Loan Quality

The performance of MSRs’ underlying loans — specifically, the rates of default and delinquency — directly affect MSR values because of the disruptions they cause to those loans’ cash flows.

Delinquencies lead to higher advance payments for servicers, making them unattractive for the MSR investors. Meanwhile, higher default rates can lead to higher costs and reduced income for both servicers and investors, decreasing MSR values.

Conversely, lower delinquency and default rates are favorable for MSR valuation. The likelihood of delinquency and default are directly tied to the credit quality of a servicing portfolio, which corresponds to the borrower characteristics in that loan pool.

The overall credit quality of the servicing portfolio influences MSR valuation indirectly. Higher FICO credit scores and lower debt-to-income (DTI) ratio loans lead to lower rates of delinquency and default, rendering MSRs with those underlying qualities more valuable.

Beyond the credit qualities and performance of MSRs’ underlying assets, the manner in which a loan is originated and serviced, including the ambient market conditions, ties the value of the MSR to the reason a lender, servicer, or investor may want to hold an MSR in the first place.

Originator Type And Market Conditions

Depository banks and independent mortgage banks (IMBs) have different strategies when it comes to servicing mortgages. IMBs typically focus on loan origination and sell servicing rights because they lack the capital reserves to hold them on their balance sheets. Depositories, however, can integrate servicing into other bank operations and hold the loans in their portfolios.

When the Federal Reserve dropped its benchmark borrowing rate to zero during the COVID-19 pandemic, trillions of dollars worth of mortgages were originated (2020, 2021) at the lowest rates ever. Flush with cash, IMBs were able to retain servicing without the need to sell it. The tables turned, however, when the Fed started raising rates in the second quarter of 2022.

As origination profitability tumbled, MSR values began increasing significantly, keeping pace with interest rates. Increased escrow amounts and earnings, combined with low delinquency and default rates, pushed servicing values considerably higher.

Because holders of servicing (depending on the state guidelines) can earn interest on the escrows, MSR values increased significantly as Fed fund rates have gone from 0% to 5.25%.

State guidelines play a significant role in determining how much a servicer earns from escrows.

As originations and origination profitability eroded over the past two years, however, lenders have sold their MSR books, taking advantage of strong valuations to better manage cash flows and shore up liquidity. Still, very few market transactions of MSRs occur on a monthly basis because it is an esoteric asset class.

Lenders rely on fair value estimates to book the value of servicing. This measure of the MSRs’ worth reflects the present value of expected future cash flows, adjusted for risks and uncertainties. Fair value considers assumptions such as prepayment rates, default rates, interest rate changes, and servicing costs. It is more theoretical and based on models that project these future cash flows and risks rather than marks derived from trading MSRs.

Discounted Cash Flow (DCF) analysis is commonly used to estimate the fair value of MSRs, which involves forecasting future cash flows from servicing fees and discounting those cash flows back to present value using an appropriate discount rate. The discount rate associated with Ginnie Mae servicing, for example, is higher than for Fannie and Freddie loans because of Ginnie loans’ inherently riskier collateral.

Nevertheless, MSR valuation is integral to pricing mortgage rate sheets because it influences a lender’s understanding of servicing costs, profitability, and risk. By accurately valuing MSRs, lenders can set competitive mortgage rates that reflect the costs and benefits associated with servicing mortgages, ultimately affecting their overall pricing strategy.

When MSR values are high, lenders may offer more attractive rates to borrowers because they expect to generate significant servicing income or can sell those MSRs at a premium. When MSR values drop, lenders might adjust mortgage rates upward to mitigate the impact of reduced servicing income, increased servicing costs, or lower fair book values when selling in bulk. It is crucial for lenders to regularly back-test the fair book value with the market value so as not to underestimate or overestimate servicing valuations.

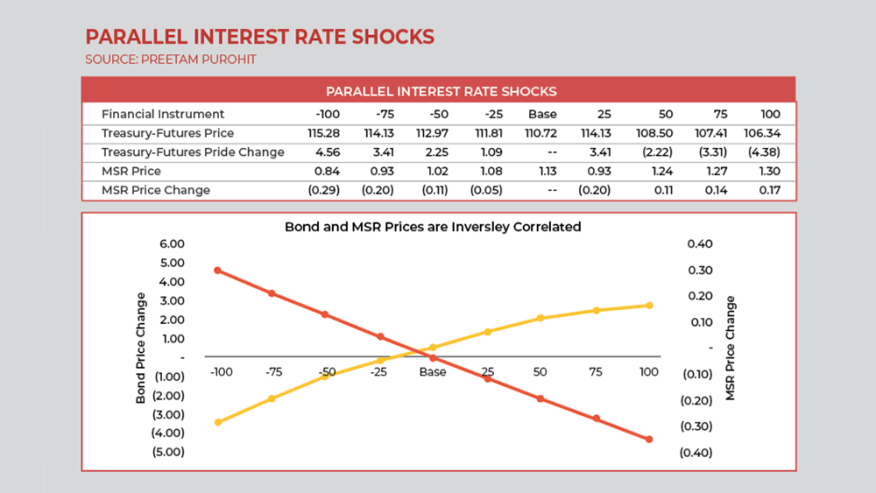

Also important for lenders to remember, servicing value used for the rate sheet is a function of the interest rate and loan balance being originated. Significant mismatches can occur when using an average servicing value for all loans originated on a particular day. Considering the table below, using the MSR value for a $250,000 loan to price a $100,000 loan would result in a lower profit for the lender.

Lenders often hedge their MSR exposure to manage risks associated with interest rate fluctuations and prepayment speeds. The valuation of MSRs helps in establishing these hedges and can influence mortgage pricing. Effective hedging strategies, informed by MSR valuations, can allow lenders to offer more stable and competitive mortgage rates, while protecting lenders from sudden shifts in the primary market or investor attitudes.

Advances

As mentioned previously, servicers are sometimes required to advance payments to investors when a borrower is delinquent, covering missed principal and interest payments. The servicer later recoups these advances when the borrower catches up on payments or through foreclosure proceeds.

This advance requirement has the potential to create a liquidity issue for IMBs if a massive delinquency event hits an IMB/servicer all at once. This is one of the major reasons that IMBs usually only retain a small servicing book, if one at all. However, one potential way to overcome this issue is using early buyouts (EBOs).

With EBOs, an IMB can partner with a private investor to buy any loans that are 90+ days delinquent from their servicing book. These loans are then modified in a manner that enables the borrower to get current on their mortgage. One popular vehicle for Ginnie Mae issuances is for the loan to be conveyed into an ET pool (40- year pool), reducing the borrower’s monthly payment with a longer amortization. When the borrower is current, the loan is sold to investors.

Conclusion

With the Fed beginning its easing cycle with a 50-basis point cut to its benchmark interest rate in September, the employment side of the central bank’s double mandate is attracting more focus than the inflation battle. Recently originated and retained servicing will provide opportunities to refinance. At the same time, and in the absence of a strong recapture strategy, the least that a lender can do is hedge this MSR book.

Understanding and executing effective MSR strategies is crucial for lenders aiming to maintain profitability and competitiveness in the ever-changing mortgage landscape. As interest rates and market conditions continue to fluctuate, the ability to accurately value and strategically leverage MSRs will remain a key differentiator between lenders struggling with loan volume.