Fitch Ratings says it assumes a higher rate of loss for non-qualified mortgage (Non-QM) loans, even though borrowers and lenders face more strict lending rules as a result of the 2008 financial crisis.

In a report released Feb. 27, Fitch said rising mortgage rates and high home prices are reducing home affordability, prompting originators to increase production of more affordable Non-QM mortgages, or “affordability products.”

Affordability products allow a borrower to qualify for a loan and make the monthly payments through longer terms to maturity or other features, satisfying the Consumer Financial Protection Bureau's Ability to Repay (ATR) Rule.

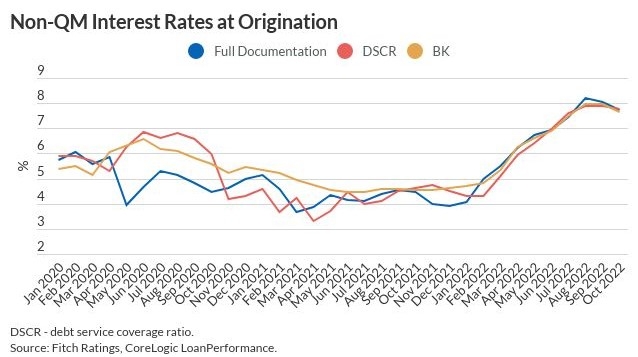

Fitch said it does not expect ratings to be affected as a result of the growth of Non-QM mortgage products, given robust credit enhancement for Fitch-rated residential mortgage-backed securities (RMBS) transactions. Non-QM, 30-year, fixed-rate loan rates typically are a percent or two higher than the prime 30-year fixed mortgage rate, which increased from the mid-3% range to over 7% in 2022, and now hovers around 6.5%-7%.

Freddie Mac said Thursday that the 30-year fixed mortgage rate increased again in the past week, and now sits at 6.65%.

“Although the majority of loans in Non-QM RMBS transactions are 30-year fixed-rate loans, an increasing volume of mortgages have affordability product features — such as over 40-year terms to maturity, interest-only periods, adjustable rates, and balloon payments,” Fitch said in its report. “These products offer borrowers lower monthly mortgage payments in the near term, with borrowers looking to refinance in the future when rates drop.”

Fitch said it does not believe the resurgence of affordability products akin to those seen in the run up to the 2008 financial crisis “will result in a similar extensive deterioration in performance, as a number of safeguards are now in place to prevent a repeat of the implosion of the private label U.S. RMBS market.”

It added that lenders are now subject to more stringent lending and disclosure laws, including the ATR Rule and the TILA-RESPA Integrated Disclosure (TRID) rules.

“Issuers have skin in the game under risk-retention requirements that encourage the alignment of issuer and RMBS noteholder interests,” Fitch said. “Furthermore, third-party review (TPR) firms conduct credit, compliance, valuation, and data integrity reviews on the loans in new U.S. RMBS transactions to ensure they are being underwritten to the originator’s guidelines, citing any exceptions that they find.”

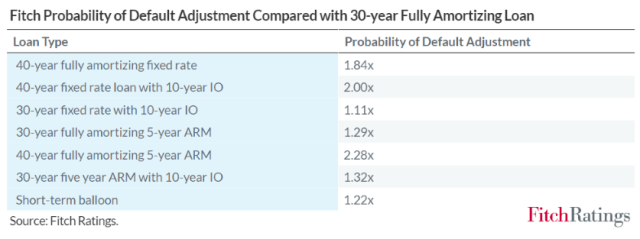

Fitch conducts operational reviews of originators and aggregators to assess how loan processes and procedures affect the origination quality of the loans. “We also increase the probability of default (PD) for affordability products compared with a 30-year fully amortizing loan to model higher stressed losses for these loan types,” it said. (See chart below.)

The loan losses Fitch assumes for affordability products are significantly higher than they were before the financial crisis, it said, reflecting a number of analytical lessons learned. Its loss models incorporate loan-level data from loans originated in the runup to the financial crisis, so ratings reflect severe losses from that period, accounting for the risk of affordability product collateral, it said. In addition, Fitch adjusts modeled losses based on the results of the TPR review.

Although the overall credit box for Non-QM has tightened in the first quarter of 2023 from the first quarter of 2020 — with weighted-average (WA) FICO scores increasing 20 points to 741 and debt-to-income (DTI) levels decreasing 2% to 34% — credit quality on a weighted average basis has seen a decline in the past year as affordability has decreased, Fitch said.

The ratings firm said that, over the past year, it reviewed the collateral attributes from eight Fitch-rated Non-QM issuers — Imperial Funding Mortgage Trust (IMPRL); Angel Oak Mortgage Trust (AOMT); Ellington Financial Mortgage Trust (EFMT); Starwood Mortgage Residential Trust (STAR); Bravo Residential Funding Trust (BRAVO); New Residential Mortgage Loan Trust (NRMLT); COLT Mortgage Loan Trust (COLT); and OBX Non-QM Trust (OBX) — and found that, along with the higher volume of affordability products, WA FICOs have declined and WA combined loan-to-value ratios (CLTVs) increased in Non-QM RMBS transactions, reflecting a shift from refinancing to purchase activity and resulting in an increase in average expected losses.

The concentration of DSCR loans — a loan product underwritten to the cash flow from rent payments rather than the borrower’s ability to repay — has also increased in issuer pools since January 2022, Fitch said. The spike in interest rates has driven many potential homebuyers to continue renting, leading to a booming rental market. Fitch said it has seen originators targeting DSCR product borrowers at a higher rate to drive business.