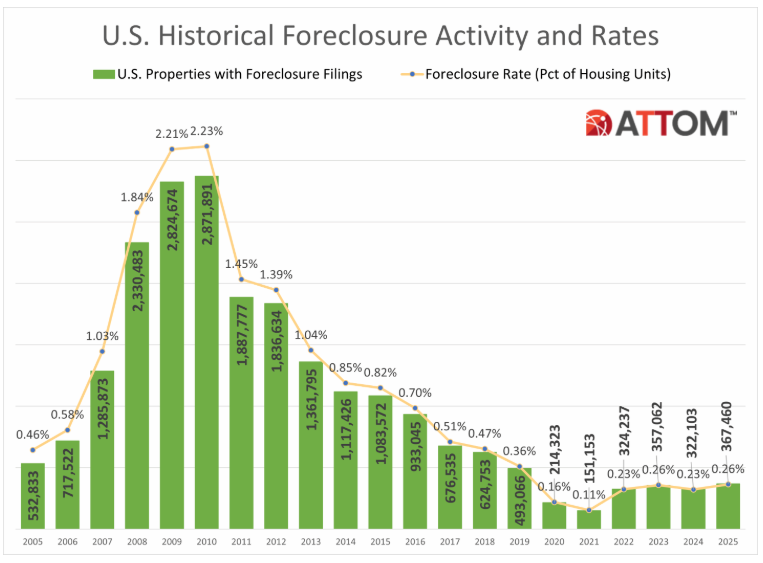

Foreclosure activity rose notably in 2025, according to the ATTOM Year-End 2025 Foreclosure Market Report, reflecting a broader trend toward normalization in the housing market after several years of historically low foreclosure levels. The data reveal increases in foreclosure filings, starts, and bank repossessions compared with 2024, although overall activity remains significantly below pre-pandemic levels and far below peaks seen during the 2008–2010 housing crisis.

In total, 367,460 properties across the U.S. reported one or more foreclosure filings in 2025 一 a 14% rise from 2024, and a 3% increase from 2023 一 yet remains about 25% below 2019 levels before pandemic disruptions reshaped housing market dynamics. From a long-term perspective, filings are 87% lower than the height of the foreclosure surge in 2010, when nearly 2.9 million properties were in distress.

Foreclosure filings accounted for approximately 0.26% of all U.S. housing units in 2025, slightly higher than the 0.23% recorded in 2024 but still below historical norms from earlier in the decade. “While filings, starts, and repossessions all rose compared to 2024, foreclosure activity remains well below pre-pandemic norms and a fraction of what we saw during the last housing crisis,” said Rob Barber, CEO at ATTOM. “The data suggests that today’s uptick is being driven more by market recalibration than widespread homeowner distress, with strong equity positions and more disciplined lending continuing to limit risk.”

Foreclosure Starts And Repossessions Rise

Lenders initiated the foreclosure process on 289,441 properties in 2025, a 14% increase from the prior year and a dramatic rebound from the pandemic-era low in 2021 — although these figures remain below pre-pandemic volumes. Texas, Florida, California, Illinois, and New York reported the largest numbers of foreclosure starts, with major metropolitan areas such as New York City, Chicago, and Houston among the most affected.

Bank repossessions, real estate-owned (REO) filings, increased 27% year-over-year, with 46,439 properties repossessed through foreclosure. Texas led in REO activity, followed by California and Pennsylvania. Even with this increase, completed foreclosures are still well below levels seen before the pandemic, underscoring the broader context of modest distress relative to historical norms.

Geographic Variations And Metro Distress Patterns

Foreclosure rates varied significantly by state and metropolitan area in 2025. Florida, Delaware, and South Carolina reported the highest rates of foreclosure filings, with one in every approximately 230–242 housing units affected. Additional states with elevated rates included Illinois, Nevada, New Jersey, and Ohio. Metro areas with the worst foreclosure rates included:

- Lakeland, Florida

- Columbia, South Carolina

- Cleveland, Ohio

- Cape Coral, Florida

- Atlantic City, New Jersey

Among larger metro regions, Jacksonville, Florida; Las Vegas, Nevada; Chicago, Illinois; and Orlando, Florida were particularly notable for higher foreclosure activity.

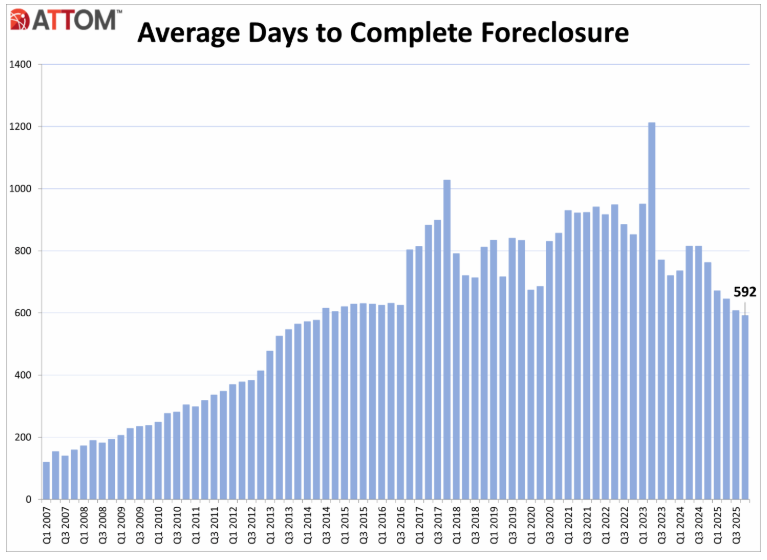

Timeline Of Foreclosure Proceedings Shortens

The average time a property spent in the foreclosure process declined in late 2025, with properties foreclosed in Q4 spending about 592 days in distress — down 3% from the previous quarter and 22% from a year earlier. States with the longest foreclosure durations included Louisiana, New York, Hawaii, Connecticut, and Kansas, with timelines ranging from roughly 1,600 to more than 3,400 days.

Quarterly And Monthly Trends

The year’s Q4 continued the broader trend, with 111,692 properties reporting foreclosure filings — up 10% from the previous quarter, and 32% year-over-year. December 2025 also saw an uptick, with 44,990 properties reporting filings, a 26% increase from November, and 57% above December 2024 figures.

"We project a sharp rise in FHA foreclosure referrals during the second and third quarters of this year, as new FHA loss mitigation restrictions end the perpetual workout cycle and push more mortgages into foreclosure," added Donna Schmidt, president and CEO of DLS Servicing. "At least five years’ worth of inventory will need to move through the system within a condensed time frame."