Mortgage applications for new home purchases increased 0.6% in March from a year earlier, the Mortgage Bankers Association (MBA) said Tuesday.

The MBA’s Builder Application Survey (BAS) data for March 2023 also showed that such applications in March increased by 10%, not seasonally adjusted, from February.

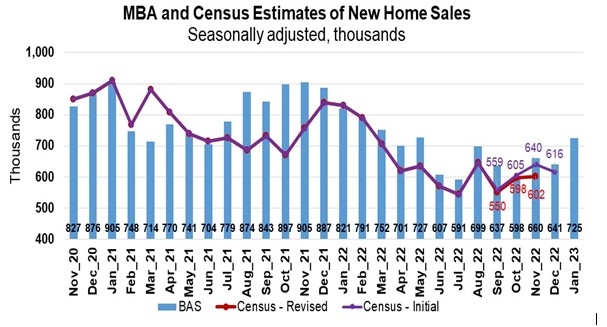

“Low for-sale inventory continues to constrain sales, along with mortgage rates that remain above 6%,” said Joel Kan, MBA’s vice president and deputy chief economist. “MBA’s estimate for new home sales was down 3% from the previous month. New home sales will be key to the housing market recovery in 2023, as they account for an increasing share of purchase activity as home builders maintain construction levels and offer concessions for buyers.”

On the other hand, Kan said, “existing home inventory remains low as many current homeowners are locked in to their homes with a lower mortgage rate.”

MBA estimates that new single-family home sales — which consistently has been a leading indicator of the U.S. Census Bureau’s New Residential Sales report — were running at a seasonally adjusted annual rate of 666,000 units in March 2023, based on data from the BAS. The new home sales estimate is derived using mortgage application information from the BAS, as well as assumptions regarding market coverage and other factors, the MBA said.

The seasonally adjusted estimate for March is a decrease of 3.2% from the February pace of 688,000 units. Unadjusted, the MBA estimates there were 65,000 new home sales in March 2023, an increase of 6.6% from 61,000 new home sales in February.

By product type, conventional loans made up 66.4% of loan applications, FHA loans made up 22.6%, RHS/USDA loans comprised 0.3%, and VA loans comprised 10.7%, the MBA said.

The average loan size of new homes ticked up just 0.02%, rising from $406,953 in February to $407,015 in March.

MBA’s Builder Application Survey tracks application volume from mortgage subsidiaries of home builders across the country. Using this data, as well as data from other sources, MBA provides an early estimate of new home sales volumes at the national, state, and metro level. It also provides information about the types of loans used by new home buyers.

Official new home sales estimates are conducted monthly by the Census Bureau. In that data, new home sales are recorded at contract signing, which is typically coincident with the mortgage application.