Intercontinental Exchange, Inc. today released its October 2024 ICE Mortgage Monitor Report, revealing that in August, the average monthly mortgage payment reached a record $2,070. This marks a 7.2% increase from last year and a 19.3% rise since early 2020.

According to ICE Vice President of Research and Analysis Andy Walden, every element of a mortgage payment – principal, interest, taxes, and insurance (PITI) – has been rising in recent years, but spikes in property insurance costs have been particularly sharp.

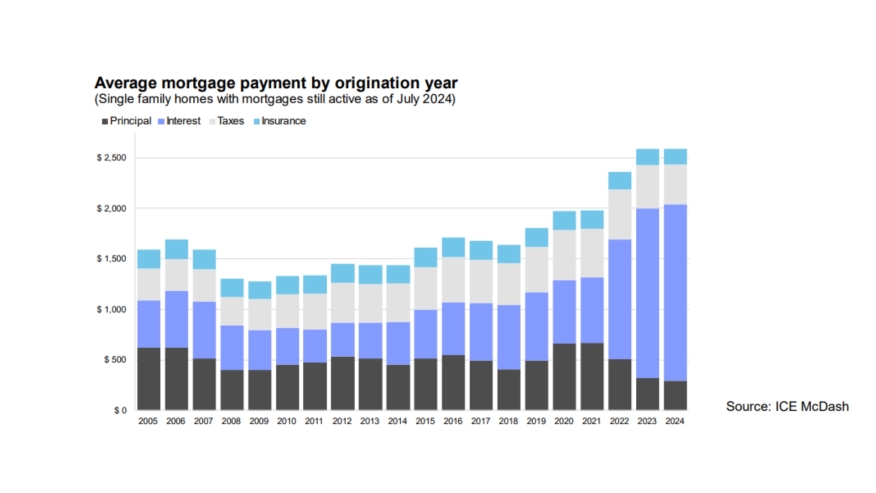

“When you peel back the layers on the data," said Walden, "a clear delineation appears between those fortunate enough to have taken out their mortgages before the Fed began to raise interest rates in 2022 and everyone who’s taken one out since. For this second group, a historically outsized share of their total mortgage payment is covering interest, with very little – even considering the young age of the loans – going towards principal.”

More seasoned mortgages, though they tend to have lower overall mortgage payments, are seeing a growing share of total PITI going to variable costs that exist outside of fixed rate terms and set principal and interest installments. Indeed, more than a third of their perceived ‘fixed’ housing payment consists of variable costs.

“While principal, interest, and taxes have all increased in the 15-17% range since the beginning of 2020, property insurance is up 52% over the same time span. And, yes, higher home prices logically lead to higher-dollar policies; that’s why looking at the cost for every $1,000 of coverage gives us such critical, apples-to-apples, context. Not only are homeowners paying 12% more today for the same dollar amount of coverage than they were, on average, from 2013-2022, but they’re also insuring a smaller share of the property’s underlying value. Given that coverage amounts are based not on a property’s market value, but its replacement cost, the average policy has also gone from covering over 100% of the average home’s value back in 2013-2015 to just 88% today.”

In hurricane-prone areas like New Orleans and Miami, annual insurance premiums on mortgaged homes average $17 per $1,000 of coverage, over three times the national average.

In tornado-prone areas like Oklahoma City, premiums average more than $10 per $1,000. Conversely, premiums are much lower in the Northeast and West, dropping below $3 per $1,000 in cities like San Jose, San Francisco, Las Vegas, and Rochester, NY.

“Given the rising costs of homeowner’s insurance in many areas of the country, it’s hardly surprising that premiums now make up more than 9.4% of monthly obligations on mortgaged single-family homes across the U.S.,” Walden added. “That’s up from an average of less than 7.7% from 2013-2020 and the highest share on record. Of course, in higher-risk areas such as New Orleans, the share of the mortgage payment earmarked for insurance can be as high as 25%. That’s something we also see beyond traditional hurricane zones. For example, insurance already accounts for more than 15% of monthly mortgage payments in areas like Oklahoma City, Wichita, and Tulsa and, every day, a growing number of potential trouble spots emerge.”

In parts of the Northeast, Midwest, and Texas, high property taxes rather than insurance, drive mortgage payment variability, with over 40% of payments being variable. In Rochester and Syracuse, NY, property taxes alone make up more than 35% of the average monthly payment.