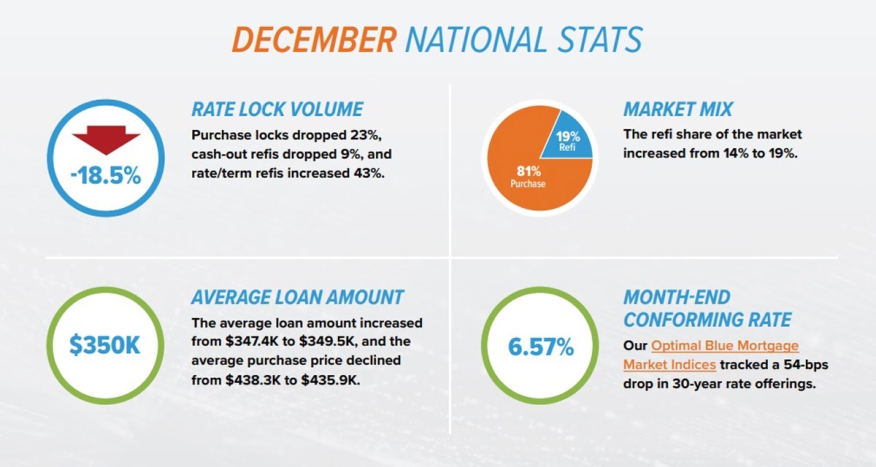

In December, purchase rate lock volume dropped 23%, cash-out refis dropped 9% and rate/term refis increased 43%, according to the Optimal Blue Originations Market Monitor report.

“Mortgage rates continued to fall in December, with the Fed delivering welcomed commentary suggesting rates may have peaked with cuts on the horizon in 2024,” said Brennan O’Connell, data solutions manager, Optimal Blue. “The sharp drop in rates provided tailwinds that caused rate/term refinance volume to rise a notable 43% month over month. Despite cash-out volume declining 9%, the total refinance share of locks rose to 19% in December – the highest level since April 2022. However, the improving rate environment had little impact on purchase lending, where lock volume fell 23% in December, traditionally the slowest month for homebuyer activity.”

The growth in the rate/term volume was driven by VA volume.

VA loans saw the highest volume in December, rising 137 bps to finish the month at 11.8% of total volume.

FHA refinance volume also ticked up in December, despite FHA total volume dropping 105 bps of market share to 21.5% of total volume. The GSE-eligible share rose 36 bps to 56.6% and nonconforming volume – inclusive of jumbo and non-QM – dropped 72 bps to 9.4%. The adjustable-rate mortgage (ARM) share of locks continued to fall, dropping to 5.2% of total volume.

The 30-year conforming rate dropped 54 bps to finish the month at 6.57% and jumbo, FHA, and VA loans fell 74 bps, 49 bps, and 67 bps, respectively.

“The spread between the 30-year conforming rate and the 10-year Treasury yield remained essentially flat in December as government bonds and mortgages benefitted equally from the positive fixed-income outlook,” O’Connell said. “Looking ahead to 2024, the mortgage-to-Treasury spread remains elevated from historic norms at roughly 275 bps, suggesting there may be further room for compression and reduction in mortgage rates.”

The rise in rate/term refinance volume coincided with a drop of eight points in the average credit score as borrowers with lower credit scores jumped on the opportunity to lower their monthly payments with VA and FHA refinances. Purchase and cash-out refinance credit scores ticked higher, however. The average loan amount rose to $349,500 from $347,400, while the average purchase price saw another – albeit smaller – decline, falling from $438,300 to $435,900.