A majority of U.S. loan officers are bracing for an economic downturn, according to HomeLight’s Q2 2025 Lender Insights & Predictions survey, which polled over 105 top lending institutions including The Loan Store, Fairway Independent Mortgage Corporation, and Cross Country Mortgage. Amid mounting concerns about a recession, shifting borrower behaviors, and volatile policy moves, lenders are turning to innovative financing strategies to keep the market moving.

Recession Fears Dominate The Forecast

The survey reveals that 63% of loan officers believe the United States is on the brink of — or already in — a recession. More than half (57%) predict that economic instability will delay homebuying activity, as fears of job loss and shrinking incomes hamper borrower confidence.

“We are already in a recession. Buyers are being cautious, and some are worried about losing their jobs,” said Texas-based loan officer Kirsten Fleenor.

Yet the situation isn’t entirely bleak. A slim majority (51%) of respondents believe a recession may drive down mortgage rates, potentially spurring new purchase and refinance activity among financially stable buyers.

Still, seasoned loan officer Bill Staiger cautioned, “(It’s) definitely a mixed bag. Rates would come down, which would encourage buyers…those who have kept their jobs, anyway. But I doubt that will have any impact on the shortage of inventory that is out there.”

Pipeline Volatility

Pipeline volatility has emerged as one of the most pressing challenges for loan officers in 2025, with a noticeable uptick in mortgage deals collapsing before they can reach closing. According to HomeLight’s Q2 2025 Lender Insights report, 50% of loan officers have observed an increase in pipeline deal cancellations—40% describe the increase as slight, while 10% categorize it as significant.

Charts source: HomeLight

But responses from loan officers suggest the trend is being driven by a combination of economic uncertainty, shifting buyer behavior, and financing hurdles.

The data reveals that the most common reason for cancellations — cited by 37% of respondents — is the discovery of major property issues during inspections. However, loan officer Devon Rowe believes many buyers are using minor inspection issues as justifications to walk away from contracts, even when sellers are willing to make repairs.

Other significant factors include high interest rates, failed financing due to high debt-to-income (DTI) ratios, and challenges in selling an existing home. With affordability squeezed by elevated mortgage rates and growing consumer debt, buyers are entering the process with less confidence and greater sensitivity to disruptions.

“Buyer commitment is wishy-washy,” observed Michelle Jacinto, a loan officer with 25 years of experience. “Any slight challenge, and they want to cancel. Anything from payments, cash to close, inspection items, or timeline changes.”

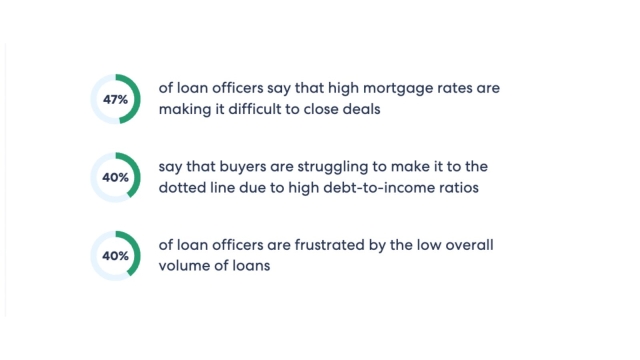

This fragility in the loan pipeline reflects broader market anxiety. Loan officers report widespread frustrations, with 47% citing high mortgage rates and 40% pointing to buyers struggling with DTI ratios as key obstacles to closing deals.

The result is a landscape where even qualified buyers hesitate, and minor obstacles derail transactions. To combat this, lenders are being urged to communicate clearly, set expectations early, and offer creative financing solutions where possible. In this environment, nurturing buyer confidence and reducing friction throughout the loan process has become more crucial than ever.

Creative Financing And DPAs Surge

In response to tighter financial conditions, buyers and lenders are embracing innovative mortgage strategies. California-based loan officer Kimberly Capizzi noted that many clients are exploring down payment assistance and adjustable-rate mortgages to remain competitive.

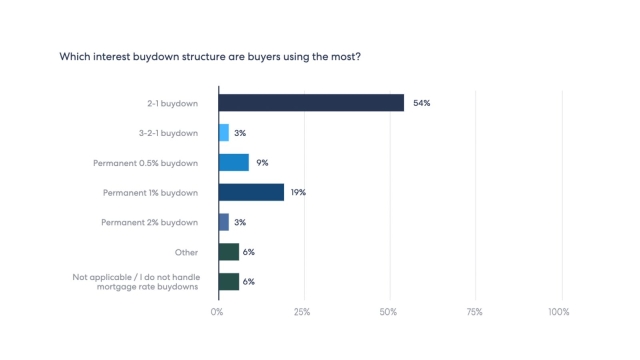

Seller-paid closing costs and 2-1 buydowns — where interest rates are temporarily lowered during the first two years of the loan — are particularly in vogue. According to the survey, 54% of loan officers say 2-1 buydowns are the most requested option, far ahead of permanent 1% buydowns at 19%.

“Creative solutions like these are helping buyers stay in the game,” said Colorado loan officer Annette Copeland, who has 45 years of industry experience.

Despite these hurdles, there is strong interest in down payment assistance. Twenty-one percent of loan officers highlighted a rise in demand for seller concessions, while others reported increased usage of aid programs.

A Down Payment Resource report confirms the trend: 43 new programs were introduced in 2025, bringing the nationwide total to 2,509. Seventy-four percent offer assistance with either down payments or closing costs.

Tariffs, Housing Starts, And Spending Cuts

Loan officers are split over the impact of the Trump administration’s proposed tariffs. While 53% foresee a negative effect on housing affordability and construction costs, 45% are not concerned.

Economists, however, are less optimistic. The IMF recently downgraded U.S. economic growth forecasts to 1.8% (from 2.7%) and raised the likelihood of a recession to 40%, up from 25% last October. Yale’s Budget Lab predicts tariffs could increase unemployment by 0.6% and spike prices for materials like steel and lumber.

“I’m concerned. Tariffs… could make it more expensive to build homes, which often leads to higher home prices,” warned Stephen Waldon, a loan officer with nearly a decade of experience.

While February saw an 11.2% jump in new home starts, future outlook is subdued. Single-family permits dropped 0.2% and multifamily permits fell 4.3%, according to Market Watch. The National Association of Home Builders expects housing starts to remain flat in 2025, citing regulatory and tariff uncertainties.

Compounding these challenges are steep cuts to affordable housing initiatives. At least $60 million in funding is now in limbo under the Department of Government Efficiency (DOGE), spearheaded by Tesla CEO Elon Musk. Analysts warn these cuts could weaken fair housing enforcement and exacerbate existing inequalities.

Outlook: Buy Now — If You Can

Despite the uncertainty, many loan officers encourage buyers to act sooner rather than later.

“Buy now before rates drop and the buying frenzy begins,” advised Missouri loan officer Dieterle.

Still, only 10% of respondents think mortgage rates will fall below 5%, while 25% expect affordability to deteriorate before improving. Meanwhile, 36% say buyers and sellers alike are waiting for rates to hit 5.75% before re-entering the market.

If rates drop to that threshold, loan officers predict home prices could spike by up to 16%.

“Make sure the mortgage payment ... fits in your budget,” cautioned Michael Ferraro, a loan officer with 28 years of experience. “Don’t overextend yourself, assuming rates will drop substantially.”

Market Realities

Currently, the average down payment seen by loan officers is 16%. On a median-priced $420,000 home, that amounts to $67,200. In expensive markets like California, Massachusetts, and Washington D.C., this figure can soar past $100,000.