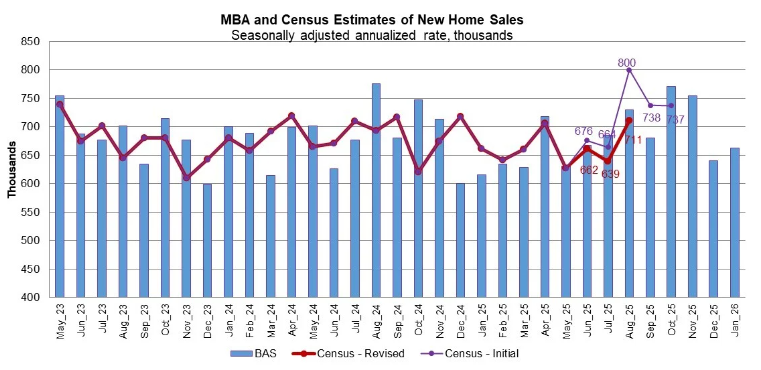

New home purchase mortgage applications increased modestly in January, signaling steady demand despite ongoing affordability challenges and elevated mortgage rates, according to the latest data from the Mortgage Bankers Association (MBA).

MBA’s Builder Application Survey showed that applications for mortgages to purchase newly built homes rose 2% compared to December, reflecting incremental improvement as the housing market begins the year on firmer footing. The gain suggests continued interest in new construction, even as affordability constraints and economic uncertainty continue to influence buyer behavior.

On a year-over-year basis, purchase mortgage applications for new homes declined compared to January 2025, underscoring the uneven pace of recovery following a period marked by higher borrowing costs and constrained housing supply. While mortgage rates have moderated from recent peaks, financing conditions remain tighter than the historically low levels seen earlier in the decade.

“New home purchase activity strengthened in January, as both mortgage applications and new home sales saw gains,” said Joel Kan, MBA’s vice president and deputy chief economist. “This increase was consistent with single-family housing starts finishing 2025 at a stronger pace even as permitting stayed relatively flat. MBA’s January estimated sales pace for newly built homes rebounded slightly from December to a pace of 663,000 units as buyers continue to use builder concessions and ARM loans. The average loan size of a purchase application was $385,506, the highest in 11 months.”

Builders continue to play an increasingly important role in supporting housing inventory and facilitating transactions. With resale inventory still limited in many markets, newly constructed homes are helping fill supply gaps and provide buyers with more options. Builders have also relied on incentives such as rate buydowns and pricing adjustments to help maintain sales momentum and attract qualified borrowers.

Persistent affordability challenges, including high housing price-to-income ratios and elevated land and construction costs, helped push builder confidence lower for the second straight month to start the year, according to the National Association of Home Builders (NAHB).

Builder confidence in the market for newly built single-family homes fell slightly in February, according to the National Association of Home Builders (NAHB)/Wells Fargo Housing Market Index (HMI).

“Housing affordability remains an ongoing challenge at the start of 2026,” said NAHB Chief Economist Robert Dietz. “The solution for the housing market is the enactment of policies that will bend the construction cost curve and enable additional supply of attainable housing. On the positive side, easing inflation should continue to allow lower interest rates for mortgages and builder loans.”

At the same time, underlying demand fundamentals remain intact, supported by demographic trends, household formation, and sustained interest in homeownership.

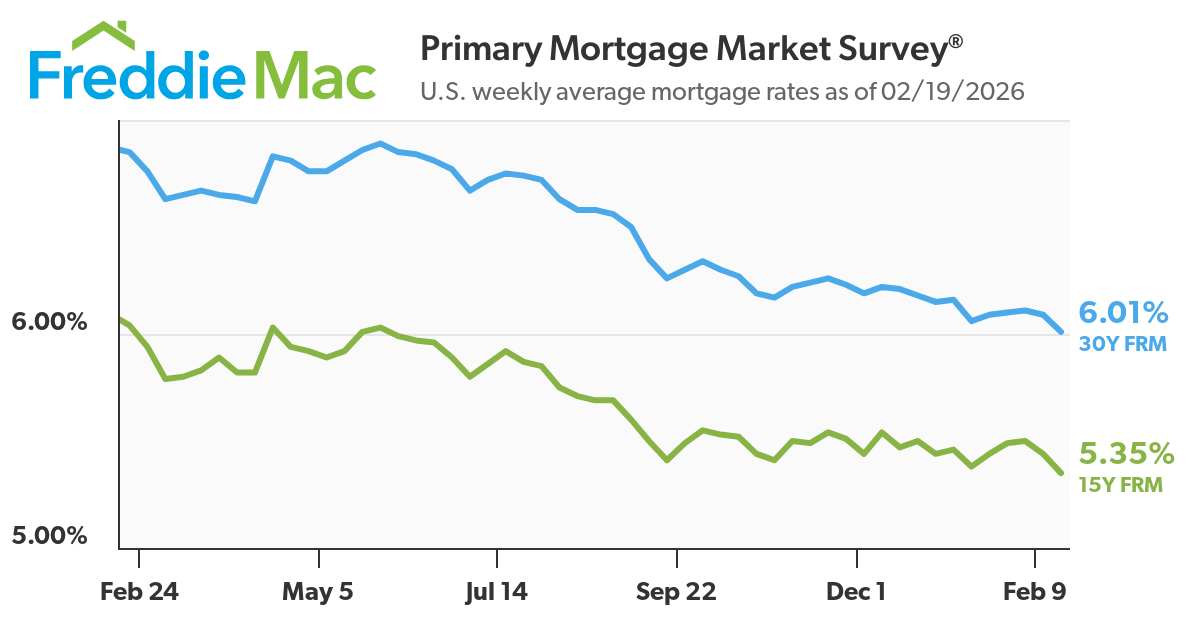

Freddie Mac reports the 30-year fixed-rate mortgage (FRM) averaged 6.01% as of February 19, 2026, down from last week when it averaged 6.09%. A year ago at this time, the 30-year FRM averaged 6.85%.

“Mortgage rates dropped again this week, now down to their lowest level since September of 2022,” said Sam Khater, Freddie Mac’s chief economist.

Recent mortgage application trends reflect a market gradually stabilizing following significant volatility in recent years. While overall application volumes remain below long-term averages, the latest increase in new home purchase applications suggests continued resilience in buyer demand and highlights the importance of new construction in supporting overall housing market activity.