Sales of existing homes may have hit bottom, according to a report released Wednesday by First American Financial Corp.

The Santa Ana, Calif.-based provider of title, settlement, and risk solutions for real estate transactions released its Potential Home Sales Model report for June, which includes an analysis of how sales of existing -homes fared in previous eras with rising mortgage rates.

First, the report said potential existing-home sales decreased to a 5.31 million seasonally adjusted annualized rate (SAAR), a 0.23% month-over-month decrease. This represents, however, a 52.4% increase from the market potential low point reached in February 1993, the report said.

The report also said the market potential for existing-home sales decreased by 2.8% compared with a year ago, a loss of 152,400 sales (SAAR)

It added that the potential existing-home sales are 1.49 million (SAAR), or 21.8%, below the peak of market potential, which occurred in April 2006.

The Potential Home Sales Model measures what a healthy market for home sales should be, based on the economic, demographic, and housing market environments.

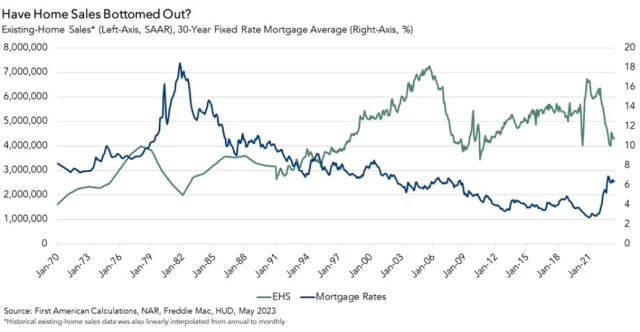

“Mortgage rates have risen substantially since the spring of 2022, and higher rates have a dual impact on sales — pricing out buyers who lose purchasing power and keeping some potential sellers rate-locked in,” said Mark Fleming, chief economist at First American. “Since the start of the latest rising mortgage-rate era, existing-home sales have declined by approximately 30%.”

Fleming added that “While higher mortgage rates reduce affordability, existing-home sales, historically, do not always fall when rates rise. In fact, existing-home sales are often more influenced by why mortgage rates are rising.”

Rate Analysis

That leads to First American’s analysis of past eras in which mortgage rates rose.

“Over the past 50 years, we’ve tracked 12 rising mortgage-rate eras and existing-home sales declined in only half of them,” Fleming said. “The 1977-1981 rising-rate era stands out because mortgage rates increased dramatically — from approximately 9% to 18.5%. During this period, the Federal Reserve hiked interest rates to tame out-of-control inflation. The result was a 43% decline in existing-home sales.”

He said the 2005-06 rising-rate era that preceded the 2008 housing crisis also stands out because sales fell dramatically.

“Rising mortgage rates in that period were driven by the Federal Reserve’s efforts to tame above-target inflation,” Fleming said. “The Fed’s moves worked, as existing-home sales declined by more than 12% in approximately one year. Existing-home sales also decreased in the 1994 rising-rate era, as the Fed increased the federal funds rate to prevent strong economic growth from feeding inflation.”

There are, however, other examples when existing-home sales proved resilient to rising-rate environments, he said.

One example: Mortgage rates spiked in the summer of 2013 when the Fed indicated it would taper its quantitative-easing policy of buying Treasury bonds and mortgage-backed securities.

“But this ‘taper tantrum’ had little impact on existing-home sales,” Fleming said.”Most recently, in 2017-18, it took almost a year of rising mortgage rates before the pace of existing-home sales declined below the pace seen before rates started to rise.”

Today’s Market

In the current rising-rate era, Fleming said, mortgage rates have increased by over 3.5 percentage points since the Fall of 2021, while existing-home sales have declined by approximately 30% over that same period. This housing market is particularly unique because most homeowners refinanced into rock-bottom, likely never-to-be-seen-again mortgage rates during the pandemic.”

He noted that more than 90% of homeowners in the U.S. have locked in a mortgage rate below 6%.

“As mortgage rates return to a not-so-new-normal of over 6%, those homeowners have a financial disincentive from selling, keeping a lid on the primary source of housing supply, and you can’t buy what’s not for sale,” Fleming said. “The good news is that home sales have likely already bottomed, and the pace of sales will begin to settle into a new normal below the breakneck pace of 2020 and 2021, but also not as low as earlier this year.”

Fleming added that the hope is “that affordability will improve in the second half of 2023, so that the pace of sales can be not too hot, not too cold, but just right.”