Leading to 'crushed' expectations of another significant rate cut

The September jobs report came back with flying colors, adding far more jobs than Wall Street economists projected while the unemployment rate ticked down, leading to what can only be called a crushing defeat for mortgage professionals. In response, the average rate for the benchmark 30-year fixed rate mortgage (FRM) shot up 1 basis point from last week to 6.23%.

Data from the Bureau of Labor Statistics released October 4 showed the labor market added 254,000 payrolls in September, more than the 150,000 expected by economists. In August, the unemployment rate fell to 4.1% from 4.2%. Revisions to both the July and August report showed the US economy added 72,000 more jobs during those two months than previously reported.

Additionally, wage growth rose 4% annually in August from 3.9% last year. On a monthly basis, wages increased 0.4%, in line with August's reading.

The data creates a picture that’s altogether much too sunny for the mortgage industry. A few rain clouds are needed to dampen the labor market's outlook and push the Fed into slashing interest rates.

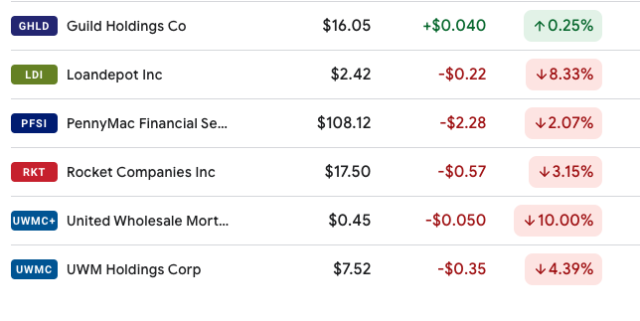

As a result of latest Nonfarm Payroll report, mortgage stocks are down while the rest of the market is up.

“The September Jobs report crushed consensus expectations, likely undercutting mounting concerns of weakness in the labor market and lowering the probability of a 50-basis point cut in November,” said First American Deputy Chief Economist Odeta Kushi. “The 10-year treasury yield is higher on this news, which may result in some upward pressure on mortgage rates.”

Mortgage Bankers Association (MBA) Senior Vice President and Chief Economist Mike Fratantoni commented on the positive data found in the jobs report — noting job gains in food services, health care, construction, and government hiring — saying, "All of these signs point toward a successful 'soft landing,' but also stoke worries that inflation may not move in a straight line to the Fed’s 2% target. This report could certainly slow the expected pace of rate cuts."

The CME Group's FedWatch Tool shows there were many dashed hopes following the jobs report; markets were pricing in a roughly 12% chance that the Fed cuts interest rates by half a percentage point in November, down from a 53% chance a week ago.

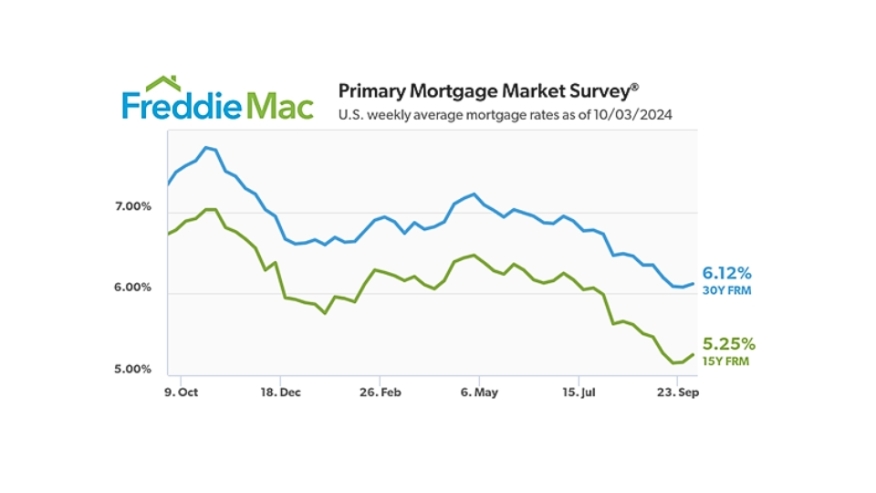

Yesterday, the Freddie Mac’s Primary Mortgage Market Survey, showed the 30-year fixed-rate mortgage (FRM) averaged 6.12%, up from last week's averaged 6.08%. The 15-year FRM averaged 5.25%, up from last week's averaged 5.16%. By Friday, October 4, the 30-year FRM ticked up to 6.23%.

Still, at this time last year, the 30-year FRM averaged 7.49% and the 15-year FRM averaged 6.78%.

“The decline in mortgage rates has stalled due to a mix of escalating geopolitical tensions and a rebound in short-term rates that indicate the market’s enthusiasm on rate cuts was premature,” said Sam Khater, Freddie Mac’s Chief Economist. “Zooming out to the bigger picture, mortgage rates have declined one and a half percentage points over the last 12 months, home price growth is slowing, inventory is increasing, and incomes continue to rise. As a result, the backdrop for homebuyers this fall is improving and should continue through the rest of the year.”

“Interest rates jumped on the release of this report," Fratantoni added. "MBA’s forecast is for longer-term rates, including mortgage rates, to remain within a relatively narrow range over the next year. This news will push mortgage rates to the top of that range, but we do expect that mortgage rates will stay close to 6% over the next 12 months.”

Seller/servicers using artificial intelligence in origination or servicing must have formal policies, oversight, and vendor controls in place

Fannie Mae’s artificial intelligence and machine-learning governance requirements take effect Thursday, Aug. 6, giving approved seller/servicers a final deadline to formalize how the technology is used across mortgage origination and servicing.The requirements apply when a s...

Pending sales fell to their lowest level since early April, but lower asking prices and reduced competition give originators more options to structure deals for qualified borrowers

Higher mortgage rates are thinning the purchase pipeline, even as lower asking prices and reduced competition give borrowers still in the market more leverage.Seasonally adjusted U.S. pending home sales totaled 322,739 during the four weeks ending July 26, their lowest level...

Pending sales fell to their lowest level since early April, but lower asking prices and reduced competition give originators more options to structure deals for qualified borrowers

Price cuts and longer listing times are creating opportunities for loan officers to help borrowers negotiate seller concessions, but leverage varies sharply by metro