loanDepot posted its seventh consecutive quarterly loss in the fourth quarter of 2023, but saw significant year-over-year improvements in their gain on sale margin and pull through weighted lock volume, according to a press release and earnings call announcing the earnings Tuesday evening.

Net losses for the fourth quarter totaled $59.8 million as compared to a net loss of $34.3 million in the third quarter of 2023 – a roughly 43% increase – “primarily due to revenues decreasing more than the decrease in expenses,” per the press release.

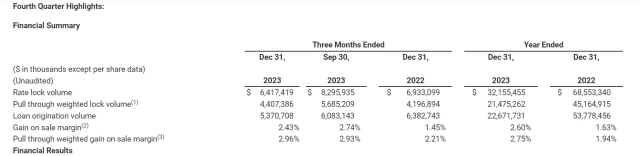

loanDepot reported a 22% drop in full-year revenue from 2022 – to $974 million – driven by a roughly 58% decline in origination volume, from $53.7 billion in 2022 to $22.6 billion in 2023.

Though the company reported an annual net loss of $236 million for 2023, it was able to narrow its losses by $375 million year over year, or 61% from 2022’s annual net loss of $611 million.

Loan origination (dollar) volume for the fourth quarter of 2023 was roughly $5.3 billion, a 12% drop from the third quarter’s roughly $6 billion, and a 16% drop from the fourth quarter of 2022’s roughly $6.3 billion in originations. Like much of the industry, loanDepot’s originations have been dominated by purchase volume, which rose to 76% of total origination in the fourth quarter from 71% in the third quarter.

Over the course of 2023, loanDepot slashed their operating budget by $693 million, or 36% to $1.25 billion – citing, ironically, cost productivity improvements and lower origination volume as primary drivers of decreased total expenses.

In other words, originating fewer loans saved the company money.

“Our cost reset has allowed us to maintain a strong liquidity position and at the same time support reinvestment in critical platforms and programs,” said loanDepot’s Chief Financial Officer David Hayes. “As the housing and mortgage markets begin to recover, we believe we enter 2024 positioned for success through a relentless focus on delivering against the pillars of Vision 2025.”

Though loanDepot’s fourth-quarter revenue and gain on sale margin weakened on a quarterly basis, both improved dramatically year over year.

Citing higher servicing income, an improved gain on sale margin, and improved pull through weighted lock volume as primary drivers, revenue was up 35% from the fourth quarter of 2022 ($169 million) to the fourth quarter of 2023 ($228 million).

The company’s gain on sale margin improved from 145 basis points in the fourth quarter of 2022 to 243 basis points in the fourth quarter of 2023 – a slight decline from 274 basis points in the third quarter. On a yearly basis, loanDepot’s gain on sale margin improved from 163 basis points in 2022 to 260 basis points in 2023 – nearly a full-percentage-point swing.

The improved gain on sale margin and pull through weighted gain on sale margin reflects the impact of loanDepot’s cost productivity improvements and reduced origination volume and expenses.

On the servicing side, loanDepot saw its servicing fee income increase by roughly $42 million year over year, an increase of roughly $12 million from the third quarter.

Volume-wise, the company grew its servicing portfolio 5.5% on an annual basis from roughly 471,022 units in 2022 to 496,894 units in 2023, representing a 2.8% increase in unpaid principal balance.

Notably, loanDepot experienced a 12.7% quarterly increase in the dollar-volume of loans that were 60+ days delinquent.

Not helping the fourth-quarter balance sheet was a $4.9 million quarterly increase in “non-volume related expenses”' such as “higher restructuring related charges, lease and other asset impairment costs, and legal expenses.”

As an outlook for the first quarter of 2024, loanDepot projects origination volume of between $3.5 billion and $5.5 billion, pull-through weighted rate lock volume of between $3.5 billion and $5.5 billion, and pull-through weighted gain on sale margin of between 270 basis points and 300 basis points.

The company reported a cash balance of $661 million, and a strong liquidity position moving into 2024.

Non-volume related expenses, including legal expenses, are expected to continue impacting loanDepot’s profitability at least through the first quarter of 2024, though.

The company reported to regulators in late February that a ransomware attack that occurred on January 4, 2024, would likely cost the company $12 million-$17 million, materially impacting profitability for the first quarter of 2024.

The incident exposed the personal data of 16.6 million customers, and loanDepot has been named in several class action lawsuits as a result.