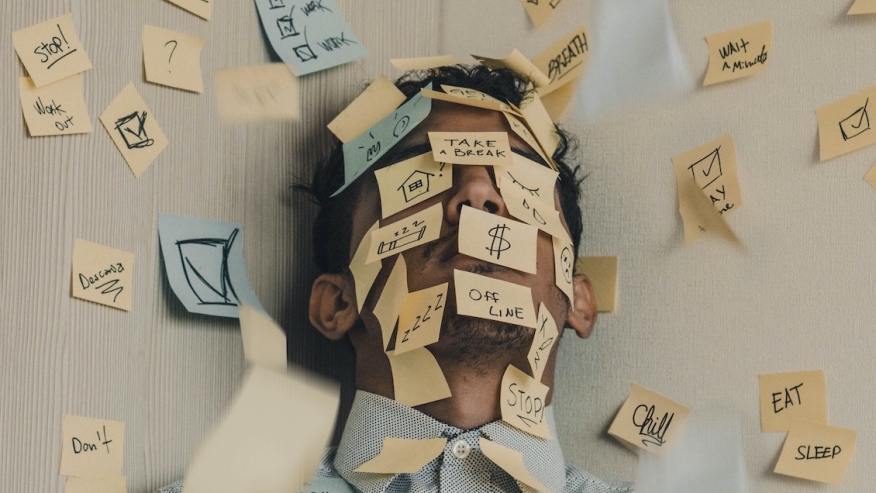

Recognizing Burnout Issues

As many employees were forced to move to working remotely because of the pandemic, it made it more and more difficult to keep work from creeping into their personal lives. Being just steps away from a home office on the weekend or being unable to resist the urge to respond to one last email to get ahead on work became the norm for so many people in the mortgage industry because there was no longer that clear separation from work. Unfortunately, these habits have stuck around, and almost seem expected by many lenders for employees to continue to always be “on call” even as many employees have returned to working back in an office setting in some capacity.

Yes, many lenders have tried offering additional incentives to their employees to reward them for grinding day after day but at a certain point, plain and simple, sometimes employees just need the ability to take time off without the fear of being shamed or feeling like they will be crushed by the weight of the work that will pile up in their absence.

According to a recent Gallup study, some of the top reasons for employee burnout in the mortgage industry included an unmanageable workload coupled with the fear of falling behind should the employee take time off, lack of support from management, specifically when it came to being proactive about hiring to ensure employees didn’t have too much on their plates, and finally unreasonable time constraints to get tasks done so employees felt it was necessary to work long hours or on weekends just to meet deadlines.

Avoidable

The most unfortunate thing about all these causes of employee burn out is they are entirely preventable. It’s important for management to have open communication with employees and recognizing when there is a need to hire additional employees rather than overloading their current work force. Also setting realistic deadlines and expectations for certain tasks and accepting that employees have limits to what they are able to take on are all things lenders need to get a better handle on if they want to retain their current workforce.

Finally, lenders need to stop incentivizing employees to not use their time off or at the very least, stop shaming employees that do use the time off that they earn. There continues to be an unspoken stigma in the mortgage industry about taking time off. Account Executives especially are always expected to be available to take a phone call or answer an email regardless of the day or time. Lenders should take the time to establish a small team or at the very least a backup for each member of their sales team to allow employees to take time off when they need it.