Xpert Home Lending Inc., a fast-growing mortgage brokerage led by a former top account executive at United Wholesale Mortgage (UWM), has agreed to a sweeping consent order with the Washington State Department of Financial Institutions (DFI) following an investigation into multiple violations of the state’s Consumer Loan Act.

In just a few years, Xpert Home Lending had positioned itself as a major force in the mortgage industry. According to the NMLS, the company has grown to 602 loan originators since its founding in 2021. That rapid expansion had placed the brokerage on the fast track to joining the ranks of mega brokers before the consent order was issued on May 2, 2025.

The order resolves a case against the company and its co-owners, CEO Alysia Jill Budd and Chief Compliance Officer Richard Louis Hanlin. The agreement includes monetary penalties, license sanctions, and corrective action requirements stemming from a compliance examination conducted between November 2023 and February 2024.

The examination revealed multiple violations of Washington's Consumer Loan Act, including:

- The company did not develop and implement supervisory plans on or before February 2, 2024;

- Xpert, Budd, and Hanlin operated without supervisory plans in place for all supervisors who supervised loan origination, underwriting, or processing employees on behalf of Xpert;

- From about Jan. 21, 2023 to Feb. 2, 2024, the respondents aided and abetted an individual’s violation of two previous orders issued by DFI prohibiting the individual from participation in the conduct of the affairs of a consumer loan company licensed by DFI;

- From about Nov. 15, 2023 to Feb. 2, 2023, Xpert had between 1-15 branch offices that were not identified in the NMLS and were not licensed with DFI. Respondents had Washington mortgage loan originators associated, listed, or assigned to at least four branch offices;

- On or about Nov. 13, 2023, respondents reported to DFI that they did not have any branches. On or about Nov. 15, 2023, respondents reported to the Department that they had at least 15 branch offices.

- On or before Feb. 2, 2024 and on at least one website advertising Xpert, the company and a mortgage loan originator employed by it did not provide one or more of the following: Xpert’s name as entered on NMLS, Xpert’s license number, and/or a link to the NMLS Consumer Access webpage.

- On or before March 6, 2023 and in at least two closed loans for properties located in Washington state, Xpert did not date, or did not accurately date, at least one residential mortgage loan application;

- On or before Feb. 2, 2024, Xpert did not develop a compliant anti-money laundering (AML) program that complies with the requirements of the Financial Crimes Enforcement Network (FinCEN);

- From about Feb. 15, 2023 to March 9, 2023 — in at least two closed loans for properties located in Washington State — Xpert did not provide complete closing disclosures. The company did not list the origination fees in the correct section, did not include all seller paid fees, or did not indicate the recipient of the fees charged.

The order states that DFI's investigation into the alleged violations continues to date.

As part of the settlement, the respondents agreed to pay a whopping total of $185,664.28. That amount includes a $72,000 fine, $22,593.69 in investigation fees, $3,269.53 in examination costs, and $87,801.06 in prosecution costs. Payment of the settlement is now due in full.

Imposed Sanctions

The consent order also imposes a series of stayed sanctions that will remain in effect through May 2, 2028, unless the respondents fail to comply with the agreement. If that occurs, the Washington DFI may lift the stay and enforce the penalties without further notice, unless contested in a formal adjudicative hearing.

Under the terms of the order, Xpert Home Lending’s license to operate as a consumer loan company is revoked but stayed for three years. That means the revocation won’t take effect unless the parties violate the terms of the agreement.

Hanlin’s mortgage loan originator license is also revoked under the same conditions. Additionally, both the company and Hanlin are prohibited from participating in any Washington-licensed consumer lending activities for the same period, with the prohibition likewise stayed.

Budd faces a separate set of restrictions. For three years, she is barred from directly or indirectly participating in loan origination or servicing activities in the state, unless she is involved only in third-party coordination, recruiting or employment functions. She may remain employed by Xpert Home Lending but may not apply for any state licenses or registrations during the restriction period. Any application submitted after that time must meet the licensing standards in place at that time.

Some Violations Admitted, Some Contested

While agreeing to the consent order, the respondents admitted to some but not all of the allegations detailed in an amended statement of charges filed in November 2024. They acknowledged that the company had advertised without the required disclosures, failed to accurately date residential mortgage loan applications, and did not provide complete closing disclosures in at least two transactions involving Washington properties.

They did not admit to other findings cited by examiners, including operating without supervisory plans, making false statements to regulators, failing to license branch locations, and failing to establish a compliant anti-money laundering program. The investigation also alleged that the company aided and abetted a previously barred individual’s participation in the mortgage business in violation of earlier regulatory orders.

Corrective Actions

In addition to financial penalties and licensing restrictions, the consent order requires Xpert Home Lending to take corrective actions. That includes ensuring all branch locations are licensed, updating corporate policies and procedures, and submitting proof of compliance to DFI.

The department emphasized that any failure to comply with the order’s terms could trigger additional legal action.

Budd and Hanlin signed the order on April 24, 2025, and it was approved by Ali Higgs, acting director of the Division of Consumer Services, on May 2.

By signing the order, Budd and Hanlin waived their right to a hearing or further appeal. If any terms are violated during the three-year stay, DFI can lift the stay and impose full penalties — including license revocations and industry bans — without further warning unless challenged in a formal hearing.

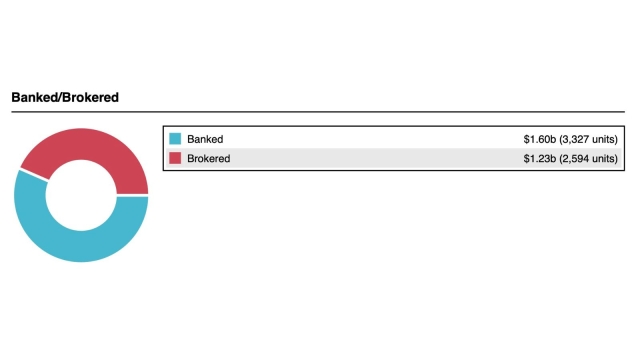

Loan Distribution

According to data from Modex, Xpert Home Lending banked most of its loans in the past 12 months while only about 44% were brokered to wholesale lenders. Its top lender beneficiary happens to be the CEO’s former employer, UWM, which received at least 9.5% of Xpert’s loans.