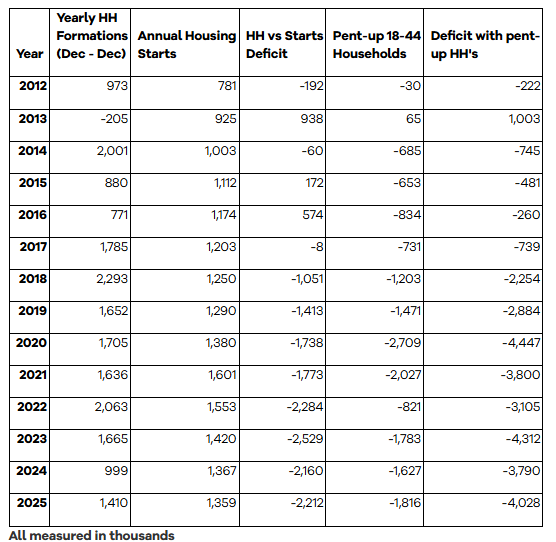

The U.S. housing supply gap widened to an estimated 4.03 million homes in 2025, according to Realtor.com’s 2026 Housing Supply Gap Report, highlighting persistent underbuilding amid strong household formation and ongoing demand.

The deficit expanded from approximately 3.8 million homes in 2024, underscoring a structural mismatch between housing supply and demand that has been building for more than a decade.

Last year saw about 1.41 million new households formed, compared with approximately 1.36 million housing starts, leaving the market with roughly 50,000 fewer units constructed than needed just in 2025.

"Even when annual construction and household formation are roughly balanced, the market is still digging out from more than a decade of underbuilding," said Danielle Hale, chief economist at Realtor.com. "A supply gap exceeding four million homes underscores how deeply rooted the shortage has become. Without a sustained and targeted increase in housing supply, particularly in areas with strong job growth and persistent demand, affordability challenges will continue to sideline many would-be buyers."

Although the annual shortfall may seem modest in isolation, it compounds a long history of underbuilding that continues to constrain overall inventory, fuel price pressure, and make homeownership harder to reach for many Americans — particularly younger households. Realtor.com economists found that roughly 1.82 million millennial and Gen Z households were “missing” in 2025, meaning they have delayed forming independent households because of limited housing options and affordability constraints.

Affordability Remains A Major Barrier

Even with mortgage rates improving in late 2025, the minimum recommended income to purchase a median-priced starter home was about $86,000, well above the earnings of many younger buyers. The median down payment reached approximately $30,400 — equivalent to roughly 14.4% of the purchase price — meaning it could take a typical household seven years or more to save for a down payment at current savings rates.

"While construction levels remain elevated compared with historical norms, they are not yet high enough, or targeted enough, to meaningfully close the gap," said Hannah Jones, senior economic research analyst at Realtor.com. "The fact that it would take roughly seven years to eliminate the deficit even under an optimistic building scenario highlights just how significant and persistent this shortage has become."

The report notes that even under an optimistic scenario in which construction increases significantly, it would take years to meaningfully close the existing gap. Analysts warn that sustained and targeted increases in housing supply — especially in regions with strong job growth — are critical to improving affordability and giving more Americans a realistic path to homeownership.