Interest rates are in the hot seat, with many in the industry holding the common belief that even a slight decrease in basis points will improve housing affordability. But housing affordability also depends on house prices, which have competing effects; when interest rates increase, house prices tend to decline.

However, a new report from the Federal Reserve Bank of Dallas using data from the National Association of Realtors (NAR) presents the thesis that lower interest rates do not necessarily improve housing affordability.

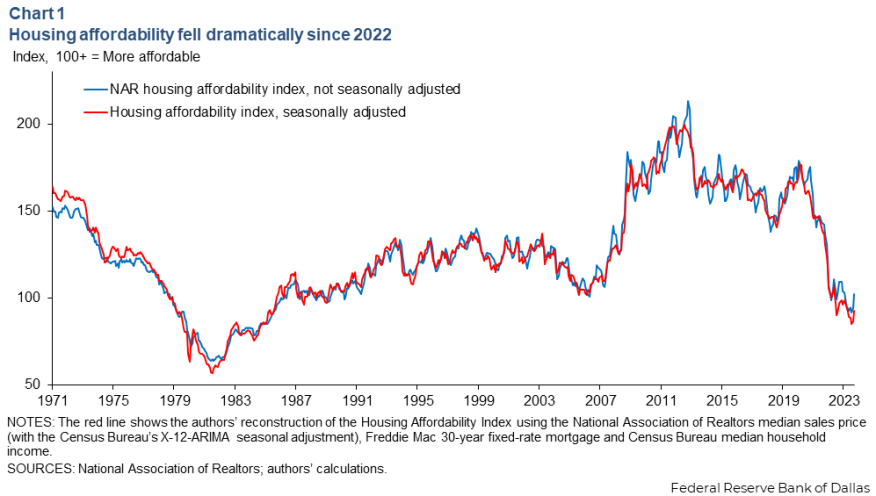

Interest rates increased from around 3% in December 2021 to nearly 7% two years later, a result of the Fed’s rapid monetary tightening. According to NAR, housing affordability declined almost 30% since December 2021, close to levels last seen in the late 1980s. Those sharply rising mortgage payments caused homebuyers to link it to housing affordability.

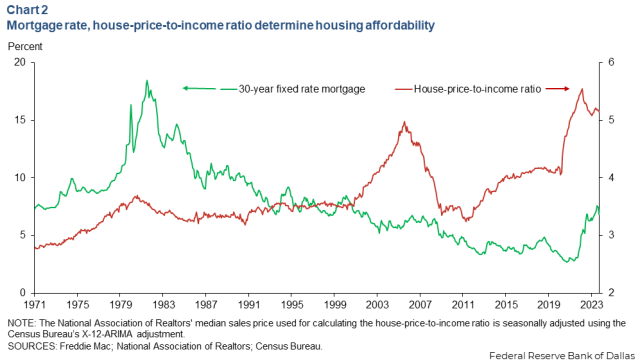

Yet, a multitude of factors drive affordability, such as house-price-to-income ratio.

Before 2000, the house-price-to-income ratio was relatively low, which supported housing affordability. After 2000 — besides the brief period of the housing bust from 2008 to 2012—the high price-to-income ratio lowered housing affordability. Post-pandemic, there was such a large increase in house prices that housing affordability would have declined even if mortgage rates stayed at their average.

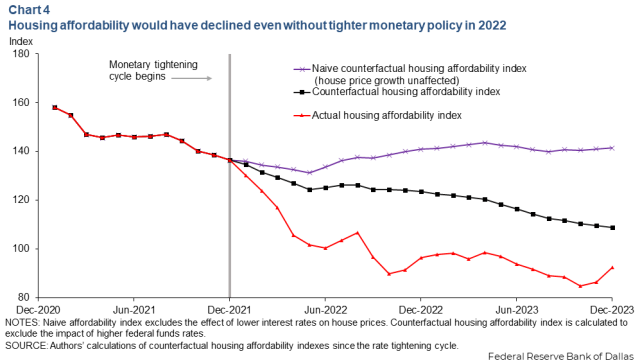

Some mistakenly believe had the Fed not raised the federal funds rate in early 2022, housing affordability would not have declined further, because house prices largely stabilized after mid-2022. But that neglects the effect of rate changes on house prices.

Estimates from the San Francisco Federal Reserve Bank suggest if short-term interest rates increased by 1 percentage point, it would lower house prices by 7.5% over two years. But if monetary policy did not tighten and mortgage rates stayed at its December 2021 level, house prices would have risen faster. The Dallas Fed estimates the monthly growth rate of house prices would have been 1.1 percentage points higher.

Changes in monetary policy directly affect mortgage rates, but there is also an indirect effect on house prices, the Dallas Fed concludes. When monetary policy is easier, mortgage rates tend to fall, while house prices tend to rise due to higher demand. These opposing channels imply that the net effect on affordability is ambiguous and potentially the opposite of what intuition based solely on mortgage rates would suggest.