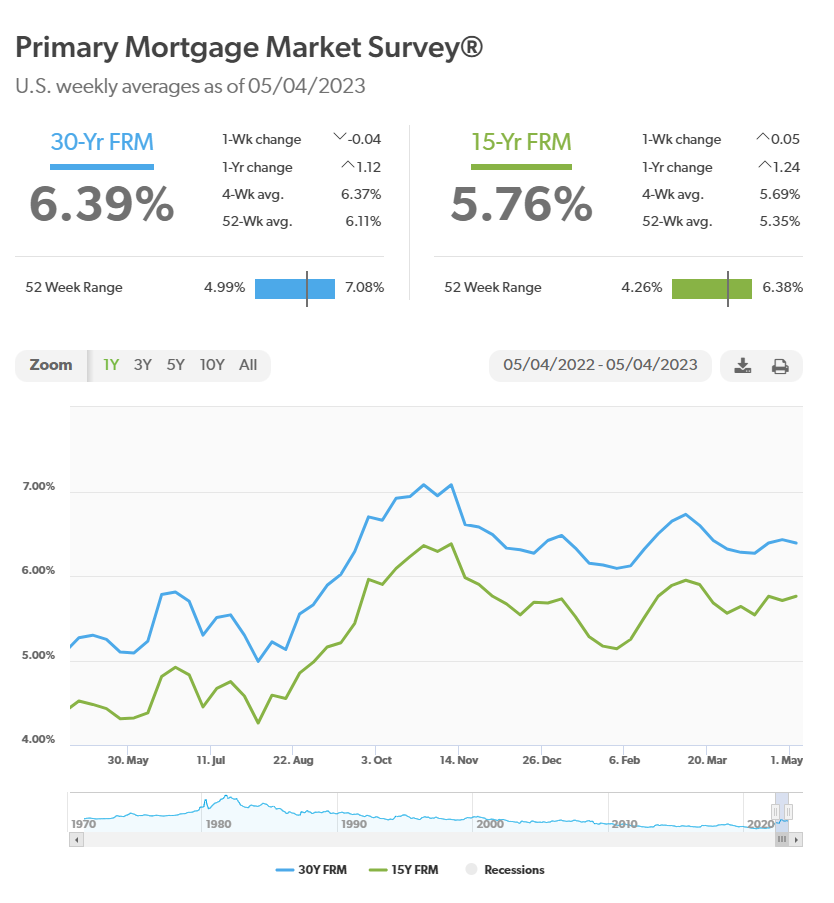

After rising for two straight weeks, the 30-year, fixed mortgage rate slipped back this week, according to Freddie Mac.

The government-sponsored enterprise on Thursday released the results of its Primary Mortgage Market Survey (PMMS), showing the 30-year fixed-rate mortgage (FRM) averaged 6.39%, down slightly from 6.43% a week earlier.

The 15-year, fixed mortgage rate posted a small increase.

“This week, mortgage rates inched down slightly amid recent volatility in the banking sector and commentary from the Federal Reserve on its policy outlook,” said Sam Khater, Freddie Mac’s chief economist. “Spring is typically the busiest season for the residential housing market and, despite rates hovering in the mid-6% range, this year is no different. Interested homebuyers are acclimating to the current rate environment, but the lack of inventory remains a primary obstacle to affordability.”

According to the PMMS:

- 30-year fixed-rate mortgage averaged 6.39%t as of May 4, down from 6.43% last week. A year ago at this time, it averaged 5.27%.

- 15-year fixed-rate mortgage averaged 5.76%, up from 5.71% last week. A year ago it averaged 4.52%.

Freddie Mac’s PMMS is focused on conventional, conforming, fully amortizing home purchase loans for borrowers who put 20% down and have excellent credit.

Low Inventory

Jiayi Xu, an economist with Realtor.com, said the slight increase must be put into context with the recent action taken by the Federal Reserve.

“The Federal Reserve Bank announced an interest rate hike of 25-basis points at its May FOMC meeting, setting the fed funds rate in the range of 5% to 5.25%, the highest since 2007,” Xu said. “As the Fed’s decision was well anticipated, the rate hike is unlikely to cause significant changes in mortgage and other interest rates.”

She continued, “The higher rates will continue to slow economic growth toward the target rate of 2%. However, as the impacts of earlier rate increases continue to work through the economy and the recent bank failures reveal the impact of higher rates, there is a risk of the U.S. economy entering a recession.”

She noted that the housing market is moving slower this spring, primarily because mortgage rates are elevated, which leaves many potential sellers “locked in,” with existing mortgages with rates far below the current level.

“In a typical year, we would expect to see the number of homes for sale begin to increase more significantly from this point forward,” Xu said. Instead, she said, “locked-in” owners plan to wait “until rates come down before selling, leading to fewer newly listed homes than a year ago.”

As a result, buyers are frustrated by the limited options of existing homes available and are turning to new construction.

“In addition, starting May 1st, the Federal Housing Finance Agency (FHFA)’s new loan-level price adjustments (LLPAs) could further complicate things for middle-class buyers who typically have high credit scores,” Xu said. “According to this new policy, well-qualified borrowers with scores ranging from 680 to above 780 may need to pay slightly more than before to offset the reduction in fees charged to buyers with low credit scores.”