There was good and bad news this morning relating to homeowners facing financial difficulties.

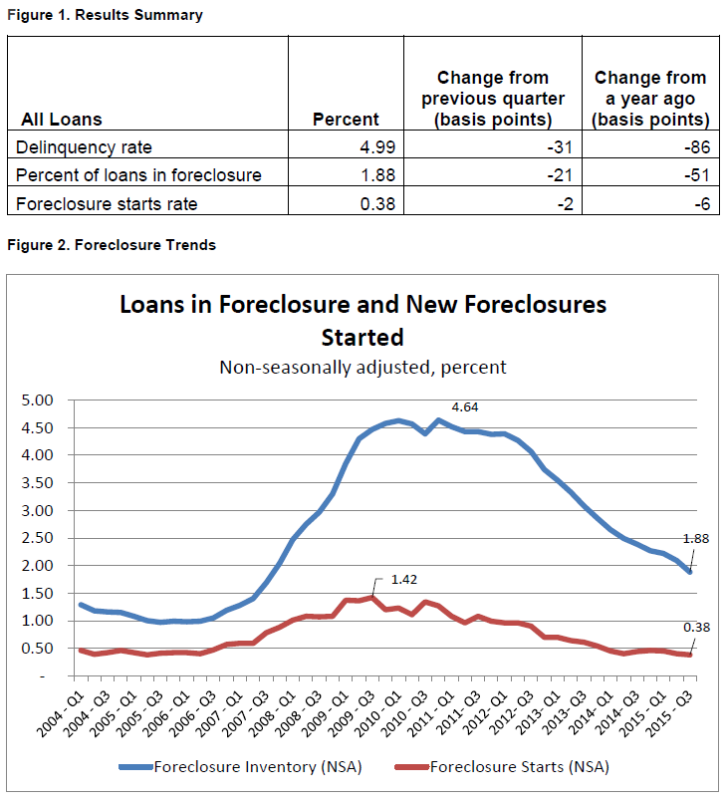

First, the good news: the new National Delinquency Survey released by the Mortgage Bankers Association (MBA) found the delinquency rate for mortgage loans on one- to-four-unit residential properties fell to a seasonally adjusted rate of 4.99 percent of all loans outstanding at the end of the third quarter, which is the lowest level since the first quarter of 2007. The delinquency rate decreased 31 basis points (bps) from the previous quarter, and 86 bps from one year ago.

The survey also determined that the percentage of loans on which foreclosure actions were started during the third quarter was 0.38 percent, down two bps from the previous quarter and down six bps from one year ago. The foreclosure starts rate is at the lowest level since the second quarter of 2005, the MBA added.

Furthermore, the serious delinquency rate—defined as the percentage of loans that are 90 days or more past due or in the process of foreclosure—ended the third quarter at 3.57 percent, a decrease of 38 bps from the second quarter and a decrease of 108 bps from last year. This was the lowest serious delinquency rate since the third quarter of 2007.

Marina Walsh, MBA’s vice president of industry analysis, noted the continued disparity in foreclosure activity between states with judicial and non-judicial solutions.

“While only 40 percent of loans serviced are in judicial states, these states account for a majority of loans in foreclosure,” said Walsh. “For states where the judicial process is more frequently used, 3.01 percent of loans serviced were in the foreclosure process, compared to 1.06 percent in non-judicial states. States that utilize both judicial and non-judicial foreclosure processes had a foreclosure inventory rate closer that of the non-judicial states at 1.26 percent. As has been the case since the fourth quarter of 2012, New Jersey, New York, and Florida had the highest percentage of loans in foreclosure in the nation. All three of these states primarily use a judicial foreclosure process.”

Now, the bad news: The latest S&P/Experian Consumer Credit Default Indices found the composite rate for consumer credit defaults last month was 0.94 percent, up five bps from the previous month. The first mortgage default rate measured 0.81 percent up five bps from the previous month, while the second mortgage default rate measured 0.56 percent, up nine bps from the previous month. The default rates on auto loans also rose in October while the bank card default rate fell two bps.

“Despite recent modest increases, consumer credit default rates remain at low levels,” said David M. Blitzer, managing director and chairman of the Index Committee at S&P Dow Jones Indices, adding that the potential for a rate hike in December by the Federal Reserve “is not expected to dampen consumer spending or lead to any near-term move in consumer credit defaults.”