RealtyTrac has reported identifying county-level housing markets with early warning signs of a possible home price bubble—where prices overinflate and eventually decline. The report also identified markets with little risk for a home price bubble. The report analyzed 475 U.S. counties with a combined population of more than 221 million—accounting for more than 70 percent the total U.S. population—based on three early warning signs of a possible home price bubble: If the market was less affordable in October 2014 than its peak price during the 2005 to 2008 housing bubble; if a market was less affordable in October 2014 than its historical affordability average since January 2000; and if a market had a rising foreclosure rate on loans originated in 2014 compared to loans originated in 2013.

In the 475 counties analyzed, buying a median-priced home in October 2014 required 26 percent of median income on average compared to an average of 41 percent of median income in each county’s respective peak month during the housing bubble. The historical affordability average going back to January 2000 for all 475 counties was 28 percent of median income needed to purchase a median-priced home. Meanwhile the average foreclosure rate among the 475 counties on loans originated in 2014 was 0.25 percent, up from an average of 0.20 percent for loans originated in 2013.

“Affordability and foreclosure rates by loan vintage are two key metrics that will help consumers, investors, institutions and policy makers identify if a housing market is at risk for another price bubble,” said Daren Blomquist, vice president at RealtyTrac. “While 99 percent of markets have not returned to the irrational affordability levels during the previous housing bubble, one in five markets have now exceeded their historical affordability norms, which is a strong sign that either a new home price bubble is forming in those markets or that home price appreciation will soon plateau until incomes can catch up."

“Meanwhile, foreclosure rates on loans originated in 2014 are still significantly lower than for loans originated during the previous housing bubble in most markets, but there was an uptick in foreclosure rates on 2014 vintage loans compared to 2013 vintage loans in more than one-third of the counties we analyzed,” Blomquist said. “This is concerning given that the 2014 loans are newer and have had less time to sour than loans originated in 2013.”

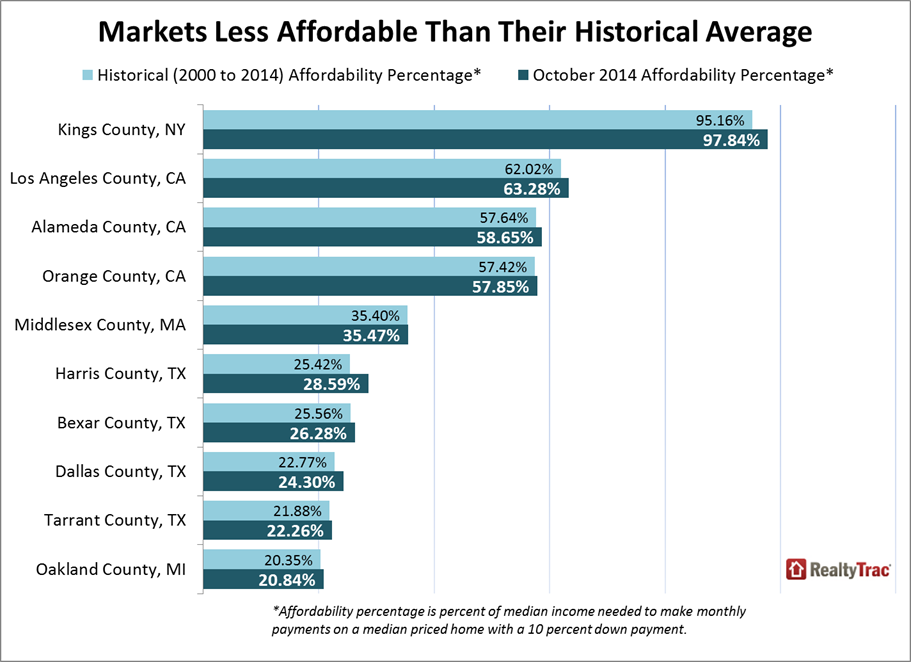

There were 98 counties (21 percent of all counties analyzed) with a combined population of nearly 62 million where the October affordability percentage was higher than the county’s historical average affordability percentage, including Los Angeles County, Calif., Harris County, Texas in the Houston metro area, Orange County, Calif., in the Los Angeles metro area, Kings County (Brooklyn), N.Y., Dallas County, Texas, Bexar County, Texas in the San Antonio metro area, Alameda County, Calif., in the San Francisco metro area, Middlesex County, Mass., in the Boston metro area, Oakland County, Mich., in the Detroit metro area and Travis County, Texas, in the Austin metro area.

There were 30 counties (six percent of all counties analyzed) with a combined population of nearly 19 million where the October affordability percentage was above the historical average and where foreclosure rates on 2014 vintage loans were higher than foreclosure rates on 2013 vintage loans, including Kings County, N.Y. (Brooklyn), San Francisco, San Mateo and Alameda counties in the San Francisco metro area, Suffolk County in the Boston metro area, Orange County in Southern California, Honolulu County, Hawaii, Denver County, Colo., Washington County, Utah in the St. George metro area, and Deschutes County, Ore., in the Bend metro area.

"We expect prices to peak in Q2 2015 before leveling off in the Southern California coastal markets,” said Chris Pollinger, senior vice president of sales at First Team Real Estate, covering the Southern California market.

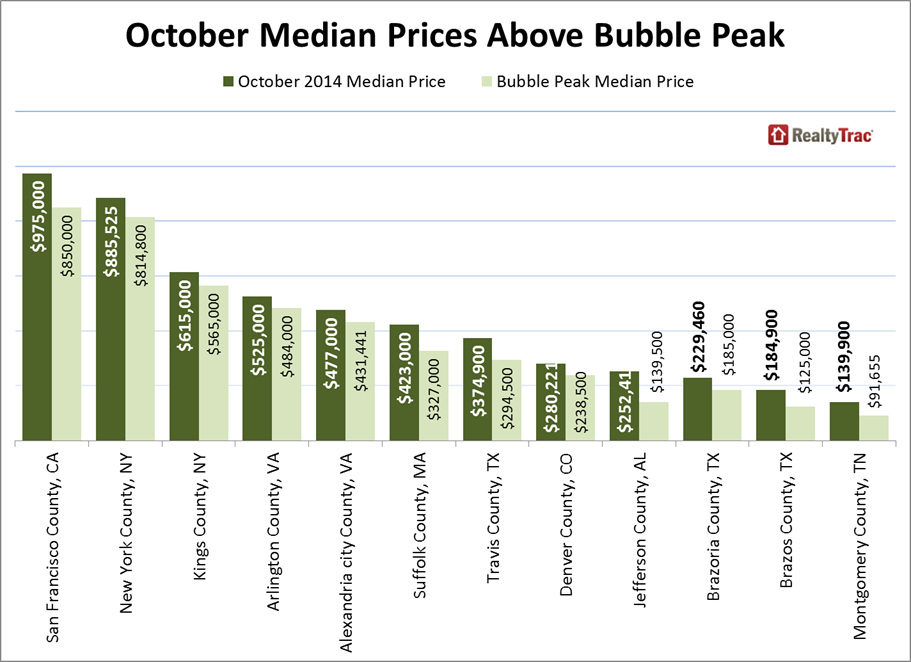

There were 58 counties (12 percent of all counties analyzed) with a combined population of more than 26 million where the median price of a home in October was higher than the peak during the housing bubble, including Kings County (Brooklyn) and New York County (Manhattan), N.Y., Travis County, Texas in the Austin metro area, Honolulu County, Hawaii, Fulton County, Ga., in the Atlanta metro area, Mecklenburg County, N.C., in the Charlotte metro area, Erie County, N.Y., in the Buffalo metro area, Wake County, N.C., in the Raleigh metro area, San Francisco County, Calif., and Monroe County, N.Y., in the Rochester metro area.

Thanks to lower interest rates and higher incomes in some of the 58 counties, there were only six counties nationwide where a median-priced home in October 2014 was less affordable for median income earners than at the peak of the 2005 to 2008 housing bubble: Suffolk County, Mass., in the Boston metro area, Travis County, Texas, in the Austin metro, Jefferson County, Ala., in the Birmingham metro area, Brazos County, Texas in the College Station metro, Allegan County, Mich., and Montgomery County, Tenn., in the Clarksville metro area.

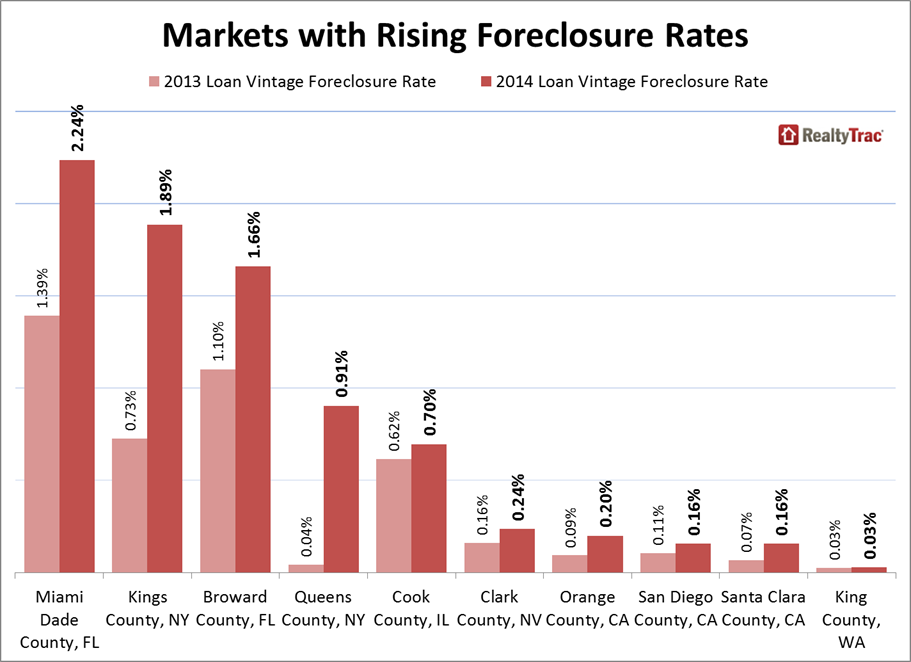

There were 178 counties (37 percent of all counties analyzed) with a combined population of nearly 100 million where the foreclosure rate on loans originated in 2014 was higher than the foreclosure rate on loans originated in 2013, including Cook County, Ill., in the Chicago metro area, San Diego and Orange counties in Southern California, Kings County (Brooklyn), N.Y., Miami-Dade County, Fla., Queens County, N.Y., Clark County, Nev. (Las Vegas), King County, Wash. (Seattle), Santa Clara County, Calif. (San Jose), and Broward County, Fla. (Miami).

“With the stiff competition for homes in Seattle, one might think that our market is well on its way to a bubble, but buyers have gotten more savvy and aren't overbidding at levels we saw a year or two ago,” said OB Jacobi, president of Windermere Real Estate, covering the Seattle market. All three counties in the Seattle metro were more affordable than their historical levels in October despite a slight increase in foreclosure rate in two of the three counties. “We also have a strong job market with wages that are keeping up with appreciation—especially in the growing tech sector. As a result, prices in Seattle are appreciating at a healthy pace, but they've slowed from the double digit increases we saw last year.”

There were 229 counties (48 percent of all counties analyzed) with a combined population of nearly 79 million where median home prices in October were more affordable than their historical averages and where foreclosure rates on 2014 vintage loans were flat or declining compared to foreclosure rates on 2013 vintage loans. Among these counties with a low risk of a home price bubble, the most affordable were in Lansing, Mich., Syracuse, N.Y., Buffalo, N.Y., Cincinnati, Ohio, and Atlanta, Ga.

“The Ohio markets have been fortunate through 2014 in showing continued modest gains regarding volume and prices reflective of a market in balance between home sellers and buyers, in contrast to concerns over a housing bubble being experienced in many other parts of the country,” said Michael Mahon, executive vice president and broker at HER Realtors, covering the Columbus, Cincinnati and Dayton, Ohio markets. “Growing job markets within the fields of medical, finance, construction, and education continue to supply increased demand for housing across Ohio, although concerns over consumers with increasing debt issues, particularly in the fragile first time home buyer sector, could provide for a slight decrease in demand for 2015.”