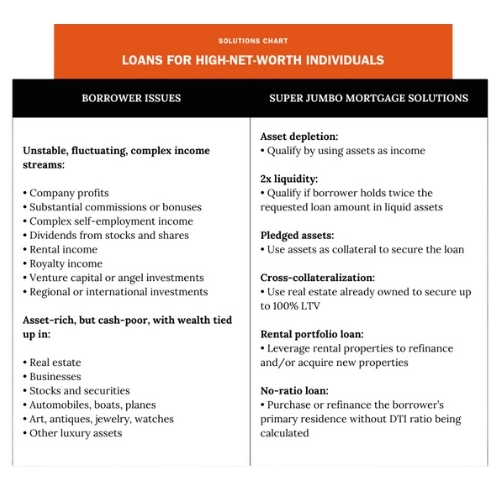

Asset depletion: DTI tool

The asset depletion program is ideal for borrowers who have substantial wealth but are unable to sufficiently document their income.

The following assets may be used to qualify: checking and savings accounts, stocks and bonds, mutual and money market funds, income from real estate investments, vested amounts in retirement funds, annuities, pensions, and cryptocurrency.

Based on the assets, the lender calculates how long they can generate an income stream sufficient to cover the mortgage payments.

The main benefit of asset depletion is it allows an alternative way to satisfy the lender’s debt-to-income ratio (DTI) requirement.

2x liquidity

As a creative variation of the asset depletion program, some super jumbo lenders simply require that the borrower hold at least twice the requested loan amount in liquid assets. For example, for a $3 million loan, the borrower would need to show at least $6 million in liquid assets.

Pledged assets: LTV tool

Similar to the asset depletion program, the pledged assets program allows the borrower to use assets to qualify. However, there is an important difference. The pledged assets program requires the borrower to actually pledge the assets as collateral for the loan.

Pledging assets allows the borrower to obtain higher LTV, up to 90%.

Assets that can be pledged include cash, stocks, bonds, certificates of deposit (CDs), savings accounts, and mutual funds. Some creative lenders allow the pledging of more exotic assets, such as automobiles, art, antiques, jewelry, and royalty income streams.

Cross-collateralization

While the pledged assets program entails pledging non-real-estate assets such as stocks and savings accounts, the cross-collateralization program involves pledging real estate.

With this approach, the lender takes a first lien position on both the newly purchased property and the cross-collateralized property.

The primary advantage of cross-collateralization is the ability to obtain up to 100% LTV (i.e., 0% down payment).

Rental portfolio loan

While the cross-collateralization program involves 2 properties, the rental portfolio loan is for borrowers with extensive portfolios of multiple rental investment properties, and are looking to refinance and/or acquire a new rental property.

A rental portfolio loan consolidates any existing mortgages into one single jumbo-sized loan, offering flexibility in terms and conditions. This streamlines monthly payments and simplifies debt management for the investor.

No-Ratio loan

A no-ratio loan is a mortgage that does not require any calculation of the borrower’s DTI. Quite simply, there is no verification of employment or income required.

This approach is appealing to borrowers who may have significant assets but prefer not to disclose their income or whose income might not qualify under traditional loan standards.

The program is available only for owner-occupied properties and the maximum loan amount is $2 million, but can be higher by exception depending on the strengths of the file.

Ripe For Opportunity

With the exit of major banks like First Republic Bank and the remaining banks tightening up their credit boxes, the super jumbo mortgage landscape in California is ripe for opportunities.

The usual arsenal of non-QM products (such as bank statement, P&L, and DSCR programs) is not enough to stay competitive.

Instead, to stand out from the crowd, mortgage brokers should also offer the exotic loan products highlighted in this article, as they specifically cater to high-net-worth individuals with super jumbo needs.

By embracing nonbank lenders and diversifying their portfolios with the most cutting edge lending options, brokers can establish a book of business that’s resilient to any economic or banking uncertainties.