Carrying too much debt is delaying potential home buyers from achieving their aspirations for a median of three years, according to a new report. But for a third of all wannabes, it will be at least 10 years before they can buy a house.

The report from the National Association of Realtors (NAR) cites high rental costs as the main obstacle standing in the way of the 12% of all would-be buyers who are having difficulty accumulating the money for a down payment. Almost half of them say their main problem is rent or house payments.

But a third are stymied by credit card debt, student loans and car loans. Not just a third of all three types of debt, but a third for each one. About 1 in 8 said childcare expenses and/or health care costs were holding them back.

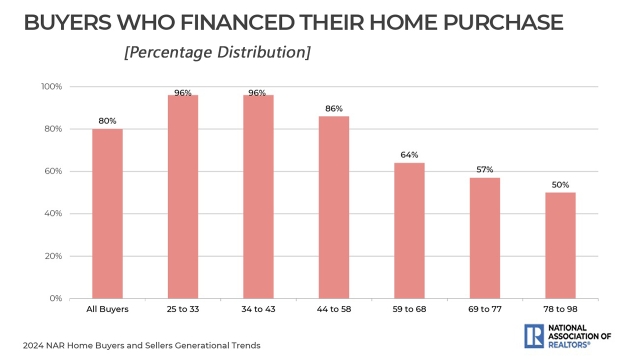

Despite these roadblocks, three out of every four buyers financed their homes, the latest edition of NAR’s Home Buyers and Sellers Generational Trends Report found, with 95% of those in the 26 to 34 and 35 to 44 age brackets taking out a mortgage. Even half of all seniors age 60 and over borrowed the money to buy their next house.

The report includes age-bracket breakdowns for each of these categories. Not surprisingly, for example, most of those finding it tough to raise a down payment were in the 26 to 34-year-old group. But citing unspecified “other” reasons, the survey found that a large percentage of those in the three oldest age cohorts – 60 to 69, 70 to 78 and 79 to 99 – also has issues.

Most buyers had no difficulty with the lending process, and 21% said it was easier than expected. But a significant 26% found it “somewhat” more difficult than expected or much more so. The senior age groups again were at the top of the list here with more problems navigating the application and approval process than other age groups.

Buyers had at least one loan application rejected, mostly because of loan-to-value ratios that were too high or credit scores that were too low. A significant 12% each were turned away because of insufficient income, insufficient reserves or incomes that could not be verified. But 13% said they had no clue why they were rebuffed.

When they did buy, buyers in all age cohorts overwhelmingly favored fixed-rate loans, and conventional loans over the government-backed variety. The median down payment was 15%, but seniors were able to put up 28% or more, with those over 79 putting down 38% of the purchase price.

In the end, three-quarters of all buyers used financing. But more than 90% of those 44 years and younger financed their purchases, whereas only 49% of Older Baby Boomers and 41% of the Silent Generation did the same.

On the seller side of the equation, the typical holding period for sellers was 10 years before moving on. But the houses these sellers bought were pretty much the same size as the ones they sold. More than 90% said they sold when they wanted to sell. Just 5% said they delayed selling because they owed more than their places were worth.

44% cut their asking price, but 55% got what they were asking or more. 7% sold for 110% or more of their listing price. 55% sold within four weeks of putting their houses on the market, but 10% nailed a buyer within 7 days.

Only one out of every four sellers offered an incentive to attract a buyer, with the most popular bonus being financial assistance with their closing costs.

The NAR report is based on 5,390 responses to a 127-question survey sent to people who purchased a primary residence between July 2023 and July 2024. It also contains data on the respondents’ characteristics, characteristics of the homes the bought, the search process and their experiences with the buying and selling process, including their dealings with realty agents and brokers.