A report released today by the Urban Institute shows mortgage loan originator profitability continues to drop. That aligns with a projected sharp decline in refinancing.

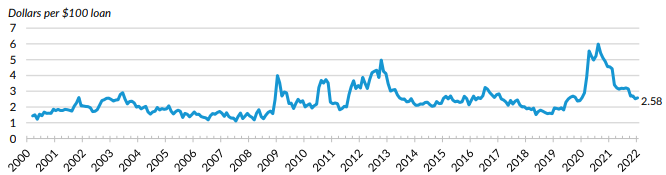

The nonprofit research institute reports that, in January 2022, Originator Profitability and Unmeasured Costs (OPUC) stood at $2.58 per $100 loan, a decrease from December 2021. The continued decline reflects the fact that the backlog of refinance has been processed, and originators are competing more aggressively on price.

OPUC, formulated and calculated by the Federal Reserve Bank of New York, is considered a good relative measure of originator profitability. OPUC uses the sales price of a mortgage in the secondary market (less par) and adds two sources of profitability; retained servicing (both base and excess servicing, net of guaranteed fees), and points paid by the borrower.

A high OPUC generally occurs when interest rates are low, originators are capacity constrained due to high refinance demand, and no incentive exists to reduce rates. A low OPUC occurs when interest rates are higher and refi activity low, competition forces originators to lower rates, which sends profitability down.

The OPUC number should continue to weaken; the Urban Institute predicts a drop in origination volume for 2022 driven by a sharp decline in refinancing.

The institute reported Fannie Mae, Freddie Mac, and the Mortgage Bankers Association estimate 2022 origination volume to be between $2.6 trillion and $3.34 trillion, down from $3.99 trillion to $4.65 trillion in 2021. By most estimates, 2021 was the highest origination year of the 21st century, with volumes surpassing 2020, the year with the previous record.

Strong refinance activity drove the robust origination volume in 2020 and 2021. All three groups expect the 2022 refinance share to be 18 to 26 percentage points lower than in 2021.

The 30-year fixed-rate mortgage continues to remain the bedrock of the U.S. housing finance system, accounting for 75.8% of new originations in December 2021. The share of 15-year fixed-rate mortgages, predominantly a refinance product, was 14.3% of new originations, according to the Urban Institute, which added the ARM share accounted for 1.5% of new originations.

As rates have started rising and the bulk of rate-refinance activity is in the rearview mirror, the cash-out share increased to 59.8% in January 2022. Despite the increase in the cash-out share, the absolute volume of cash-out refinances is relatively stable, the report said.