Substantial home equity has boosted consumer financial health, but risks remain in non-mortgage consumer lending

“Persistently resilient” describes U.S. consumers according to DoubleLine Portfolio Manager Andrew Hsu and ABS Trader Michael Fine in their newly published research, "The State of the U.S. Consumer Through the Lens of Asset-Backed Securities.” That consumer resilience is backed, they say, by a lot of home equity.

By leveraging asset-backed security (ABS) loan data with macroeconomic data, the asset management firm DoubleLine formed a comprehensive view of the U.S. consumer that offers perspective on their economic/financial health. The authors of the study, Hsu and Fine, conclude that consumer resilience has been fueled by the strength of the residential mortgage market, a healthy labor market, and excess savings accumulated during the pandemic.

A gradual slowdown in prepayment speeds indicates that consumers are still largely able to meet their obligations despite higher borrowing costs, the study found. Plus, overall delinquencies have remained low in the past two years, especially mortgage delinquencies, which are below the long-term historical average.

Low rates of mortgage default and substantial home equity have provided a buffer against financial stress for homeowners. Also, because of consumers’ resilience, the authors of the study believe it suggests the possibility of pulling off an economic soft landing.

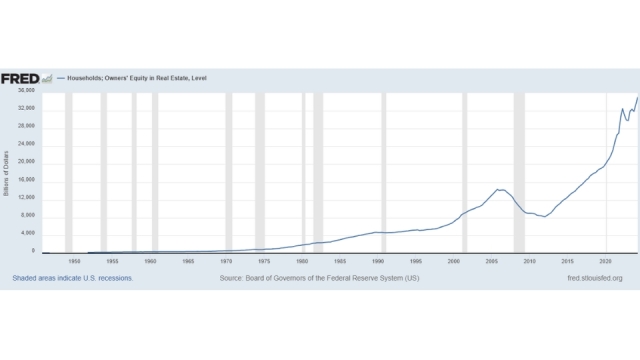

Owners' equity in real estate from January 1952 to January 2024. As property values increase, so does homeowners' financial security.

However, the authors note that "potential risks to the consumer persist, including the depletion of these savings, wage stagnation, a recent rise in unemployment and ongoing high consumer prices, notwithstanding cooling in the year-over-year rate of inflation."

Get the NMP Daily

Essential stories, every weekday.

Credit card delinquencies, for example, have been climbing. The study highlights how the rise in delinquencies in other sectors of consumer lending suggest growing financial stress among consumers, especially those with weaker credit profiles. Although defaults have remained low, the authors predict that default levels could rise if economic conditions worsen.

Still, an apparent improvement in underwriting and lending practices as observed from the average FICO score among vintage ABS loan pools also provide a positive sign of consumer financial health, per DoubleLine's report. ABS deals in 2021 have an average FICO score of 680, whereas 2024 deals have an average of 724, rendering a decreased likelihood of default.

The authors report that DoubleLine continues "to find attractive relative value in select areas of the ABS consumer market. While prepayments, defaults and loss severities require close monitoring, they all remain within reasonable historical average moving bands."

Seller/servicers using artificial intelligence in origination or servicing must have formal policies, oversight, and vendor controls in place

Fannie Mae’s artificial intelligence and machine-learning governance requirements take effect Thursday, Aug. 6, giving approved seller/servicers a final deadline to formalize how the technology is used across mortgage origination and servicing.The requirements apply when a s...

Pending sales fell to their lowest level since early April, but lower asking prices and reduced competition give originators more options to structure deals for qualified borrowers

Higher mortgage rates are thinning the purchase pipeline, even as lower asking prices and reduced competition give borrowers still in the market more leverage.Seasonally adjusted U.S. pending home sales totaled 322,739 during the four weeks ending July 26, their lowest level...

Pending sales fell to their lowest level since early April, but lower asking prices and reduced competition give originators more options to structure deals for qualified borrowers

Price cuts and longer listing times are creating opportunities for loan officers to help borrowers negotiate seller concessions, but leverage varies sharply by metro