Mounting consumer debt and loan delinquencies are putting a damper on the financial outlook for many American households, according to a new report from Achieve, a digital personal finance company, and its think tank, the Achieve Center for Consumer Insights.

In a survey of 2,000 consumers, nearly one-third of consumers said it is difficult or very difficult for them to pay their recurring debts on time, the report stated.

“We know that household debt and credit are growing at an alarming pace,” said Achieve co-founder and co-CEO Andrew Housser. “ Skipping payments on financial obligations in order to afford essentials is the type of decision driving more everyday people deeper into debt. This research highlights the choices that many consumers have to make month after month to simply stay afloat."

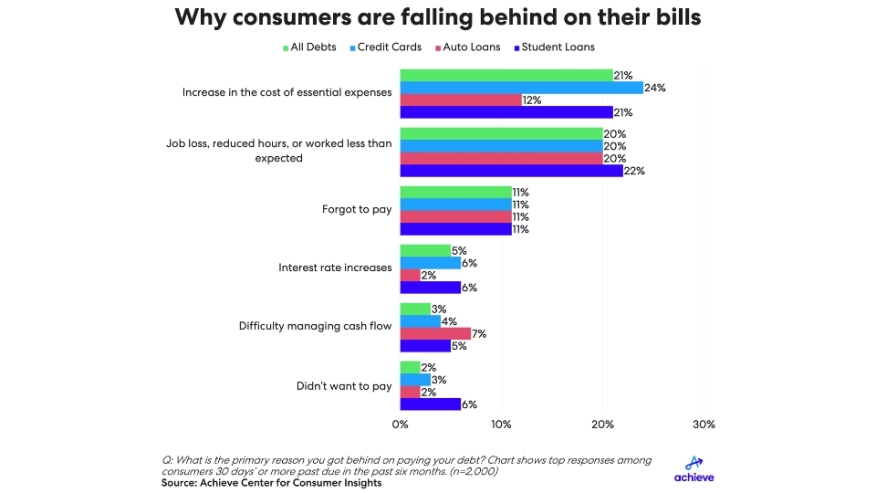

The report analyzes why consumers are falling behind on their bills and mortgage professionals may be surprised the biggest culprit cited among consumers 30 days or more past due on debt payments wasn’t interest rates. Rather, the most popular reasons cited were inflated costs of essentials (21%), job loss or reduced hours (20%), and forgetting to pay (11%).

"For many consumers, money is going out the door as quickly as it's coming in, if not faster," Housser said.

Among consumers who had a recent credit card delinquency, 6% said interest rate increases made paying difficult. Among delinquent auto loan borrowers, 7% cited difficulty managing cash flow between when respondents receive income and their payment due dates. In student loans, 6% of delinquent borrowers said they missed a payment because they didn't want to pay.

Additionally, among those respondents, 65% said it simply comes down to not having enough income to cover their spending. Other challenges include owing money on too many different accounts (39%); cash flow timing differences between when income is received and debt payments are due (27%) and difficulty keeping track of how much is owed across all their accounts (14%).

Consumers who struggle to make ends meet are often faced with difficult choices. In the past three months, 25% of survey respondents said they have reduced spending on basic needs; 18% have taken on additional credit card debt, and 11% report skipping payments on one or more of their bills.

For many consumers, having multiple bills due at once is another source of financial strain, according to another recent Achieve Center for Consumer Insights study on buy now, pay later lending. Difficulties stem from struggling to have money to make on-time payments and the complexity of managing a portfolio of accounts.