April 2024 (Q1) Senior Loan Officer Opinion Survey on Bank Lending Practices shows weakening demand for consumer loans.

The Federal Reserve Senior Loan Officer Opinion Survey on Bank Lending Practices (SLOOS) recently published its findings for the first quarter of 2024, addressing lending standards, terms, and demand for bank loans among businesses and households.

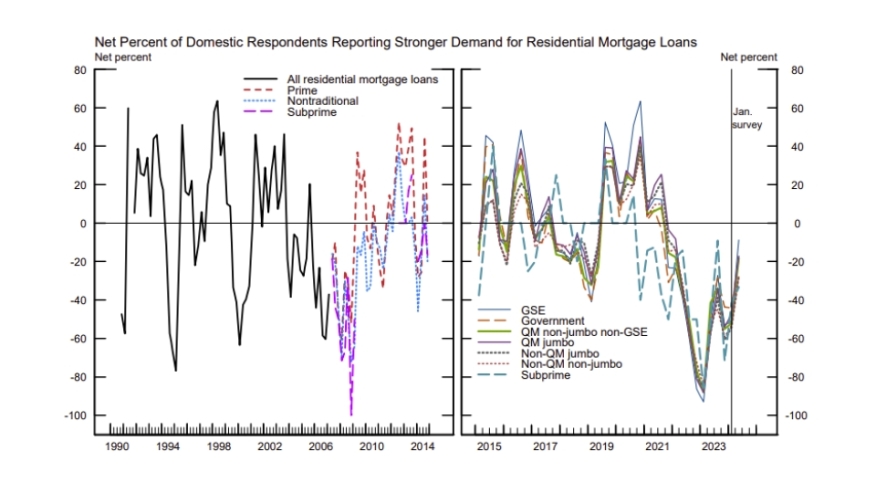

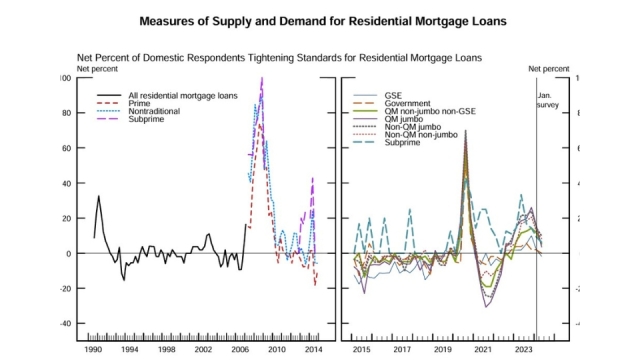

For households, a modest net share of banks reported that lending standards tightened across some categories of loans, including Non-QM jumbo, Non-QM non-jumbo, subprime, and qualified mortgage (QM) non-jumbo, non-GSE-eligible mortgage loans. Lending standards remained about the same for GSE-eligible mortgages, government mortgages, and QM jumbo mortgages.

Large banks reported net easing of standards, while other banks reported net tightening of standards for most residential real estate (RRE) loans. Additionally, a moderate net share of banks reported weaker demand for HELOCs.

Federal Reserve Board, April 2024 Senior Loan Officer Opinion Survey on Bank Lending Practices shows bank lending standards tightening.

Over the first quarter, banks reported tightening lending standards and most terms, on net, for all consumer loan categories, including credit card loans.

Significant net shares of banks reported tightening lending standards for credit card loans, but only moderate and modest net shares of banks reported tightening standards for other consumer loans and auto loans, respectively.

Get the NMP Daily

Essential stories, every weekday.

Additionally, a significant net share of banks reported increasing the minimum credit score requirements for credit card loans, while only a moderate net share of banks reported doing the same for other consumer loans. Plus, a modest or moderate net share of banks reported decreasing the extent to which loans are granted to customers not meeting credit scoring thresholds and increasing spreads of interest rates over the cost of funds for all consumer loan categories.

Other queried terms and conditions were left unchanged on those loans, except for the credit limits for credit card loans.

As for demand, a moderate net share of banks reported weaker demand for credit card loans and other consumer loans in the first quarter. Also, a significant net share of banks reported weaker demand for auto loans.

Seller/servicers using artificial intelligence in origination or servicing must have formal policies, oversight, and vendor controls in place

Fannie Mae’s artificial intelligence and machine-learning governance requirements take effect Thursday, Aug. 6, giving approved seller/servicers a final deadline to formalize how the technology is used across mortgage origination and servicing.The requirements apply when a s...

Pending sales fell to their lowest level since early April, but lower asking prices and reduced competition give originators more options to structure deals for qualified borrowers

Higher mortgage rates are thinning the purchase pipeline, even as lower asking prices and reduced competition give borrowers still in the market more leverage.Seasonally adjusted U.S. pending home sales totaled 322,739 during the four weeks ending July 26, their lowest level...

Pending sales fell to their lowest level since early April, but lower asking prices and reduced competition give originators more options to structure deals for qualified borrowers

Price cuts and longer listing times are creating opportunities for loan officers to help borrowers negotiate seller concessions, but leverage varies sharply by metro