It’s been a slow burn since the Federal Reserve changed direction and, in mid-September, responded to economic uncertainty and a sagging jobs market by lowering the target range for the federal funds rate by 0.25 percentage points to 4% to 4.25%. This move by the Federal Open Market Committee (FOMC) marked the first time in 2025 that the Fed has cut rates, ending a streak of five consecutive meetings where the federal funds rate was held steady at 4.25%–4.50%.

And with this move, homebuyers have begun to reap the benefits of a sliding mortgage rate market, slowly emerging from the sidelines and benefiting from the Fed’s rate cuts.

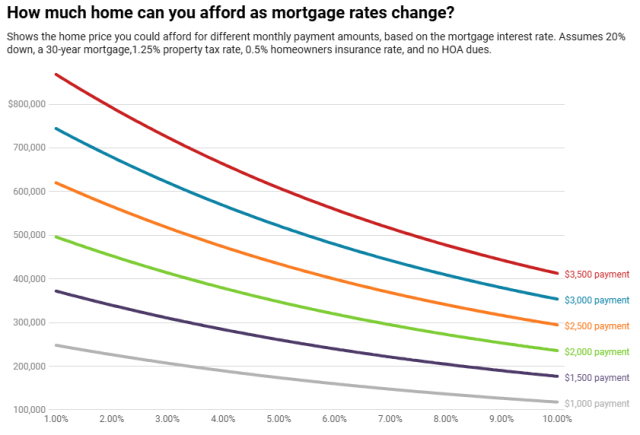

For prospective buyers, those on a $3,000 budget have gained $26,000 since last year as mortgage rates fall, but pending home sales are still slipping. Lower mortgage rates are curbing growth in monthly housing payments, as the typical U.S. monthly payment is $2,556, up 0.6% year-over-year, the smallest increase in three months, according to a new report from Redfin.

Freddie Mac reports the 30-year, fixed-rate mortgage (FRM) at 6.19% as of October 23, 2025, down from the previous week when it averaged 6.27%. A year ago at this time, the 30-year FRM averaged 6.54%.

With rates in their current range, a homebuyer on a $3,000 budget can afford a $473,750 home at today’s mortgage rate, compared to the $447,750 home they could have bought one year ago, when rates were around 6.85%. Compared to one month ago, buyers have gained $9,500 in purchasing power; they could have bought a $464,250 home with rates sitting near 6.4%.

“Mortgage rates continued to trend down this week, hitting their lowest level in over a year,” said Sam Khater, Freddie Mac’s Chief Economist. “At the start of 2025, the 30-year, fixed-rate mortgage surpassed 7%, while today it hovers nearly a full percentage point lower. This dynamic has kept refinancings high, accounting for more than half of all mortgage activity for the sixth consecutive week.”

Despite More Purchasing Power, More Remain In The Shadows

Pending U.S. home sales fell 0.7% year-over-year during the four weeks ending October 19, marking the third consecutive week of declines.

Buyers are citing a few reasons they remain on the sidelines. First, many cite the forces pushing mortgage rates down — economic uncertainty and political tensions — are also making some house hunters feel uneasy about making a major purchase. Buyers are also facing stubbornly high prices, with the median home-sale price up 2% year-over-year, the biggest increase in six months.

The selling side is holding up better. Redfin reports that new listings rose 4.6%, the biggest increase in nearly five months, as sellers hope buyers pounce on lower rates. Nationwide, there are half a million more home sellers than buyers.

“Buyers are scoring deals, especially those who can pay all cash and/or those who are open to new construction,” said Amanda Peterson, a Redfin Premier agent in Dallas. “One recent all-cash buyer paid $500,000 for a condo that was appraised at $685,000 — and the seller agreed to pay upfront for six months of pricey HOA dues. And builders are offering steep discounts on new homes, especially in areas where they already have a lot of inventory and are still actively building. Builders are dropping prices, giving up to $20,000 in concessions, throwing in appliances, and buying down mortgage rates, sometimes to below 4%.”