New data released by the Mortgage Bankers Association (MBA) shows that homebuyer affordability improved modestly in December 2025, driven primarily by lower mortgage payments and steady income growth.

The MBA’s Purchase Applications Payment Index (PAPI), which measures median monthly mortgage payments relative to income based on Weekly Applications Survey data, recorded a decline in mortgage application payments last month.

The national median mortgage payment for purchase applications fell to $2,025 in December, down from November’s $2,034 and about 4.8% lower than a year earlier, according to the MBA report. Higher household earnings also contributed to improved affordability, with the PAPI decreasing 7.5% on an annual basis.

“Housing affordability conditions improved for the seventh consecutive month to close out 2025 because of lower mortgage rates and steady household earnings growth,” said Edward Seiler, MBA’s associate vice president of housing economics and executive director of the Research Institute for Housing America (RIHA). “MBA expects that moderating home-price appreciation, combined with even lower mortgage rates, will continue to gradually ease affordability constraints and support increased housing market activity.”

MBA research highlights that this marks the seventh consecutive month of improving affordability conditions, as declining interest rates and modest moderation in home-price appreciation eased some financial pressures on prospective buyers. However, affordability gains were uneven: while the median payment declined overall, FHA loan applicants saw modest increases in their typical payment amounts compared with the previous month, though still below year-ago levels.

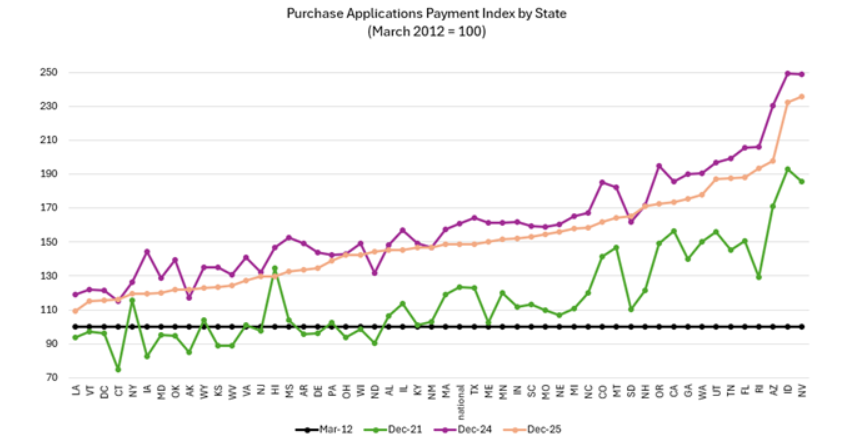

A Regional Look

Geographically, states such as Nevada, Idaho, and Arizona posted some of the highest payment-to-income ratios, while Louisiana and Vermont remained more affordable by comparison. Affordability improvements also extended to Black and Hispanic households, with index measures indicating slight declines in payment-to-income ratios for these groups in December.

Overall, the MBA’s December data suggests a cautiously optimistic backdrop for the housing market as affordability pressures eased heading into 2026.

Key Data Points

Among other top level data points, the MBA found that:

- The national median mortgage payment for FHA loan applicants was $1,802 in December, up from $1,776 in November and down from $1,866 in December 2024.

- The national median mortgage payment for conventional loan applicants was $2,036, down from $2,063 in November and down from $2,128 in December 2024.

- The top five states with the highest PAPI were: Nevada (235.8), Idaho (232.5), Arizona (197.6), Rhode Island (193.3), and Florida (187.9).

- The top five states with the lowest PAPI were: Louisiana (109.2), Vermont (115.2), Washington, D.C. (115.5), Connecticut (116.2), and New York (119.5).

- Homebuyer affordability increased for Black households, with the national PAPI decreasing from 154.5 in November to 153.8 in December.

- Homebuyer affordability increased for Hispanic households, with the national PAPI decreasing from 141.8 in November to 141.1 in December.

- Homebuyer affordability increased for white households, with the national PAPI decreasing from 151.2 in November to 150.5 in December.