Regulation Z requires that the Consumer Financial Protection Bureau (CFPB) to make annual adjustments to the dollar amount thresholds under the HOEPA "points and fees" provisions of Regulation Z §1026.32(a)(1)(ii) (Section 32) and the qualified mortgage "points and fees" provisions under Regulation Z §1026.43(e)(3)(ii) based on changes in the Consumer Price Index for All Urban Consumers (CPI-U). For 2016, the dollar amount adjustments reflect a two percent decrease in the CPI-U.

HOEPA points and fees thresholds

The CFPB issued a final rule, effective Jan. 1, 2016, providing that the dollar amount of the HOEPA fee-based trigger will decrease to $1,017. Additionally, the total loan amount threshold used to determine whether a loan is subject to the "total points and fees" provisions of HOEPA, or Section 32, is $20,350.

The fee-based trigger is used to determine whether the total points and fees payable by the consumer at or before loan closing subjects that loan to Section 32. Section 32 applies, in part, to certain loans if the total points and fees payable by the consumer at or before loan closing exceed the greater of eight percent of the total loan amount or a dollar amount threshold.

In addition to the Federal Section 32 test, this annual adjustment affects the anti-predatory loan laws in the following states: Colorado, Florida, Maryland, Massachusetts, Oklahoma, Pennsylvania, Texas and Utah.

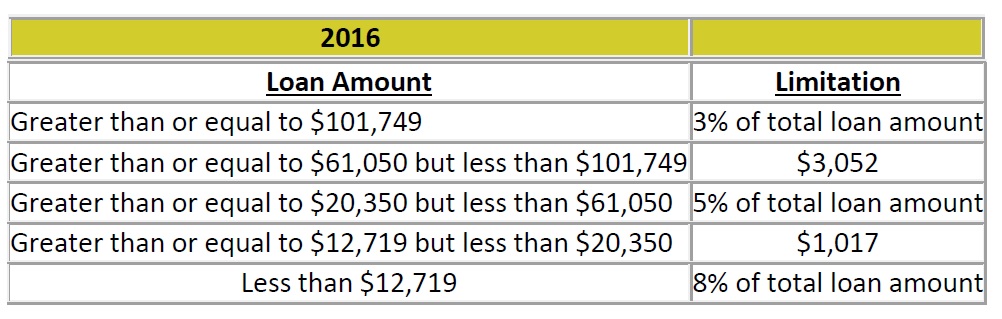

Qualified mortgage points and fees thresholds

In addition, the final rule updates the dollar amount thresholds for determining whether a loan is a qualified mortgage under the "points and fees" provision specified in Regulation Z Section 1026.43(e)(3)(ii), as follows:

No changes to 2016 conventional loan limits

The Federal Housing Finance Agency (FHFA) has announced that, except for 39 counties in which high-cost area loan limits have increased, the 2016 maximum conforming loan limits for first-lien and second-lien loans will remain unchanged from the maximum conforming loan limits for 2015.

Note that loan limits apply to the original loan amount of the mortgage loan, not to its balance at the time of purchase by Fannie Mae, and the loan origination date is the date of the note. For more detailed information about conventional conforming loan limits for 2016, please refer to Fannie Mae’s Lender Letter 2015-07 and Fannie Mae’s Web site.

Melanie A. Feliciano Esq. is DocMagic Inc.’s chief legal officer and currently serves as editor-in-chief of DocMagic’s electronic compliance newsletter, The Compliance Wizard. She received her JD from the Georgetown University Law Center, and is licensed in California and Texas. She may be reached by phone at (800) 649-1362 or e-mail [email protected].

This article originally appeared in the January 2016 edition of National Mortgage Professional Magazine.