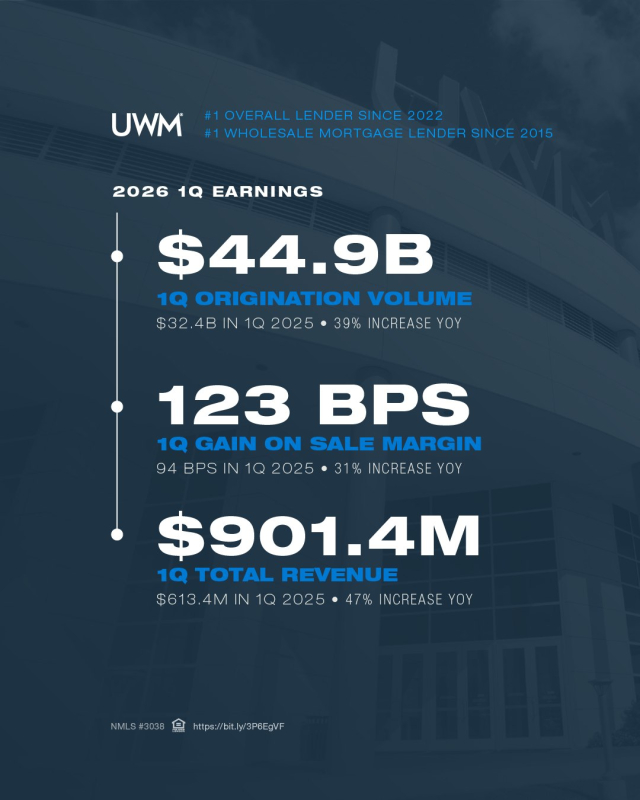

UWM Holdings Corporation returned to profitability in the first quarter of 2026, delivering $44.9 billion in originations as margins expanded and refinance volume surged in a still-elevated rate environment.

The Pontiac, Mich.-based lender reported $901.4 million in total revenue, up 47% year over year and above company guidance, alongside $170.4 million in net income — reversing a $247.0 million net loss in Q1 2025, according to its earnings release.

The production total marked UWM’s second-best first quarter ever, with volume up 39% year over year.

UWM reported a 123 basis point (1.23%) gain margin, up 31% year over year from 94 basis points, signaling improved execution in a market where many lenders are still facing pressure.

Chairman and CEO Mat Ishbia said he expects margins to remain relatively stable, with potential upside depending on rate movement.

“I kind of see this range … being the right range … not significantly higher, not significantly lower,” Ishbia said during the Q&A with investors.

“I actually think there’s upside in the margins.”

Refi Volume Leads Growth

Production leaned heavily on refinances:

- $26.3 billion in refinance originations

- $18.7 billion in purchase loans

Refinance volume more than doubled year over year — a standout result in a higher-rate environment where many lenders have struggled to generate refi activity.

“We did a heck of a job on the refinance side,” said Mat Ishbia.

Ishbia pointed to a combination of broker execution and borrower retention as key drivers, particularly through UWM’s use of AI tools to reconnect with past clients.

The takeaway: refinance volume isn’t disappearing — it’s consolidating among lenders that can identify opportunities and bring borrowers back into the pipeline.

AI Platform Driving Measurable Volume

UWM is also leaning into AI-driven borrower engagement through its “Mia” platform — and the impact is already showing up in production.

“Roughly … 80,000 to 100,000 closings over the last year have come from Mia,” Ishbia said, adding the tool is responsible for roughly 12% to 13% of refinance activity.

The platform automates borrower outreach and follow-up, helping brokers stay connected to past clients and recapture refinance opportunities that might otherwise be lost.

Credit Scoring Shift

Ishbia also weighed in on the evolving credit scoring landscape, including the use of alternative models and expanded data inputs to qualify more borrowers.

“We’re using Vantage and expanded data like rent history to help more borrowers qualify who might have been shut out under traditional FICO alone,” said Ishbia.

The discussion comes as the Federal Housing Finance Agency and the government-sponsored enterprises — Fannie Mae and Freddie Mac — continue evaluating broader adoption of alternative credit models.

“When you add real-world data like consistent rent payments, people who look like lower-score borrowers on paper can actually qualify for a home,” Ishbia said.

“A lot of the conversation is about when this will be ‘live’ … the important thing is we’re already helping borrowers today.”

The shift could allow more borrowers with limited traditional credit histories to qualify, particularly those with strong payment behavior that hasn’t historically been captured in standard scoring models.

Servicing Push Builds Long-Term Engine

UWM continues to scale its servicing platform as part of a broader strategy to stabilize earnings across cycles.

The company said all new originations are now being boarded on its proprietary servicing platform and that it is on pace to bring all loans in-house by October 2026, ahead of its previously communicated timeline.

“All new originations are going on … and we’ll bring all of our loans in-house … by the end of this year,” Ishbia said.

The shift is expected to improve borrower retention, reduce costs, and create more consistent long-term revenue.

UWM also continues to expand borrower engagement through its collaboration with Bilt, allowing borrowers to earn rewards on on-time mortgage payments — a tool brokers can use to differentiate and strengthen long-term relationships.

Ishbia On Two Harbors

Ishbia also used the Q&A to address UWM’s ongoing pursuit of Two Harbors Investment Corp., offering a pointed assessment of the company’s leadership and the deal process.

“We don’t see much value in their management … their leadership team we were not as impressed with,” he said.

He said UWM remains willing to move forward at $12 per share and indicated a preference for cash over stock given current market conditions.

“We plan on paying $12 … quite honestly … I’d rather pay it in cash than in stock,” Ishbia said.

Ishbia added that the company has attempted to re-engage but has not received a response.

“They never engaged … they just went out to another offer … they basically ignored it,” he said, adding the board “is maybe playing some games.”

He reiterated that the strategic value lies primarily in the company’s servicing portfolio and shareholder base.

“It’s very clear to us that it’s the MSR book and the shareholders that have value — we don’t have any value for the leadership team,” Ishbia said.

Broker Strategy Drives Growth

Ishbia also used the Q&A to reinforce UWM’s core strategy: growing the broker channel itself, not just competing within it.

He said UWM currently works with roughly 12,000 to 12,500 brokers, with only a small number of high-producing shops not fully aligned with the company.

“Almost everyone in the broker market already works with UWM … that’s why we’re close to 50% share in the broker channel,” Ishbia said.

He added that the broader broker channel still represents a relatively small portion of the total mortgage market — but sees significant room for expansion.

“Broker share of the mortgage market is roughly 20% today … my long-term view is we can double that,” he said.

The strategy is straightforward: as more loan officers move into the broker channel, UWM expects its own volume to grow alongside that shift.

“The more the broker channel grows, the more UWM grows,” Ishbia said.

Margins, Pricing And Broker Support

Ishbia pushed back on the idea that competing on price alone is a sustainable strategy, emphasizing that UWM’s value proposition extends beyond rate.

“If the only thing that mattered was being the absolute lowest price, every broker would just cut their comp … that’s not how this business works,” he said.

Instead, UWM focuses on a combination of pricing, service, and tools designed to help brokers win and retain clients.

The company continues to run targeted pricing initiatives — including incentives tied to purchase volume and adoption of hybrid or virtual closings — which Ishbia said are designed to improve borrower experience and long-term retention.

“Our pricing initiatives … are about changing behavior and improving the borrower experience, not just racing to the bottom,” he said.

Long-Term Outlook

Looking ahead, Ishbia outlined a multi-year growth strategy centered on scale, efficiency, and diversified revenue streams.

“Over the next five years, I expect UWM to do at least $1.3 trillion in mortgages … that’s the North Star,” he said.

He noted that annual production could vary significantly depending on market conditions.

“You could see a year at $400 billion and another at $150 billion, but in total I feel very confident in that $1.3 trillion-plus outlook.”

A key component of that growth is operational leverage, driven by technology and automation.

“We’re talking about more than doubling our volume while keeping expenses basically flat, driven by the impact of our AI initiatives,” Ishbia said.

He added that gain-on-sale margins are expected to remain within a relatively stable range, while additional revenue streams continue to grow.

“Gain-on-sale margins should stay in roughly the range you’re seeing now … nothing dramatically higher or lower in our base case.”

“We see almost another 20% to 25% in other revenue streams … those products are already starting to show up.”

What It Means

For originators, the quarter reinforces several key trends:

- Refinance opportunity still exists — but is increasingly driven by retention and technology

- Margins are stabilizing, with potential upside depending on rate movement

- AI and automation are beginning to materially impact production

- Credit expansion could bring more borrowers into the market

At the same time, UWM is making a broader bet: that growth will come not just from rate cycles, but from expanding the broker channel, improving borrower retention, and scaling more efficiently than competitors.

The refi isn’t gone, it’s just going to the lenders that know how to capture it.