The value of homeownership continues to assert itself, with a new report by First American Data & Analytics showing how Americans who own their homes accumulate more wealth over time than those who rent the place in which they live.

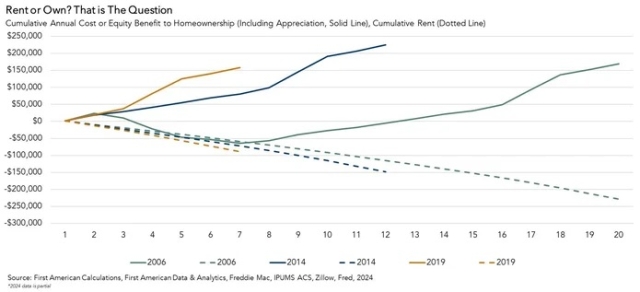

“In deciding whether to rent or own, it’s important to remember the wealth-building power of equity accumulation,” First American Chief Economist Mark Fleming said in his analysis of the company's latest Real House Price Index (RHPI) data, adjusted for income and interest rate changes. “Even homeowners who bought at the height of the housing boom in 2006 have gained $169,000 in equity, while renters over that same time period cumulatively lost $229,000 in wealth.”

The RHPI showed that prices decreased by 3.1% between August and Sept. 2024, falling 9.2% year-over-year.

Consumer house-buying power, or how much one can purchase based on changes in income and mortgage rates, increased 3.7% in September from the month prior and increased 14.5% year over year.

Affordability Still Below Average

Fleming emphasized that while improving affordability is providing some relief, it’s still a long way from the historical average.

“National affordability on an annual basis improved for the second consecutive month in September,” he explained. “Despite the recent improvement, affordability nationally as measured by the RHPI remains 36% below the pre-pandemic historical average.”

Two factors drove the 9.2% annual increase in affordability – a 3.1% annual increase in nominal household income and a one percentage point decrease in the 30-year, fixed mortgage rate compared with one year ago.

Nominal house price appreciation slowed nationally for the ninth consecutive month in September, while still reaching a record high. Lower mortgage rates and higher household income were enough to offset the price increase.

Despite the recent improvement, affordability nationally as measured by the RHPI, combined with data from the U.S. Census Bureau and Freddie Mac, remains 36% below the pre-pandemic historical average.

“For those trying to buy a home, house price appreciation can be intimidating and makes the purchase more expensive, all else held equal,” Fleming pointed out. “However, once the home is purchased, appreciation helps build equity in the home, and becomes a wealth-generating benefit. As potential first-time home buyers consider homeownership in today’s market, they should carefully weigh the costs, and potential future benefits, of owning a home against the cost of renting.”

Rent V. Own

In First American’s analysis of rent-versus-own scenarios, the annual cost of renting is considered the amount of rent paid that year. The annual cost of owning a home includes taxes, repairs, homeowners insurance, along with mortgage payments. It also assumes the potential buyer is taking out a 30-year, fixed-rate mortgage with a 5% down payment on a median-priced home.

Furthermore, the analysis weighs equity gained or lost during the period of ownership or rental.

"If the homeowner loses equity, it is added to the annual costs of owning. If a homeowner gains equity, it reduces the annual costs of owning," Fleming said. "If the annual equity gained exceeds the other annual costs of owning, then the house 'paid you' to live there.”

The following chart compares the cumulative wealth gained from owning with the cumulative wealth lost from renting using three different intervals – the peak of the housing bubble in 2006 to today, the 10-year window from 2014 to today, and pre-pandemic 2019 to today.