Where a borrower lives may be one of the biggest factors determining whether they can achieve homeownership as a single parent.

A new LendingTree analysis found that single parents in some U.S. metropolitan areas are more than twice as likely to own a home as those in the nation's most challenging housing markets, underscoring the role local affordability plays in shaping homeownership outcomes.

Nationally, 39.2% of single parents are homeowners, compared with 73.7% of two-parent households and 65.2% of Americans overall. Single-parent homeowners spend 25.7% of their income on housing costs, while single-parent renters devote 40.9% of their income to housing, well above the commonly cited 30% affordability threshold.

For mortgage professionals, the findings offer another illustration of how local housing economics can influence borrower opportunity. While affordability remains a nationwide challenge, the study suggests some markets continue to offer a realistic path to ownership for single-income households.

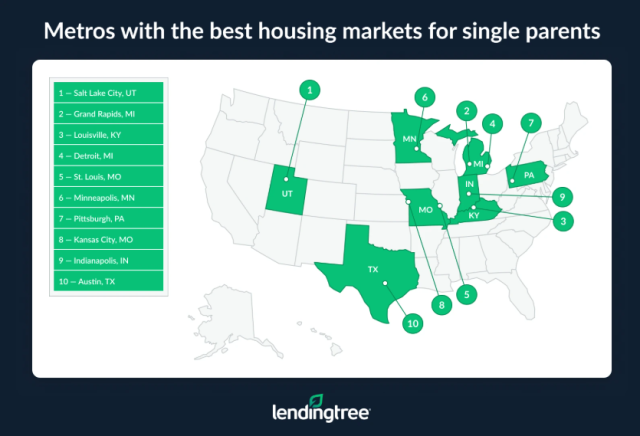

LendingTree ranked the nation's 50 largest metropolitan areas using a housing index that combines single-parent homeownership rates with affordability measures for both owners and renters.

Salt Lake City ranked as the best housing market for single parents, followed by Grand Rapids, Mich.; Louisville, Ky.; Detroit; St. Louis; Minneapolis; Pittsburgh; Kansas City; Indianapolis; and Austin.

"The metros that tend to work best for single parents usually strike a balance between decent wages and relatively affordable housing," said Matt Schulz, LendingTree's chief consumer finance analyst. "Places like Salt Lake City, Grand Rapids, and Louisville generally offer lower housing costs than the biggest coastal areas while still providing economic opportunity and communities where families can realistically put down roots."

At the opposite end of the rankings were Los Angeles, New York, and San Diego, where housing costs have significantly outpaced incomes.

"Even solid earners can struggle there, and for single parents relying on one income, the math often just doesn't work," Schulz said.

Salt Lake City also posted the highest single-parent homeownership rate among the nation's largest metros at 52.2%, followed by Minneapolis at 48.4% and Grand Rapids at 48.1%.

By comparison, Los Angeles recorded the lowest single-parent homeownership rate at 24.3%, followed by New York at 27.2% and Memphis, Tenn., at 28.1%.

That means a single parent in Salt Lake City is more than twice as likely to own a home as a single parent in Los Angeles.

"A lot of this comes down to affordability," Schulz said. "In places where starter homes still exist and where families can buy in decent neighborhoods without stretching every dollar, homeownership rates are naturally going to be higher."

The affordability differences extend beyond whether households own or rent.

Single-parent homeowners in Indianapolis spend the smallest share of their income on housing costs at 21.7%, followed by Louisville at 22.0% and Raleigh, N.C., at 22.5%.

Meanwhile, single-parent homeowners in Los Angeles spend 31.8% of their income on housing, compared with 31.6% in New York and 30.4% in both San Diego and Miami.

"In places like Indianapolis, Louisville, and Raleigh, housing simply consumes a smaller share of income, which gives families more breathing room," Schulz said. "When you're not pouring every spare dollar into housing costs, you're better able to save for emergencies as well as for your long-term goals."

The study also found that renters face even steeper challenges. Single-parent renters nationwide spend an average of 40.9% of their income on housing. Among the nation's largest metros, Kansas City, Louisville, and Nashville had the lowest rental cost burdens for single parents, while Miami, Orlando, and Riverside, Calif., ranked among the highest.

The findings arrive as lenders continue searching for purchase-market growth in an environment defined by affordability constraints. While elevated home prices and mortgage rates remain obstacles across much of the country, the report suggests geography continues to play a major role in determining where single-income households can successfully transition from renting to owning.

The analysis was based on data from the U.S. Census Bureau's 2024 American Community Survey and examined housing costs, affordability, and homeownership rates among single-parent households across the nation's 50 largest metropolitan areas.