Reverse mortgages have been around for decades, yet the product still generates more than its fair share of confusion and apprehension.

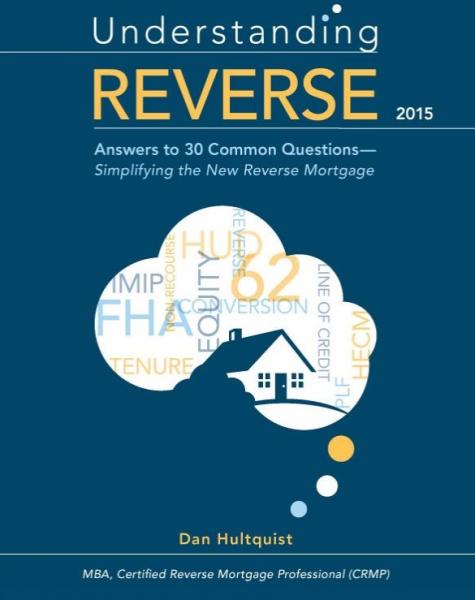

In an attempt to answer the many questions and concerns surrounding this product, Dan Hultquist, a Certified Reverse Mortgage Professional who serves on the Independent Certification Committee with the National Reverse Mortgage Lenders Association (NRMLA), has authored the book Understanding Reverse: Answers to 30 Common Questions—Simplifying the New Reverse Mortgage. Hultquist has also launched an accompanying blog, www.understandingreverse.com, to further clarify any issues surrounding the product.

Hultquist, who is also opening a Reverse Mortgage Branch of OpenMortgage covering the state of Georgia, spoke with National Mortgage Professional Magazine about his new publishing endeavor.

What inspired you to write this new book?

What inspired you to write this new book?

Dan Hultquist: I found myself answering the same questions, like “what happens to the home when I die?” In addition, I found that answering one question naturally steered the listener to ask predictable follow-up questions like, “what other maturity events cause the loan to be due?” or “does the reverse mortgage stick my heirs with a bill?” The fully-compliant answers to these questions are important to know, but I also feel it is necessary to document the relevant government regulations that apply to each question.

Reverse mortgages never quite broke through as a mainstream product, despite being around for many years. Why aren't they more popular?

Hultquist: There are many reasons. First, there is a stigma that this product is only for the desperate and needy. That is clearly not true. There are financial planning advantages that are only now being recognized by the financial planning community.

If you ask a seasoned professional in my industry whether they would encourage a family member to get one, they would likely say YES, even if the family member is unlikely to “need” one in a traditional sense. That is simply because they know how to maximize the use of the product as a form of insurance and comprehensive planning solution, instead of a cash-out refinance.

Second, there is a perception that it is an expensive product. It can surely be expensive if viewed simply as a mortgage or a short-term financial solution. For the right homeowner, using it as a supplement to retirement planning, it can be very inexpensive.

Third, the reverse mortgage is a highly-regulated and complex transaction that is a three-way agreement between the federal government, a lender, and a homeowner. I believe they would be more mainstream if they were better understood. Hopefully the book will simplify the product and increase the popularity.

There have been many negative press reports and commentaries relating to reverse mortgages, with people like CNBC’s Suze Orman among the most passionate critics of the product. How can the industry respond to this bad press?

There have been many negative press reports and commentaries relating to reverse mortgages, with people like CNBC’s Suze Orman among the most passionate critics of the product. How can the industry respond to this bad press?

Hultquist: The reverse mortgage is complicated niche product, and so we cannot expect the entire press to understand all of the advantages. But there have been high-profile advisers have been irresponsible in their coverage. We will continue to educate, but the best way to counteract the bad press is by asking the borrowers themselves if it solves a problem for them or increases their quality of life. Consumer satisfaction with this product has historically been very high.

One could assume that reverse mortgage volume will grow as the number of seniors increases over the coming years. But is that a false assumption to make?

Hultquist: The reverse mortgage was created, in part, to address the needs of baby boomers. It was to add a fourth leg to their retirement planning stool–Social Security, pension, retirement savings, and what I do, home equity conversion. So as the largest wave of baby boomers turns 62, the usage should increase, but there are other dynamics at play. There are concerns about social security and when to draw it, pension plans are often not available, and retirement savings are either insufficient or non-existent.

Fortunately, many seniors have a large nest egg in their home equity. Most assume the only way to crack that nest egg is by selling the home and downsizing. As more seniors begin to understand how they can access those funds through monthly payments, the reverse mortgage volume should increase.

What feedback have you gotten for your book?

Hultquist: The feedback has been tremendous. Whether they are financial planners that were not accustomed to explaining the product, or other industry professionals that need to be more compliant in their explanations, the response has been very good.