The latest data view of the housing world found upward motion for mortgage applications and a slight disconnect between appraisal values and expectations by homeowners on what their properties are worth.

The Mortgage Bankers Association’s Weekly Mortgage Applications Survey for the week ending Dec. 4 found significant activity on unadjusted index levels. The Market Composite Index increased by 1.2 percent on a seasonally adjusted basis from one week earlier—but on an unadjusted basis, the index skyrocketed by 43 percent compared to the previous week. Likewise, the seasonally adjusted Purchase Index increased by a scant 0.04 percent from one week earlier, but the unadjusted soared by 36 percent compared to the previous week and was 29 percent higher than the same week one year ago.

The Refinance Index increased by four percent from the previous week, while the refinance share of mortgage activity increased to 58.7 percent of total applications from 56.6 percent the previous week. The government loan programs registered mixed results: the FHA share of total applications increased to 14 percent from 13.2 percent the week prior, but the VA share of total applications decreased to 10.8 percent from 11.3 percent one week earlier and the USDA share of total applications remained unchanged at 0.7 percent.

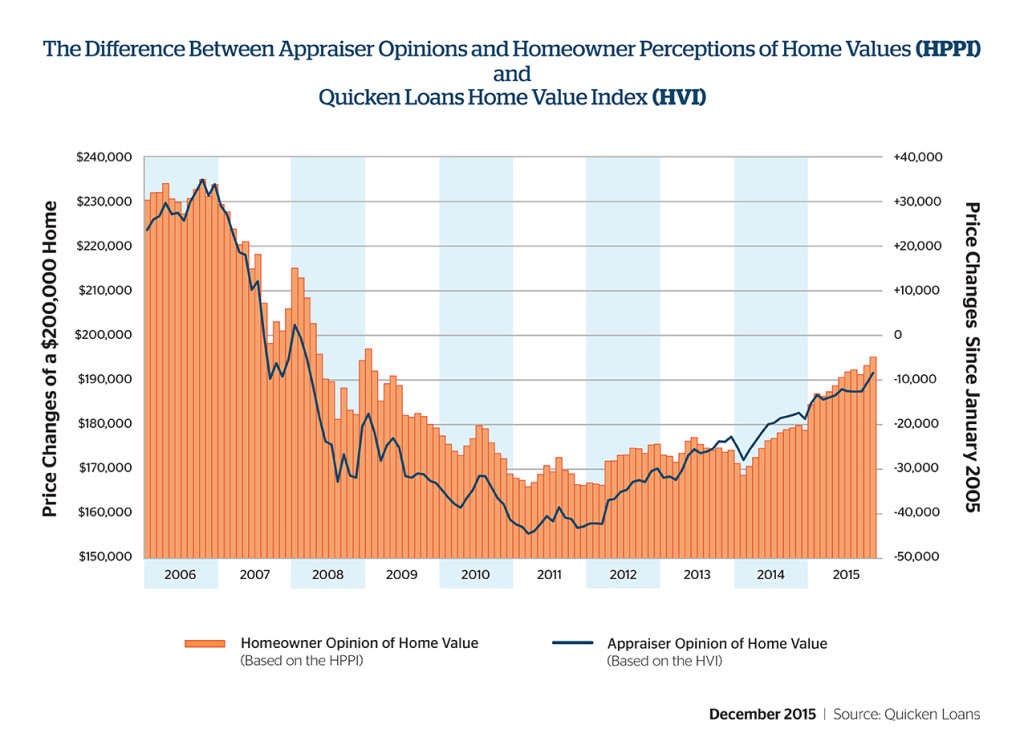

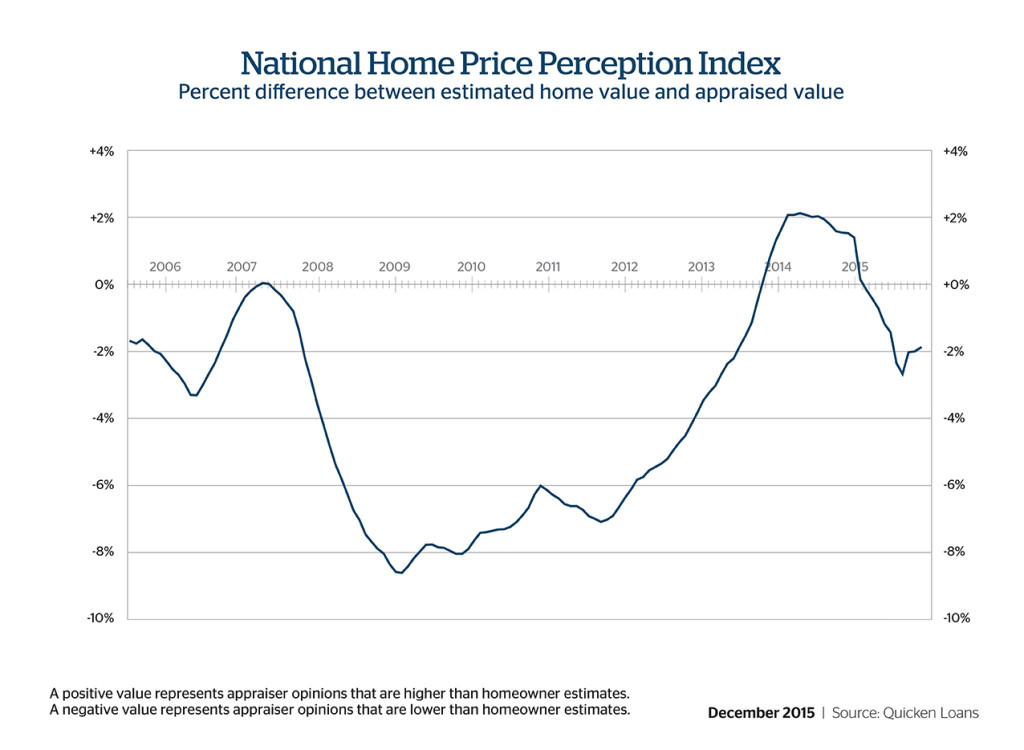

Separately, Quicken Loans’ latest Home Price Perception Index (HPPI) determined the average appraisal for November was 1.87 percent below the value the homeowner expected. This is the third consecutive month of HPPI data reporting where the gap between appraisal and owner estimates have narrowed.

However, appraised values on residential properties ticked upwards an average of 1.08 percent since October and increased 4.84 percent on a year-over-year measurement. Quicken Loans found that home values in the West have grown significantly since last year (up 7.16 percent) while the Midwest and Northeast have lagged behind (0.77 percent and 0.91 percent, respectively).

“Home values continue to be driven higher as the economy improves and the desire for homeownership increases,” said Bob Walters, Quicken Loans’ chief economist. “Gains aren’t equal. In some areas, demand is robust, leading to considerable home value increases. Other markets are more balanced, resulting in more steady, measured home value growth.”