan officers… The loan officer that joins NEXA has to pay a lot. They take a lot of money out of their commissions to pay the recruiter... at the same time he charges other fees: software fees, academy fees, and all that.”

Nguyen even said that he receives calls from NEXA loan originators who complain that their company is taking too big a cut out of their paychecks. At Loan Factory, Nguyen said LOs don’t have to pay for anything, including software.

The ultimate flaw with NEXA’s model, according to Nguyen, is that it centers around recruitment. Bring a ton of fish in and only hold on to the big ones. That may mean constant staff turnover, but the end result for NEXA is clear: the company came in with the highest dollar volume overall for the past 12 months, $4.5 billion, according to Modex.

Tools & Software

In order for brokers to fund loans efficiently and fund more loans per month, they need to have access to the right tools and technology. Of course, that may vary between loan originators so many may have the desire to choose their own systems.

Although most of the broker owners on stage accept employees’ suggestions when it comes to the technology and tools they use, Nguyen believes his proprietary technology is the best, leaving no room for suggestions.

“They don’t have a choice,” Nguyen said.

The audience burst into laughter at his frankness, but Nguyen justified his stance by saying loan originators have no business making technology decisions. They must only concern themselves with the front end of the process.

Not everyone in the crowd reacted negatively to the statement, since Loan Factory’s software and technology is impressive. Nguyen claims Loan Factory is the only mortgage company that provides a free system for loan originator assistants (LOAs). That has become especially useful as originators have had to turn to more complex offerings – such as Non-QM and reverse mortgages – and LOAs are the support team that lets the originator move on to more production. Having free access to tech makes the whole process easier for everyone, Nguyen argues.

On top of that, Loan Factory also has proprietary tech that provides its originators with online application generation, rate alerts, a borrower portal, CRM and Cloud-based document management.

As previously mentioned, Nguyen boasted that his originators don’t have to pay any fees for software, marketing, assistants, training, underwriter support, or a desk at the office. However, the Loan Factory website does note that brokers have a $595 flat fee off their commission every month and have a $500 processing fee per loan.

“Why would you waste time trying other software?” Nguyen asked the audience. “It’s all free at Loan Factory.”

Loan Factory CEO Thuan Nguyen speaking on stage at the Brokerage Brawl. To his left is West Capital Lending CEO Daniel Iskander and to his right is Smart Equity Home Loans CEO Pablo Martinez.

Iskander disagreed, saying not providing originators a say in the technology they use is a bad decision.

“We encourage them to go out there and find their own technology… as long as it’s compliant,” Iskander said. “LOs are the ones out there exploring new technologies, testing them, so I think it’s important for them to have a choice. Thuan’s software might not suit a certain LO’s desire for how he wants to approach his business.”

Kortas likewise shot back at Nguyen for his response, saying that it’s “insane” to not allow originators to have a say in what technology they use. At NEXA, Kortas said originators get to voice their opinions every Tuesday in a company-wide video conference, where suggestions and criticisms are welcome.

Bringing on more than a thousand loan originators to Zoom their suggestions and criticisms seems like its own kind of brawl, but Kortas said that it is an organized meeting with a Q&A session at the end.

In a followup interview, Kortas was a bit more complimentary of Nguyen, but believes he did lose the Brokerage Brawl because of the software question.

“Contrary to popular belief, people think I don’t respect Thuan, but I do,” Kortas said. “I thought his opening music ‘don’t call it a comeback’ was appropriate. But I do think he came in last place… you don’t get to tell loan officers software is more important than you and think loan officers don’t care about that.”

Joseph Shalaby, E Mortgage Capital CEO, said his company endorses several pieces of technology. But it stays firm against allowing loan officers to have complete control over which technology they use, over concerns about borrower data protection.

“We encourage loan officers to keep their ear to the ground and find new solutions because technology is changing so quickly,” Shalaby said. “We want to be at the forefront of any innovation that can help take our business to the next level.”

Likewise, Martinez encourages collaboration and suggestions when it comes to the technology and tools they provide.

The structured-finance data provider’s first employee succeeds Rahbar following more than a decade with the company

Jonathan Warrick has been named head of dv01, succeeding founder Perry Rahbar in the top leadership role at the structured-finance data and analytics provider.Warrick, dv01’s first employee, most recently served as chief operating officer. Rahbar is transitioning to a strate...

Fitch downgraded the wholesale giant after leverage reached 6.1x, saying the preferred investment changes UWM’s funding structure but does not immediately reduce its debt burden

United Wholesale Mortgage’s $2.05 billion capital reset may strengthen its liquidity and replace secured borrowings, but Fitch Ratings does not believe the transaction immediately reduces the wholesale lender’s debt burden.Fitch downgraded the long-term issuer default rating...

New Fannie Mae-, Freddie Mac- and Ginnie Mae-approved mortgage servicer aims to keep originators connected to borrowers through servicing data, payoff visibility and retention tools